LGH Top Picks, Themes … and Why My Gravatar is a Blue Jay Taking Flight, a.k.a. ‘Front Page.’ (Publ. Jan. 27, 2018; Updated Sept. and Dec. 27, 2019–and July, 2020).

“FamilyCourtMatters.org” gets you back to the top of this page. The descriptive title is just a general guide to its contents.

LGH Top Picks, Themes … and Why My Gravatar is a Blue Jay Taking Flight, a.k.a. ‘Front Page.’ (Publ. Jan. 27, 2018; Updated Sept. and Dec. 27, 2019–and July, 2020). (shortlink ends “-8o0,” which I explain below, under a “Shortlink Shorthand” section).. Shortlinks are just a system-generated protocol I chose to display (the last three characters of) openly, on all posts and pages, for my convenience, because of the size of this blog and how often I need to cross-reference things I’ve already explained earlier — sometimes years earlier… Also people who wish to quote my blog, with its over 800 posts (!) should include that short-link and cite at least the post or page’s date.

UPDATE PARAGRAPHs July 28, 2020…and consider this update section itself “in transition” as I got to talking, again…It’ll be shortened soon. Until then, my July 2020 updates end where you see this message, in this format, again:

ANY post (or page) may be further edited (as in, condensed, or expanded, or both) after publishing. Blogger’s privilege!

I think as of July 30 (still working on it) the “Updates” section is about the length of a short post; perhaps 5,000 words..//LGH.

Know that for Pages on this blog (and you’re looking at my Front Page published January 27, 2018, as its title says), I cannot insert a “Read-More” (abbreviation) instruction. For “Posts” I can, but for “Pages” I cannot. I know the “html” for it, but WordPress somehow deactivates that instruction on its Pages. (<~Initial caps intentional there).

Meanwhile, do not be daunted by this 12,800-plus-(“and then some…”)-words Front Page! If you’re not up for reading that much at once, jump to my “For Current Posts” page (or any of those featured on the sidebar links) and come back here later. This page lays out and summarizes basic issues you’ll encounter in most posts. Because what I’m talking about, most people don’t, I include some examples and links, but it’s still an overview. By contrast, posts often detail a single aspect or organization — but my interest is in the context raised here.

Like any website’s front page, its purpose is to give an overview and reasons to read further.

The ‘Current Posts” page has 13 “sticky posts” and below it, most recent ones. I just finished shortening all their lead-ins July 28, 2020..//LGH (<~~that’s me)… Here’s that link:

SINCE DEC. 2019 and OTHER LATEST UPDATES TO THIS PAGE:

Obviously, we are mid-COVID-19/coronavirus pandemic justifying a major global economic re-boot and restructuring. The United States is already drenched with federally-funded behavioral modification stipulations, often executive-ordered, not legislatively; the pandemic just accelerated general public consent to yet more of it worldwide and more openly. In what facilities and exact circumstances any person can legally breathe mask-free or see others’ facial expressions — all of them (i.e., not wearing masks), in-person, face-to-face, i.e., “live” — is restructuring social lives and breaking many businesses — while making some — businesses. Sounds to me like some businesses were prepared in advance for such a situation, and there seem to have been some previous “drills” not quite so global… Test runs on population compliance and submission to “Health In All Policies” if you will, common-sense or not common-sense.

In the general pandemic and disruption, who’s STILL going to take time to question (or investigate) some of the planet’s largest companies (i.e., typically pharmaceutical) and drive for internationally-approved vaccines, travel restrictions, and as pervasive as possible “contact-tracing” technologies? I mean, besides me:

Gavi backed with $8.8bn to support immunization plans (June 17, 2020, by Ben Hargreaves in BioPharma Reporter © William Reed Media, Ltd.)

The U.S. and Gavi, the Vaccine Alliance (June 3, 2020, in KFF.org, no particular author shown; KFF stands for “Kaiser Family Foundation.” It’s “About Us” explains that you might be confused as it’s neither a foundation, nor a family foundation, nor associated with Kaiser Permanente… Yet the article here I’m quoting has about 26 footnotes, most of them simply from GAVI.org, a few more from KFF.org, and that’s about it. Uncritical, to say the least!):

Gavi, the Vaccine Alliance (Gavi) is an independent public-private partnership and multilateral funding mechanism that “save lives, reduce poverty, and protect the world against the threat of epidemics.”2 Created in 1999, Gavi was formally launched in January 2000.

KFF article doesn’t even recognize it’s an acronym and to be ALL CAPS (“GAVI”).

GAVI designated an international organization in 2006, according to IFFIm (International Finance Facility for Immunization, based in Geneva — it issues “Vaccine Bonds” specifically for GAVI… for major investment dividends. Donors include sovereign governments… targeted are children in lower- and middle-income countries. There’s been some controversy about the Gates’ intensity of vaccinating (so many, so early), but you’d not know it from these sources… And the US is a major supporter of the GAVI Alliance. https://iffim.org/about-iffim and its timeline: https://iffim.org/about-iffim/history

And I discovered it, and blogged it, in 2012, naming the grandiose plan, and some of its geographic/institutional organizations: “From Oxford to Harvard to D.C. … ” My context was illustrating the concept of giant nonprofit organizations — this happened to be one of the largest ones in Washington, D.C., so I took a closer look. From my other (most developed) blog — in fact from a March 31, 2020 Twitter thread when I reminded (readers) of my Oct. 25, 2012 post on the GAVI Alliance (thread includes direct link to that post; the thread has updated details on some of the companies and individuals I’d profiled in 2012):

I dn listen to all of these by @HowleyReporter but it’s a known how BillGates (Bill&Melinda) has been into vaccinations. Plus

(https://t.co/GAPfOa7vOW)

I blogged,@ 2blogs, the GAVI Alliance, Harvard-Oxford-DC connex & histories as a business interest. Vaccines: Do the math. https://t.co/hlybTc9tiR pic.twitter.com/T96Ab9xRfI— LetsGetHonest | Understand: #CAFCASS_AFCC_NCJFCJ (@LetUsGetHonest) March 31, 2020

https://platform.twitter.com/widgets.js

Or, a more direct link to my Oct. 25, 2012 post on a different blog, and I’m going to post some excerpts (Screen shots) from it:

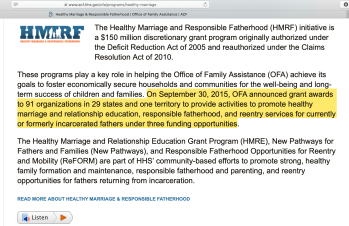

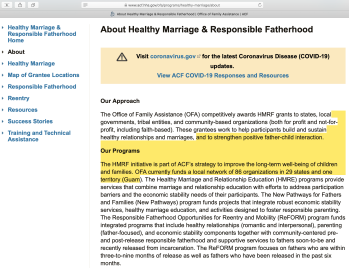

My about ten years of investigations and lived experiences (and dialogues with others over time) here, on this blog’s topics, includes some of the history of key USA federal agencies, such as the Department of “Health and Human Services” (that name dates to only 1980) which just so happens to be sponsoring programs intended to ALTER (create out-come based programming) and IMPACT family court systems which, along with most crimes on the person, are under state (not federal) jurisdiction in the USA. Below in this July 2020 update I’ve identified and shown examples (including images) of just two of these federal funding streams sponsoring such programs. Look for the first section with images.

Word has been seeping out of these, but for many years was systematically ignored by specific organizations. I just kept blogging, and naming organizations (and conferences, academics) etc. which covered it up, in between my own life crises and forced relocation events… I knew that they knew, often communicated directly asking why this known fact wasn’t being mentioned in the “reform efforts” and eventually, progressively continued documenting, by name, or quoting news articles, HOW this coverup was maintained in high places.

In recent years, I blogged “Health Systems Flush With Cash” *** (after Master Settlement Agreements involving state attorneys-general around anti-smoking or smoking-cessation campaigns). These billions in addition to billions involving major restructuring of the social services system, mid-1990s (i.e., “welfare reform’s” federal basic “block grants to states”) tend to end up in the same type of programming, particularly early childhood, psychological-educational curricula designed to, in effect, change people’s behavior. See my Tables of Contents pages (browse titles) for which posts.

***I found two earlier posts. The titles here are also active links:

A Health System Flush With Cash — because ‘Smoking Causes Cancer’ (1998 Tobacco Class Action Litigation MSA Payments, and Tobacco-Related Taxes Impact ‘in perpetuity’ on Systems Affecting Family Courts) ((Begun Early June; Publ. Aug. 7, 2019) post short-link ends “-a6m.” Currently 5,200 words, having just been shortened (split), but this one is still a bit complex. Following the funds has been made complex. Last update, Sunday, August 11, 2019.

Health Systems Still Flushing Cash into — WHERE is it going again? (About 20 Years AFTER Tobacco Master Settlement Agreements + Other Tobacco Tax Revenues like Prop 10 in California Propping Up Public/Private “First 5” Circuitry) [May-June, 2019, Published Sept. 18]. (Shortlink ending “-aaH,” and (unbelievably) under 5,000 words)

Somehow, this type of programming also ends up impacting the family court systems and the ability of domestic violence survivors with children (i.e.,. parents) of the female variety (yes, there are also survivors of the male variety…) to STAY separate, where minor children are involved. Switching legal and physical custody from the non-abusive to the abusive parent, this by and large guarantees that parent will continue coming back to court seeking justice until resources are exhausted, or it’s obviously just not safe to do so. Their continuing to come back to court feeds the rationale from the court-connected, private-interest organizations (of which this blog has much to say…) to demand yet further compromises and concessions IN DUE PROCESS and INDIVIDUAL LEGAL RIGHTS because of the over-burdened courts… Divide and conquer, it’s a game plan…

So in 2020 here, for people who’ve been through or are currently going through this type of personal shock, shakeups, and disenfranchisement from “normal” work, social, or family lives, by way of processes which they (typically) did not understand initially, while it may hit harder, experientially, they’ve been “prepped” for major lifestyle and socio/economic shakeups. My blog doesn’t alter those process, but does at least show the system logic behind the supposed dysfunction. It can (and certainly did for me, writing it) lessen the confusion and put observation back onto a more objective, factual basis.

I say “they,” but for this blogger, it’s a “we.”

Federally-funded (ongoing) programs intended to ALTER (create out-come based programming for)

and IMPACT family court systems which are legally under state control.

In other words, to influence by stealth, from afar.

Influence “from afar” and “by stealth” are contrary to basic forms of government in this country. Without the “stealth” aspect, the programs would not be so successfully (sic) churning family court cases and draining individual family lines’ resources, forcing more onto welfare, while justifying some of it in the name of reducing reliance on welfare …. The process is arrogant and disrespectful, but it has been instituted in large part because Family Courts exist — and they exist as a created turf because certain groups were determined that they should — not by popular or grassroots demand.

(One type is described here as if starting only in 2005, its program purposes however started in 1996 (just points of reference: the blog deals with what this actually represents in application, looks at specific grants and grantees in depth, which leads to even more “interesting” findings on who ends up with the money, and how well it is (or isn’t) accounted for to the public. Let alone the philosophical basis (rationale) for the programming.

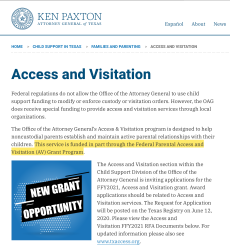

Another type is described here: I’ve provided a link to a Texas description admitting to the federal funding and announcing another line of grants for 2020. A sub-link explains how, “coronavirus or no coronavirus,” trial court orders regarding (access and visitation) regarding possession of the child and school attendance still apply!)

-

- The funding is federal, this website is Texas’ description of Access and Visitation (viewed July 28, 2020)

-

- “Access and Visitation and Coronavirus” in Texas: www.TXaccess.org

-

- “Access and Visitation and Coronavirus” in Texas: www.TXaccess.org

A_V grants 2020 announcement, at Attorney General of Texas (linked from TXaccess.org) ~Screen Shot 2020-07-29

Here’s the most recent Texas Office of Attorney General “Announcement” of availability of grants for access and visitation programs, briefly describing the federal authorization basis, what they may be used for (notice: typical activities occurring in family court hearings) and to whom –including local courts or government entities! — they may be distributed! The gender-neutral term “parent” is used, however, in practice this seems to work more effectively for one gender than the other; the grants were aimed at helping fathers in family courts. And of course, those providing the services…

Remaining unaware of those private (foundation-based) sponsors blending their strengths (such as freedom from the level or burden of taxation individuals, employees, face) with the federal governments policies expressed in their grants, and by policymakers) puts one at a disadvantage IN court and for CHANGING the same family courts where decision-making has routinely been resulting in what I call “roadkill.”

I say this as a domestic violence survivor, with children, whose first social-engineered-from-afar experience on obtaining legal intervention for protection (a.k.a. “to stay alive”) was being forcibly drop-kicked (in our city, across the street, for “mediation” via “Family Court Services”) where most of the basic protections IN that order were re-written, and the case was set for a custody battle involving, for the father and, ℅ the Local (county) Child Support Agency, a child support order, not something most abusers and perpetrators are naturally fond of, however low it’s set (and ours certainly was — lower than welfare payments at the time. There is an inherent system logic (though it’s completely immoral and unethical for a representative government) to the structure and operations of the family courts. **

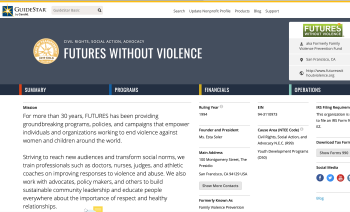

GUIDESTAR Futures w|o Violence Profile ~~Major source of funding is “government grants” (per its Forms 990) ~Screen Shot 2020-07-29. Guidestar shows its nine-digit “EIN#” (Employee Identification Number) to the right: #94311093, good to know for other database lookups…

SO, WHERE DO DOMESTIC VIOLENCE ORGANIZATIONS FIT IN, THEN?

Futures Without Violence’s profile at Guidestar reads:

(EIN# 94311093)

For more than 30 years, FUTURES has been providing groundbreaking programs, policies, and campaigns that empower individuals and organizations working to end violence against women and children around the world. Striving to reach new audiences and transform social norms, we train professionals such as doctors, nurses, judges, and athletic coaches on improving responses to violence and abuse. We also work with advocates, policy makers, and others to build sustainable community leadership and educate people everywhere about the importance of respect and healthy relationships. Our vision is a future without violence that provides education, safety, justice, and hope.

Nice spiel. I’ve read their tax returns (more than half gov’t-funded) and websites for years, attended one of their conferences (before they started taking “fatherhood” grants as well as “domestic violence prevention” grants), while still traumatized from overnight loss of children with almost no subsequent contact (not knowing, at the time, for who long that would continue) and having been accused of no crime — but falsely accused of the intent to commit one, for which apparent their father’s antidote was pre-emptive kidnapping. In the context of family courts, truth hardly mattered; the case was churned and his minimal child support payments on several thousands of dollar arrears immediately suspended (no seek-work order ever served), and the backbone — basic minimal requirements — of my ability to self-support in a profession I’d, WITHOUT legal intervention, managed to keep alive during abuse and quickly rebuild before even the very short civil protection order (a weak one) expired, was broken, overnight and that this’d be basically permanent, was made clear within the next year.

Searchable on this blog under its prior name “FVPF” or current one, “Futures Without Violence,” and many exhibits to go with.

Another (California) domestic violence nonprofit — this one, a member of the statewide coalitions network (certain type of federal funding under a 1984 Act of Congress), is I see (at least from its website), looking for a new Executive Director. At the bottom of the website, notice the usual disclaimer to anyone who might be desperately seeking help on-line: No Direct Services…. (the quote links to the website). Technical Assistance and Training seems to be the preference. “Dial this 800#.”

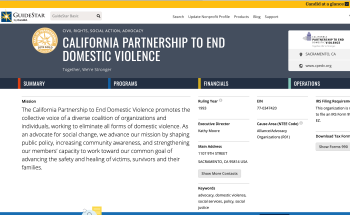

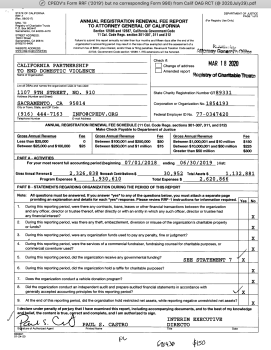

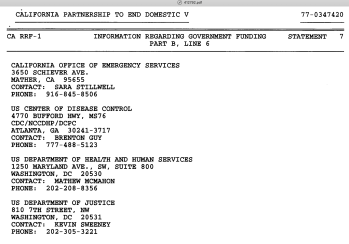

GUIDESTAR profile for CPEDV, EIN# 770347420 |Screen Shot 2020-07-29

The California Partnership to End Domestic Violence (“CPEDV”) incorporated 1993 in California as “California Alliance Against Domestic Violence,” changed its name in 2005 and had another organization (from Southern California which’d been around, so it said, since 1978) merge into it the same year. That is the only merger shown currently at the Secretary of State Level (“Business Entities Search”) under CPEDV, although elsewhere around the web, several mergers were mentioned.

Its reporting status with the state registry of charitable trusts [Shortlink here is also on my Twitter profile] is “Incomplete.” It’s far smaller than Futures, financially..

CPEDV’s “Guidestar” profile (see nearby image, its EIN# is 77-0347420) describes its mission:

The California Partnership to End Domestic Violence promotes the collective voice of a diverse coalition of organizations and individuals, working to eliminate all forms of domestic violence. As an advocate for social change, we advance our mission by shaping public policy, increasing community awareness, and strengthening our members’ capacity to work toward our common goal of advancing the safety and healing of victims, survivors and their families.

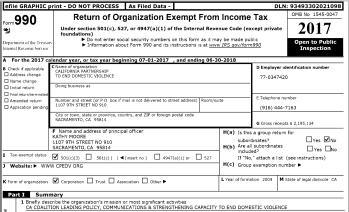

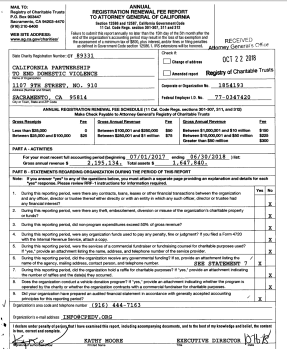

Four-image gallery above shows two state-level “RRFs” (“Registration Renewal Fee” — due annually) for CPEDV.org, and (the same second page for both) which government agencies (three federal and one state) gave it grants (though, not how much) as well as summary info. Notice two different signatures (change of leadership). The first image, taken from a Candid.org source, is the latest tax return I could find. More description in the next paragraph.

These TYPES of information I often look for, for any nonprofit (if it applies at the state level, and when tax-exempt and required to file at the federal, ALWAYS. Lookups take some time, but aren’t hard, and provide information that the organizations often are reluctant to provide. Most of all, they provide snapshots of what they’re telling government entities, and how compliant (or not) they are with filing requirements…

CPEDV here is NOT a large organization compared to many others (including those overtly “fatherhood-funded,” but it has a role to play and its filing habits are, er, ah — not up to code… View the latest tax return I could find, with their new interim executive director, Paul S. Castro (i.e., a man), was for FY2017 (Year ending June 30, 2018).

CPEDV’s tax return for FY 2018 (year ending June 30, 2019 — just over one full year ago) was due to both the IRS, and the State of California within 4.5 months of fiscal year end, but so far just is not found. It may not have been filed. Several older (as well as recent, shown above) returns I did find show a pattern of saying the organization was only formed in 2004 (it incorporated in 1993, may not have registered — as required by law — with the state charitable registry until over a dozen years later, 2006 (but hard to tell as that department hasn’t uploaded its registration form).

The organization is primarily (by a large share) government grants-funded. It’s located in the state capital (Sacramento), shows (currently) only ONE paid officer, an Executive Director, out of all, and that salary was $124K — about a third of the annual salary of Futures without Violence’s Esta Soler. CPEDV takes grants from FOUR diff’t government agencies (California requires entities to report which ones).

(I just looked four places — (1) its website (N/A), (2) Candid.org (which recently bought “Guidestar.org,”) (2) the above “Guidestar” profile still up, (3) the State of California’s Registry of Charitable Trusts (under Office of Attorney General, and (4) the IRS.gov database of tax-exempts, which sometimes holds a later year’s than does Candid.org (but this time, only showed CPEDV’s FY2016 return…)

This — and other– domestic (or family) violence nonprofit corporations and their leadership, occupy specific, planned places in the economic and media-campaign “biosphere” funded by both private and public. (See my sidebar). The established leadership of the profession of domestic violence advocacy in the United States as we know it now plays ignorant (but isn’t!) of the extent of oppositional [fatherhood.gov-style, access-visitation-programming] funding at the federal level, USA and internationally exported/imported as to policies. This effectively continues to coverup the tax-related details and extent of betrayal of their supposed beneficiaries, domestically.

Their career curves and salaries improve while ours, piecemeal, as parents, continue to be destroyed, although I notice that among some of the statewide coalitions, a single Executive Director may just not make that much.

Protecting children is a handy calling card for family court reformists to build support, but it’s an oxymoron — meaningless — as these family courts don’t even pretend to protect children. The private Illinois-domiciled judicial, custody evaluator, family lawyer, parenting coordinators, court administrators (and even some state supreme court justices) membership corporation, “Association of Family and Conciliation Courts” targeting professionals who particularly want access to vulnerable families and children (mottos such as “Kids Count On Us” for their newsletters, etc.) does pretend to protect children.

Within the USA the particular type(s) of federal funding they’re after also does, but the courts themselves don’t and family law itself doesn’t. Language about “domestic violence prevention” if anything, seems to be an politically correct gesture, no matter how much an overlap of those who abuse and batter adult parents with those who also abuse (and expose minor children nearby to witnessing) children.

So, regarding COVID-19 social and economic paradigm shifts of 2020, …

experiencing AND investigating all this ℅ attempting to exit dangerous relationships (for me, marriage) with children via the family court system, has been good preparation for the “new regime;” I was not blindsided or overly shocked: there were precedents, if not test-runs on mass-conditioning (social engineering to accept unproven conclusions) through mass-media, for replacing rule of law and national sovereignty (integrity, coherence) by rule of the massive state health enterprises.

The experience already exposed major fault lines in accountability, believability and reasons to trust our own government,primary institutions (and, it so happened with me as with many — not all — others, also) my own family of origin,who just “couldn’t handle” my stance on boundaries, safety, and insistence on being treated as what I am and always have been: a full-status, adult human being NOT in need of a life coach for self or children once I managed to have a batterer evicted from the household. With or without a resident male partner at home, and it so happens to be, a United States citizen, which comes with certain LEGAL rights– whether or not they are enforced locally or recognized by others. If anything, those leaving abusive relationships, which takes courage, persistence, and resourcefulness (as well as careful timing), ought to be treated respectfully.

Withholding key information about federal policy towards our kind is nothing of the sort, and this type of disrespect is both bipartisan and comes from both men and women in certain fields with vested interests in the family court systems and spin-off (ancillary) businesses to be run from them.

OTHER LINES OF INVESTIGATION AND REPORTING : (FYI, AS TO MY JULY, 2020 UPDATES)

I’m looking into starting a new blog on this pandemic and related pharmaceuticals topic. exploring some of the companies being offered vaccine development funding, so far. If only because it’s current, relevant, and interesting. Reading circular reasoning and predictable family court reform journalism (and socio-media responses to it) is getting old…

Now is a still a great time to take a closer look at how government operates from this point of view. As a U.S. citizen, I’ll be able to vote next November in a Presidential election (!!), but after my experiences in the California post-separation from domestic violence “family courts” (San Francisco Bay Area), I’m not waiting on a President, nor asking him (or, should it ever be a “her”) to “Fix the Family Courts” — and neither should you. Read this blog and learn why not — or continue floating downstream unaware of the currents below….

Where the page started, before this update:

ANY post (or page) may be further edited (as in, condensed, or expanded, or both) after publishing. Blogger’s privilege!

This Front Page’s last major update (Dec. 26-27, 2019) consisted of my creating a subsidiary page** to shorten it without losing major content developed over the years. A shorter Front Page makes the blog’s Sidebar, a roadmap to the blog and its various Tables of Contents, easier to find for people who use cell-phones, as opposed to laptops, tablets or other larger viewing devices. The Sidebar contains multi-part “Widgets.”

**My Front Page, Cont’d: The 75% Evicted from There to Here on Christmas Day, 2019.( short-link ending “PsBXH-bXr.”.

The “GO-TO:Current Posts” Widget holds (currently) Ten text boxes each featuring a post or page. The top box on this leads to the main “Posts Page” (but: sticky posts on top). My Dec. 21, 2019, post also lists the same ten text-boxes. (Access here, or as it’s the top sticky post just now, through that “Current Posts” link, or under that year, month, and date, through the sidebar’s calendar “Archives.”) On the same sidebar, below GO-TO:Current Posts” Widget (with its about ten textboxes) and a few other items, is another hand-crafted Widget I called “More Resources” widget holds a few more text boxes with other key post or pages. All this and more described further below..//LGH Dec. 29, 2019)

YOU ARE NOW READING:

Truth Fuels Flight, Lies Ensnare. Don’t Hang With, Serve (or Donate to) Tricksters or Their Targets. It’s a New Year — but there is STILL no excuse for abuse. // [Image captioned Jan. 2018, still true in 2019!]You are reading the home page of my WordPress blog. (WordPress uses the term “Front Page.”) Entering the basic url (internet address) “FamilyCourtMatters.org” always brings you here, to the top of this page. I have named this front page:

LGH Top Picks, Themes,** … and Why My Gravatar is a Blue Jay taking Flight. (Publ. Jan. 27, 2018; Updated Sept. and Dec. 26, 2019) about 12,400 words

For convenience, a somewhat shorter WordPress-generated shortlink to this page is “https://wp.me/PsBXH-8o0” (Case-sensitive: Capital “P” matters, ends in “zero” not a capital “O”). See next “Shortlink Shorthand” section

USING “SHORTLINK SHORTHAND” IS HELPFUL BUT COMPLETELY OPTIONAL, UNLESS YOU’RE QUOTING ME, WHICH SHOULD INCLUDE A LINK to SPECIFIC POST (or PAGE), not just the blog. I use it because as a blogger for me it’s not really optional.

WHY? With my typically LONG post titles, with now 840 posts and five dozen (60) pages, I often refer to previous writings within a new post, so having a shorthand helps me keep them straight. I also use short-links (you can, too) on Twitter.

The purpose of a blog is to have those points of reference; not to keep “re-inventing the wheel” on things already documented. They are useful…

Most bloggers don’t show the shortlinks. I don’t think most bloggers keep going for almost ten years, with original “feature-length” posts on their subject matter and because of that need to devise ways to keep track of and index them.

HOW I INDICATE SHORTLINKS (See Page Title above for an example, or sidebar widgets identifying posts or pages): Throughout the posts and on tables of contents, I now include right after the title, the final three characters (or for earliest posts, sometimes only two) of their respective short-links. Shortlinks for Pages read (start) “http://wp.me/PsBXH” with a capital “P” and for posts, the same except with a lower-case “p” “http://wp.me/psBXH-” but usually I will only display the post- or page-specific 3 characters that follow the “BXH”).

The Street Address/Apt. # Analogy: If Posts was an apartment building and Pages the next-door one, the case-sensitive PsBXH or psBXH, two DIFFERENT street addresses; those final character combos (also case-sensitive, alpha-numeric) would be specific apartment numbers. The “wp.me” is general domain (the town it’s in?); PsBXH or psBXH seems to represent this blog only, and within it (final three characters after the hyphen of each generated short-link) the post or page would represent an individual apartment/space. The further to the right a character is, as with most urls, the more specific it is.

(I flag whether to use PsBXH– or psBXH– by whether I call it a Page or a Post. There is no requirement to use any short-link (just clicking on the links provided will get you there), but if you wish to use them, as I do, know which is which). Most of my Table of Contents (posts) review this information. I have over ten times as many posts as I do pages, so the usual protocol would be lower-case “p” in “psBXH.” Most times I’ll just provide the three characters without any reminders if it’s a post. (In some earlier years’ posts I may not have adopted that standard yet). //LGH

BLOG NAVIGATION:

Content not visible on the sidebar is either on a post (most) or a page (fewer). Posts show up automatically a number of places on the blog; pages do not: the WordPress software treats and displays them differently. The posts are NOT just below this front page, but start on their own, separate designated page. The link (and page title) to browse current posts* is:

According to WordPress there is a Front Page and a Posts Page. The name of and an active link to that “Posts” page is directly above and on the sidebar, near the top, and on the image. Basically on this blog, you’re either on this Front (or “home”) page, on some part of the “current posts” page, or on the sidebar. It takes specific action (clicks) to get to individual pages or a list of them I may have created manually. The last ten posts also display automatically under the sidebar widget “Ten Most Recent LGH Posts.” I’ll say this again after the next insert.

Because pages aren’t added automatically, I compiled them (at a time when there were only 58) onto a Sticky Post under this name.

To the extent I add them to tables of contents, titles of and links to ‘Pages’ are there also, mixed in with the index of posts).

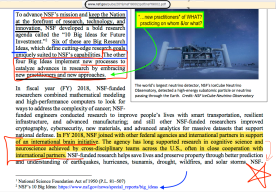

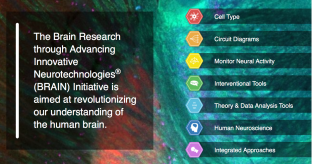

Oct. 2019 Mini-Section: National Science Foundation (“NSF”) (1950ff) & the BRAIN Initiative

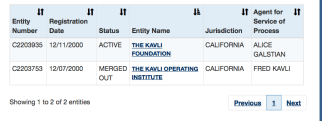

This content symbolizes “which way the winds are blowing.” It reports how I ran across some information (about the unique labeling of a part of government as a “foundation,” and uses the term “(Comprehensive) Annual Financial Report” as a government reports it. Reading through that ( C)AFR and picking up on a phrase “The BRAIN Initiative” I then searched it and read about a major financial contributor to it, the Norwegian-born physicist/inventor, Fred Kavli (1927-2013), whose biography and corporations I then looked up as entities, reading others’ bio blurbs of Kavli (usually recognizing him for the substantial contributions) and his corporations at the Secretary of State (California) Business Entities Search level.

WHY LEFT ON FRONT PAGE? If we want to understand the family (and conciliation) courts, we have to start understanding some of the private interests directing traffic through them and, in effect, running them, which entails understanding vocabulary and fact-checking (databases) for “business entities” and some of the games that get played with reporting some, not all of them under similar branding. That attention to detail pays off in the long run; avoiding facing up to the requirement for it, in the long run, hurts us all and costs more when we just don’t understand what’s going on….

A key part of the family court system is “bringing on the mental behavioral health specialists” which are enthusiastically embracing anything which might add respectable “science” connotations to their (often conflict-of-interest) spheres of work, as expert witnesses, custody evaluators, advocates, and those expounding on what is, or (more typically) what is NOT “domestic violence” “child abuse” etc. The United States federal government’s heavy investments into these fields has marked the culture of the courts and the culture of government this century and last century.

In fact, I looked up one trademarked phrase at the USPTO.gov Trademark Electronic Search Site (TESS). The same branch of government which registered it is also heavily involved in influencing the family court systems nationwide, from afar, especially as in the U.S.A., the state courts, not federal, have jurisdiction over marrige, divorce, custody and visitation, and child support matters. Some countries have a mixture of jurisdictions for family courts, including federal, but the USA does not.

So while condensing my front page by a LOT (Dec. 2019), I’m still leaving this segment in. There’s already another post published on it. Just another example of looking things up to notice “what’s up…” //LGH Dec. 26, 2019…

Oct. 2019 Mini-Section Added:

National Science Foundation (“NSF”) (1950ff) & the BRAIN Initiative

and Major Sponsor Kavli Foundation (source of wealth “Kavlico” 1962ff)…

and “Brain Research through Advancing Innovative Neurotechnologies® (BRAIN)” — Huh?”

A bonus section on the US-based National Science Foundation (“NSF”) (1950ff) & the BRAIN Initiative & sponsor Kavli Foundation (source of wealth “Kavlico” 1962ff and, of course, real estate investments) added to my Front Page Oct. 14, 2019, continued on a post published two days later (link at bottom of this section). (*Until Dec. 25, 2019, this section was a medium-light-blue background).

For something called “FOUNDATION” to be literally a part of government is unusual. Meanwhile, the National Academies of Science, which sounds more like part of government (compare: National Institutes of Health, which is: it’s under the US Dept. of Health and Human Services) represents a private non-profit, I learned. MORAL OF THE STORY: LOOK UP FIRST, EARLY, and OFTEN, which sector any name entity (or apparent entity) IS.

This section sprang from an informal conversation with a stranger asking about my work and my comments about the unreliability of databases reporting grants. His nonprofit was funded by the NSF which he knew (but at the time I did not) was part of government, i.e., “public” not a private tax-exempt corporation. So I looked for the NSF financials (which, being government would be in the form “CAFR” (Comprehensive Annual Financial Reports]. The NSF Is also well-written and a good example of what a CAFR looks like.

Fred Kavli (1927-2013) was a Norwegian-born physicist/inventor (?) who emigrated to Canada, then in the 1950s, the USA, and at some point becoming a naturalized American (USA presumably) citizen. He was obviously enterprising and able to connect with people as his company quickly got major contracts with (?) two major US auto manufacturers not long after. This naturally led to some major corporate profits, which in the US tax environment often lead to ways to reduce taxation on them, i.e., form some non-profits and/or invest (or have them own) real estate. I looked them up and quickly found some “anomalies” like one that simply failed to register when it should’ve.… Hmm..

There were TWO (Calif) now just ONE nonprofit ‘Kavli’ entities (the search filter was “Kavli”)

I discovered there even was a US-based (and an International) BRAIN initiative through reading the NSF AFR (“Annual Financial Report, in “CAFR” format; sometimes the “C” is not included in the entity’s [hyperlink] label); although indicators of coordinated language between university centers and nonprofits have shown up, and I have blogged them, in recent years, I’d not discovered this initiative or how official using the terminology had become, originating from the U.S. White House.

The financial input of a Fred Kavli and the “Kavli Foundation” (California-based, meaning I can track its financials better) was obviously well-loved (because of the philanthropic support to neuro- and nano-scientists in different countries, including the US). I see that Kavli filed almost simultaneously two California nonprofits: of these one NEVER registered with the State of California as a charitable trust (while handling millions of dollars of real estate assets, I’m talking over $20M, and paying a director, David H. Auston, at one point over $200K salary) before merging out of existence into the other one in 2006. The California Registry gave me an EIN# of the non-registered entity.

FYI, that’s inappropriate, if not unethical and illegal. It’s a definite “red flag” and indicator of the character of those founding and running the (combined) enterprise: One legit, one (apparently) illegitimate, both operations. until one covered its tracks by merging out of existence…(//LGH comment added during re-read, Dec. 2019 updates).

Obituary from the foundation (d. 2013) (<~~that’s a link) after listing a lifetime of accomplishments and philanthropy mentions he died of a rare form of cancer and is survived by two children (who have no names, nor does their mother, alive or dead) and “nine nephews and nieces” and, notably, little is said about his brother either.** This sometimes happens in families centered around one aggressive and successful member:

(** the subsidiary page profiling Fred Kavli makes frequent mention of his brothers’ influence, but still doesn’t name his own children, their mother, his own sisters, or his nephews//LGH Dec. 2019).

Immediately upon completing his studies in 1955 and receiving an engineering degree, he left for Canada and one year later came to the United States. After two years in California, he built upon his entrepreneurial spirit and experience and founded the Kavlico Corporation in Los Angeles in 1958** – later relocated to Moorpark, California. Under his leadership, the company would become one of the world’s largest suppliers of sensors for aeronautical, automotive and industrial applications with its products found in such landmark projects as the SR-71 Blackbird and the Space Shuttle.

**(The California Secretary of State says the year was 1962, not 1958….)

Fred Kavli contracted cholangiocarcinoma, a rare form of cancer, about a year ago and succumbed to complications due to surgeries. He is survived by two children, and nine nephews and nieces.

Those children had a mother somewhere, who is EITHER alive OR dead (there are only two options); so which is it, and why no associated timelines (like when). This is no normal obituary, and all are going along with it. . . .

What university or Kavli Institute at any university is going to say anything amiss about their benefactor, or, unlike the foundation, name the mother of his two children (ex-wife), his two children, or his brother as brother, mother, or sons/daughters? Judging by this announcement at at KICNano.cornelll.edu, no one, and it’s been six years now, almost… National Academy of Sciences (established 1863 by Charter, of Abraham Lincoln!) in appreciation of $10.5 Million Fred Kavli Endowment Fund in 2017, and quoting two Kavli and one NAS board member said:

“Fred Kavli had an insatiable curiosity about the world around him that underscored his appreciation and support of science and basic research,”*** said Rockell Hankin, Chairman of The Kavli Foundation and Kavli’s friend and associate for 40 years. “This gift aligns strongly with our Foundation’s mission because it will give the National Academy of Sciences broad discretion in recognizing and promoting outstanding science for the betterment of the nation and the world.”

“The National Academy of Sciences is the symbolic home for science in the United States,” said Robert W. Conn, President and Chief Executive Officer of The Kavli Foundation. “It’s entirely fitting that Fred Kavli’s lasting contributions to the advancement of science are honored in a way that will have meaningful impact for the Academy and the entire scientific enterprise.”

“Fred Kavli was a champion of basic research and the scientific process, and his legacy is felt widely throughout society,” said National Academy of Sciences President Marcia McNutt. “Through this generous gift, the NAS will build on that legacy by providing leadership on emerging issues for which science can inform effective policy and promote understanding of science.”

The Fred Kavli Endowment Fund will provide unrestricted funding to the NAS….

** I understand that basic science research is expensive and that money for it must come from somewhere, and typically has come from both government### and private sources. (### “government science & technology sponsorship” especially as spearheaded by the need to wage wars, plural and ALL that goes with it, including communications and transportation system fuels, explosives, health-related (medical efforts to stitch together broken or dying soldiers, to stop outbreaks of plagues which can come at times from such situations), and an army of mental health/psychological/psychiatric specialists to deal with such things created by wars and mass-genocides, such as: orphans and shell-shocked veterans with at times addictions.

And single mothers.

I just want to comment that many children trafficked through the family court system AFTER one parent reports domestic violence or abuse, whether into foster care or elsewhere (“reunification camps” for re-indoctrination in which parent to love equally with the other one — or instead of the other one) and/or worse (runaways, homeless who then are picked up by human traffickers), and some which do not survive the ordeal, or even a few years of “estranged spouse / bitter custody battles” when some parent “espouses” the “final solution” to getting even with (that bitch, or that bastard “ex” — more often the former when it comes to “roadkill”) — ALSO often had an insatiable curiosity about “the world around them” and while these neuro-brain-science-genetic researchers are searching for (and it’s been called that) the “Holy Grail of Neuroscience” and mapping the human brain “neuron by neuron” with a view to genetic modifications for the benefit of humanity, I wonder why so little curiosity about the financial relationships is encouraged among the same university institutes, or private ones — by making their financials available to the public.

I have some insatiable curiosity left still, and spent last few evenings [Oct., 2019 comment] looking up some of the other foundation activity of Rockell N. Hanken and the other Kavlico corporations and other Kavli Foundations (so far, that I’m aware of).

I appreciate the input of the NSF financial statements which are a good example of presenting such information for those who bother to look.

The stories are rarely so simple as presented for public relations purposes… I also know that Fred Kavli can NOT have been the only talented entrepreneur with curiosity about astroscience, neuroscience, and nanoscience. I would like to know more about how those original contracts with the clients (automotive, aerospace, etc.) that made the Kavlico millions he so closely controlled (sounds like it wasn’t public-traded, ever?) for forty years came to pass.

And I question any hero, however philanthropic, that cannot even name the other members of his own immediate family, or his offspring, or say anything remotely positive about them…and whose colleagues follow suit, thankful for the millions…. Much as I appreciate and am also interested in (though having no expertise whatsoever in) these new fields made possible with new technology in just the last few decades. . . .

CONTINUED at This Post, published Oct. 16, 2019:

BRAINInitiative.NIH.Gov (Google the term; many web domains will come up describing it, and President Obama’s 2013 launch of parts of it!).

Read (with the goal of understanding) Our Own Government’s Independent Agency Annual Financial Reports (at least parts with texts and colorful graphs) and “learn stuff.” Like NSF’s BRAIN Initiative, Its Big Ten Ideas, and Domestic | Foreign, Public | Private Revenue Sources. I just did…(Published Oct. 16, 2019) (short-link ends “-bie”, published at 8,700 words with extra section on the NAS and some intro).

(“B.R.A.I.N.” is an acronym for “Brain Research through Advancing Innovative Neurotechnologies® (BRAIN) — see nearby image (click image to enlarge if necessary or click the link in its caption). The emphasis is on the “neuro-technologies”)

[That post begins, with the nearby image and this text:]

The National Science Foundation (“NSF,” 1950ff, under President Truman) history ties in closely to Vannevar Bush. So does the history of Abt Associates (1965ff) as it intersects with Raytheon. In many ways the history of the NSF illuminates the history of the United States in the 20th Century. You can’t understand much of where we are now, and why, without some acquaintance with it.

//LGH Oct. 15, 2019.

Guess who owns the US Trademark (“Word Mark”) Brain Research through Advancing Innovative Neurotechnologies® (BRAIN) and when it was registered with the USPTO (Patent & Trademark Office)? The answers are on this pdf (and its title as uploaded here). Read the Goods & Services description carefully please! (Hint: the trademark is less than a decade old):

The (BRAIN)® trademark USPTO.gov Serial#86145003, Reg Aug 4 2015 owned by HHS! (Trademark Electronic Search System, or ‘TESS’) (searched,Printed 2019Dec26)(<~~pdfs on this blog typically require two clicks (at least from my usual viewing device: laptop: 1st one on the link; which’ll pull up a post and pdf title and a blank (gray-and-white striped, no images) page icon. Click on the page icon. Any links contained within the pdf usually remain active, but there are no internal links on this one. Just read the fine print!)//LGH Dec. 26, 2019

Back to previously-scheduled Front Page Navigation and “About This Blog”….

What’s “LGH” and/or “//LGH [date] “?

“LGH” is me, the blog administrator, and stands for my username “Let’s Get Honest.” (on Twitter it’s “@LetUsGetHonest)

I am the only poster and blog administrator on this blog, although most posts and pages are full of quotes of others I am referencing and responding to, with links, often images, with an emphasis on Show and Tell, not just “tell.”

Without my links, actual quotes and the images, readers would have me as a barrier to direct access (or more direct than typically given) to the very evidence — most of it — from which I came to the conclusions I’m posting on the blog. With them, seeing how (and where) someone else kept digging deeper exposes which verbal filters have been in place throughout social media, journalism on family court fiascoes and reforms, and what vital content they often filter out, or try to. Academic writings also filter out the same information, specifically and by type.

I wish other parents would adopt similar standards and take a much more critical stance towards repeating, reposting, blogging, and promoting others’ summaries of the overall ‘family court fiasco” situation. With every summary comes a proposed or implied solution, freely (re)circulated every time we individual parents (mother or fathers) simply do not bother to do our own homework on how our own governments (USA, UK, Canada, Australia, European bloc countries, and others**) work. **I mention those countries and regions because the family-court-connected organizations historically mingle heavily among Commonwealth nations (in association with the USA) more than even those on other continents.

Only closer looks at more types of evidence shows what these summaries tend to (strategically) omit, which then reveals over time and space, i.e., geographies, fields of operation, what the actual strategies more likely are, as opposed to the cause-based rhetoric that FRAMES most policymaking for sale to the public.

“…//LGH [date].” Because the blog’s been here so long, I sometimes update older posts, leaving the date signature. Otherwise “//LGH“ without a date is probably just taking credit for or further emphasizing something (sometimes an opinion, or an introduction to a new post)., to distinguish a sentence, comment, or insert from someone else being quoted. Sometimes I add “//LGH” to image annotations which might get re-posted on social media to claim my own work, or refer to this blog.

On Twitter, the username @LetsGetHonest was taken, so it’s “@LetUsGetHonest” (no contraction for “Let’s”). That is my theme. If there is to be family court reform, there must be an “us” and whoever that “us” is MUST be honest about key issues and have a legitimate agenda, at least for anything I would join, support, or promote. Lack of honesty systemwide ABOUT the system is a chronic, major issue. And I say “Let’s” because it should be by consent, not force, as in C’mon, people!! Wake up! Think about this! (or what you or others are saying).

Gravatars: I’ve only had two the entire time; the Flying Blue Jay is the one I’ve been using for several years now. I’ve now off-ramped the section explaining why that image, but left a footprint about it just a few inches below here (and again at the bottom where it used to be).

SEPT. 2019 UPDATED VERSION NOTES:

In January, 2018, I restructured this blog to have two home pages. One — this one — links to the other and has besides a LOT to say. From September 2-5, 2019, THIS HOME Page was being edited LIVE; large sections have been deleted or off-ramped, leaving for each removed section a “footprint” (link to destination post & connective text) . It’s a massive edit (i.e., haircut). Until revisions are fully done, flow between sections will be a bumpy though still an interesting ride, rather “Read.“

Suggestion: Read the top few sections: “LGH?” –clicking on the pdf links provided; “NAVIGATION IS SIMPLE,” “WHY A FLYING BLUE JAY GRAVATAR” and a few paragraphs into “ABOUT BLOG CONTENT” (major heading) until you see a large, blue centered “//LGH Sept. 5, 2019.” Most of the rest of the page is still “ABOUT BLOG CONTENT” and either a sample of it, or links to where you can find more of it (off-ramped sections which became new posts); but the section titles and footprints give an idea of content. At the very bottom with this revision, I reiterated a few key statements and posted some of my common hashtags in use on Twitter. The total word count now (which includes all titled links and any image captions) is about 13,200 words (<~Oct. 11, 2019 update).

Next two sections: Five short pdfs in two parts

(three in light-blue then two in tan (light-brown) background).

Just a media change to save vertical space on this page. All are short-burst statements “About this Blog” click to read!

For this Sept. 2019 “massive update” I wrote a few impromptu paragraphs of information I believe will help people understand the blog, and perhaps some basics it presents they may not have considered before. Those paragraphs are on the pdfs linked below. I’ve annotated one or two of them (an arrow or two) and added the filenames to each. All are short:

~~>>To upload a pdf, it’s my experience (on this blog), click on the link, then a second time on the blank “page icon” which will display underneath post (and image/filename) title to actually show pdf contents. These pdfs (three above, two more below) are not pictures but just a few paragraphs of text each.

[I see from the date& time stamps that this process took 45 minutes! Not including writing them the first time..]

WHO AM I (AND WHO AM I NOT?) LGH Front Page Impromptu ‘WHO AM I (and Who Am I NOT?) + Why Blog (1 para. only) | Screen Shot from FrontPage (Sept. 4, 2019) #1 of 1, this label

WHY “UNCOMMON ANALYSIS”? LGH FRONT PAGE Impromptu ‘Why Uncommon Analysis?’ | Screen Shot from Front Page (taken Sept. 4, 2019) #1 of 1, this label) …// Comments added during home page edit, Sept. 4, 2019. Click links (2nd click may be necessary on blank page icon to upload the pdf; true throughout the blog where the link is to any “pdf” as opposed to another website).

Vocabulary: Etymonline for adj. “Common” (add “un” to the search field for that definition). From 13th c. “common” was negatively used of women and criminals.

Navigation is simple, but in case there are questions about the layout, and how the sidebar sections (“widgets” group them into different parts) provide extra doorways into various posts or pages, here’s another description of the layout.

Now’s a good time to mention that I have a subsidiary front page as of December 26, 2019:

A large, subsidiary page containing at least half of Front Page’s contents, published Dec. 26, 2019 is at “My Front Page, Cont’d: The 75% Evicted from There to Here on Christmas Day, 2019. (<~Published Dec. 26, 2019 with the short-link ending “PsBXH-bXr .” It names this FRONT PAGE as its “parent.”). Shortened “footprints” here (previously off-ramped, named sections) remain on this page. I did this for a more utilitarian Front Page. Thanks for your patience meanwhile.//LGH Wednesday, Dec. 25, 2019, a.k.a. for some “Christmas.”

NAVIGATION, to the posts (& pages) [section off-ramped]

removed to My Front Page, Cont’d: The 75% Evicted from There to Here on Christmas Day, 2019. (<~Published Dec. 26, 2019 with the short-link ending “PsBXH-bXr .” . This colorful section with images has been up for almost two years now. I believe interested readers can figure it out, and it might be over-explanation. Look for images of my admin-dashboard with some bright yellow. The section is thorough, it has links but it’s about navigation not content. It’s been off-ramped.//Dec. 27, 2019.

[[End “NAVIGATION” discussion … Navigation’s really not that complicated…

the interjected material requires some background awareness, and is..

Why a Flying Blue Jay Gravatar:

(An extended section was removed from the bottom of this Front Page; I left one “footprint” which shows where it went a few inches below here; I repeat this link and some blue jay images (with different footprint text) as ties into the blog theme near the bottom, along with some of my commonly-used (at this point) Twitter hashtags.

“Blue jays will attack humans if they get too close to their nesting area.”

‘Cyanocitta Cristata’ | Blue Jays and Other Resourceful, Smart, Related Species and Their Habitats: (About my Gravatar Image) (LGH Front Page | ‘exported’ Sept. 4, 2019) (short-link ends “–aXL” and as exported under 2,500 words). This new post has now been published. The tag “Cyanocitta Cristata” will pull it up quickly (or see 2019 Table of Contents through Sept. 30).

Among many other admirable qualities of this blue jay, and related species, such as surviving man’s attempts to wipe out some of their cousins (related species), and being (take note), technically, a “songbird”… perhaps the designation “species” isn’t the best taxonomy, but if you never made it to the bottom of this home page before, visit this post. It relates the ornithological to the personal and concepts of habitat and territory to the family courts.

ABOUT BLOG CONTENT:

The rest of this page is an extended discussion, interrupted by several places showing where I’ve off-ramped sections–such as, to newly created posts, or if in an earlier revision of this page, to a page. In other words, where not just simply deleted, they were moved to another place on this blog which has a title, accompanied by a link. MOST of Sept. 2019 edits/off-ramps were to new posts.

Then my DECEMBER, 2019 revision, radically condensed the surrounding “footprints” and interim text, moving it to a subsidiary page (case-sensitive short-link ending “PsBXH-bXr”). In other words, I off-ramped a more complete version of this page, except without all the introductory material at the top.

RE: Limits to my Massive Front Page Update Early Sept., 2019: Other posts and current-events and developments in this field in rapid movement just now, that call for my focus and unique voice to be added to the mix of issue-based debates. … Also just last year (summer 2018 through summer 2019), I relocated outside [a.k.a. fled] California and so far maintained a stable lease (=predictable housing expenses), which puts me in an improved (though not yet fully free or safe) situation.

With that “phew, for a bit...” I’ve stayed a bit more active on Twitter and from following some of the leads on there, conscious of some of the parallel law reform and special-interest groups in other countries (Commonwealth ones, especially, that I have most access to information about).

Because of my increased activity on Twitter and outreach to others also concerned about current events, including some leaders of various reform movements or organizations involved in running/advising their (respective country’s) family courts, I no longer feel such a pressing need to constantly explain who I am and what I’m doing, in exhorting and demonstrating:

“DoTheDrilldowns!” “ReadMyLipsReadTheir990s!”**

(**Although I’ll be keeping those two phrases in circulation! I first started using them, as I recall, in 2012 on a footer in a forum dealing with Lackawanna County (and other nearby Counties and, generally) Pennsylvania networked family and juvenile-justice court-involved nonprofits).

(**<~IRS Forms 990 are USA-specific, but non-USA-residents concerned about their (and our) family court systems can (and I hope do) still learn much about system interconnectivity by reading some. Pick some of key organizations your country is probably dealing with as we speak. See below, see this blog (historically), see my Twitter account for some classic examples.)

//LGH Friday, Sept. 6, 2019.

IF you keep reading this front page,[[Or the Subsidiary Page off-ramping much of its content I’m creating Dec. 25, 2019; see top of this page or “My Front Page, Cont’d.: The 75% Evicted from There to Here on Christmas Day, 2019.(<~Shortlink ends “PsBXH-bXr,” published Dec. 26, 2019,]] expect to see major exposure to the field from an angle most advocates do not and cannot have because, unlike them, or volunteer individuals (on-line, off-line) who primarily associate on-line and ideologically with family court reform organizations or the professionals that run them, instead of operating as a nonprofit, I research the involved, court-connected, advocacy/reform-connected nonprofits and their funds. This provides access to less anecdotal, narrative/hearsay information and often highlights what is omitted from mainstream media looking for a theme or a story-line to tell, not a structural analysis of such a major, pervasive system within the US and other countries.

THE BLOG MOTTO IS HARD TO READ ON THE TOP: IT’S STILL (with page/post counts updated):

‘A Different Kind of Attention Develops Sound Judgment‘ | ‘Suppose I’m Right Here?‘ (@ March 23 & March 5, 2014). (Now) Holds 840 posts & nearly 60 pages of Public-Interest Investigative Blogging On These Matters Since 2009.

[Your] time spent upfront considering (immersion: looking up and looking at) some of these basics pays off efficiently in understanding how the systems actually work, not just understanding the ongoing obvious: what types of results are being spat out.

Understanding at least in part! how systems work and interact with each other (using vocabulary geared to show that) also cuts through much of the “spin” used to justify ongoing reforms based on unproven assumptions which take into account few, if any, of the entities: behind the reforms and conflcits-of-interest-involved among specific people (including judges) administering the courts and little to no awareness of how money flows through the system and is accounted for.

This type of understanding needs to move talk from amorphous, generic references (“budget” “resources” “funding”) to a direct consciousness of types A, B, C (etc.) of involved entities (entities can be government or private, among private, they can be tax-exempt or not, etc.) and using better words to reference them. Also a department or agency of some level of government is not an “entity.” Specific definitions (including where websites or reporting plays “catch/ID me if you can” on the actual entity involved) help get to the financing and the responsibility — that’s WHY it’s so important.

I realized over time that in effect, the federal government (Congress, our Executive Branch leadership and the Judicial Branch) in many ways are using nonprofits as a “front” for the certain agenda, when entire fields (such as the domestic or family violence “prevention” field) is primarily run by government-dependent nonprofits. How can such lack of independence stick up for the common people without committing fiscal suicide? Those dominating the field would not continue to exist without government support as legislated by Congress.

This is also true (USA) with the marriage/family/fatherhood values promotion so embedded within the delivery of social services (ANY type), especially welfare, foster care/adoptions and the child support enforcement system. Look under “Title IV” of the Social Security Act. Fatherhood promotion especially under Title IV-A & IV-D.

“A BUDGET IS NOT A BALANCE SHEET.” KEEP YOUR EYES ON THE ASSETS to LIABILITIES CHARACTERIZATION (and PERIPHERAL VISION ON THE RELATED ENTITIES AND RELATIONSHIPS BEING DEVELOPED WITH EACH ENTITY). THAT PHRASE IS ESPECIALLY TRUE WHEN IT COMES TO GOVERNMENT ENTITIES WHICH TEND TO ACCUMULATE LARGE, POOLED, INVESTMENT FUNDS. LEARN TO READ “CAFRS” AND WHAT ONE IS!

A classic example of amorphous, vague or derailing focus upon the financials is talking constantly “budget” and almost never “owned” or “investments in” revenue or income-producing assets. One quick cure for becoming over-impressed by this is to start reading tax returns — all the way through, lots of them, and (especially after 2008 for basic IRS Forms 990, notice the categories on Page I, Part I, a.k.a. “Summary.” Some of the organizations intent on re-arranging public resources are so “flush” they are showing up utterly careless about their own. (Some links to databases below under the “APA/ABA” section).

I cannot list here all the many insights which can be gathered by establishing a simple habit of looking for, then looking AT (literally, scrolling or paging through) tax returns and paying attention to their contents. Not necessarily every single line (many pages will often be blank) but becoming used to the categories and the concept that the supporting detail is supposed to actually support the figures on the front page. They come in a variety of flavors. Just check ’em out! This also will reveal — quickly, I assume — just how many gaps in accountability exist (or, if not exactly HOW many, THAT so many do exist) system-side.

My attempts and exhortations “Change the Conversation” [from cause-based to accounting-based, i.e., to develop an awareness of systems and operational structures) has been a key theme of the blog and practice, on-line. Different vocabulary introduces other concepts (not just re-branding for existing things) and a quick consciousness-raising about what is NOT being mentioned in the usual circles — the circles of reporting and advocacy and even legislators expressing outrage at poor performance (or lack of resources/oversight etc. for better performances) of the family court systems, overall.

In general, we are dealing with what might be called an “interlocking directorate” of existing financial and legal power bases, not above demanding that governments conform to their demand; nor are government entities, it develops, pushing back hard against private (basically, corporate) wealth — whether philanthropic or just “consultancy” based — demands it conform to protect private interests. It’s fine to talk about what is being circulated, but I find it helpful to talk about the networks through and by which it is circulated. Especially that we are now solidly in the internet age (and beyond), understanding terms like “content creation” and who owns which media (and when was the last time any major brands were re-sold, recombined, sold off, or purchased, etc.). Nonprofits organizations also run media campaigns around causes, ALL of which takes finances.

So . . . follow the financing! Sooner or later, it’ll come round back to the basic taxpayer or consumer and the issue of government accountability for those tax receipts.

[The next two, non-consecutive paragraphs in fine print, light-blue background may speak to some readers, but if the points of reference are so unclear/unfamiliar they do not, continue reading between and below them; the topics will come up again later. I realize how unfamiliar my approachs is and emphasized and repeat key points (basic principles of commonly censored information in the field) throughout the blog.]

I began doing those lookups originally seeking answers why certain topics were forbidden territory — there was a “Bermuda Triangle” surrounding select, specific, crucial and central topics. Individual comments from the sidelines (including from victims) on these topics disappeared into that mysterious unknown oblivion while, on the surface currents raged over the more popular themes. While I have been habitually looking up, more nonprofits continue to sprout up, but from which seeds is possible to determine by becoming familiar with the subterranean, less visible (in public debates) roots. With the silence, failure to even MENTION the topics by name for so long, people trawling the internet lacked search terms to lead to more information on them, which (as it turns out) suited the apparent agenda of the advocacy groups who chose not to deal with those topics. After years of blogging, some of the names are no longer sacred territory not to be spoken aloud on-line, however (from my observing activity on Twitter, or posts featuring the classic family court topics), in general, using a label doesn’t automatically indicate understanding of the substance or thing labeled. The essence is understood in context, and with specific identifiers which can be applied across a category.

My research includes closer looks at (I call them “drill-downs” of) :

- Nonprofits claiming advocacy/reform status of the family courts;

- Nonprofits (some, trade or professional associations) helping RUN them; nonprofits taking mandated-consumption (i.e., court-ordered) business referrals from (friends and colleagues in power) those courts — i.e., spinoff nonprofits.

- Other nonprofits which specialize in taking major federal grants year after year that many still seem unaware are indeed affecting family court outcomes in them (as intended to).

- For each cause, there can be an “umbrella” nonprofit and dozens (or, at times just a few) of similarly-named and themed nonprofits named after state or more local jurisdictions, and/or the subject matter.

Keeping in mind that the word “nonprofit” doesn’t mean “not profiting” — the term is somewhat of a dilemma, or contradiction in meaning. Basically, it means not taxed on its tax-exempt purpose profits. The term is really mis-leading unless understood (again, exposure to those tax returns and audited financial statements should help) in the context of what is and is not taxed, and how much.

Many nonprofits take federal (and/or other government) grants. I started researching the federal grantees (often but not always nonprofits) (as I recall) most extensively by following through with US Department of Health and Human Services (HHS or “DHHS”) grants TO the nonprofits, specific funding streams. Keeping in mind that the same grants stream could be going to both a private or a public (i.e., government entity — just a different one) at any time. Some are designated “federal grants TO STATES” but others are not.

Over time this expanded to looking at and evolving an informal vocabulary to categorize some of the private tax-exempt foundations partnering (often) with the federal, or state, governments to effect policy change intended to impact the family courts, custody out come, and domestic violence / child abuse and (not to forget:) child support issues and programs.

Next OFF-ramped section, re-titled (for its own post, started Dec. 2019), but a basic version also remains on my “subsidiary page” published Dec. 26).

Originally titled (next few lines):

For example:

THE GIANT “APA” and “ABA” TYPIFY THE PROBLEM WITH ACCOUNTABILITY

The Problem Distinguishing PUBLIC from PRIVATE GOVERNMENT (Activism to Direct Policy)

so as to hold Government Itself Accountable to the People.***

**I’ve had this section on the front page for months. I added the title because it’s come up repeatedly (connection of the APA and the ABA both with private organizations steering family court policies, which I often blog: i.e., AFCC, NCJFCJ, and others).

However as I review (some quick edits only) this Front Page in Dec., 2019, the nation is watching Impeachement Proceedings against the current President of the United States Donald S. Trump, with focus on the partisan nature, and another election looming in (Fall) 2020. People seem cognizant there is a challenge to the literal integrity of the United States itself and its Constitution, including the degree of interference in elections by foreign governments (invited or uninvited).

Yet this (challenge) has been going on in a more subterranean matter for DECADES in system after system NOT under direct jurisdiction of the U.S. Federal Governments, and through the family courts and associated supportive/administrative networks. Privatization is already WELL in place for almost every function of government and most levels of civil servants, it seems, which might have authority to direct — or re-direct — available funds.

[This “ABA/APA” Section is on my “Front Page, Cont’d.” subsidiary page, so I’m excising most of it now //LGH Dec. 26, 2019]

BELOW HERE:

An abbreviated “TOC” of Front Page Off-Ramped Posts.

(Mostly from the Sept. 2019 “haircut” updates. You’ll see these in my Table of Contents 2019 among the Sept. and Oct. post titles… Because this is an even larger edit, I have some introduction to it, which I’ll mark in this background color*****

The NEXT section contains more recent references and images to things I’m concerned about, long-term, and which I am watching on-line as they’ve developed and moved as standard “models” from the US (West Coast, East Coast, MidWest) to the United Kingdom and Australia (for starters), spearheaded by men (and women in the now established domestic violence profession) to ensure the “prevent domestic violence movement” is perpetuated with batterers intervention, involvement, and fatherhood-engagement/tools/ and perpetrator-outreach as central to it.

People, particularly those who have been batterered or abused (with or without their young) who do not follow the details and the money sponsoring the various trainings and technical assistance initiatives are likely to miss this. It seems to be sometimes the “industry’s” dirty laundry — just “unmentionable” when soliciting reform or more resources for violence prevention — and other times, its royal garments — boasted about on different websites with different intended audiences — like service providers or internal directives to the agency which still are accessible to the public (talking government entities, federal and/or state in the USA).

Core to this model is NOT talking about what I wrote this blog for — to talk about observable, documentable realities others more highly positioned in their respective fields — and their collective followers –refuse to. Who’s funding what, and why is the US funding both sides, it would seem, of a gender war played out especially in the family courts (but not only), and forcing the public (we are still a large country…) to FUND both sides of the ongoing conflict of interests…. I also talk extensively about what the “protective mothers” movement which I put in quotes because the term has become common place (it’s been so promoted) and I believe that real protective mothers would acknowledge what’s been going on for a few decades and talk with each other about it. However, talking about this doesn’t seem to match the chosen agenda of federalizing/standardizing and privatizing “best practices” in family courts which haven’t even been in existence that long, in the US.

NOTE: The version of this page with more “footprints” from the off-ramped Subsections 1 through 6, now exists on my new page, (My Front Page: The 75% Evicted from There to Here on Christmas Day, 2019.(<~case-sensitive shortlink ends “PsBXH-bXr” because it’s a Page, not a Post).

NOW THAT I’m PARTITIONING A LARGE CHUNK (versus small sections, individually) OF THIS POST: WARNING about Short-cutting Yourself (failure to visit that subsidiary page for a closer look)… Don’t kid yourself that reading just what’s below is enough. THE OFF-RAMPED posts listed below hold more more information, but so does that subsidiary page which adds more annotated/captioned images, explanation, which is not identical and which pulls them together. Some of this information seems to deal with criminal interests which are specialists in putting people OFF the trail (i.e., of the money to be made through the courts when blended with unaccountable public revenues AND unaccountable private ones). My writing/blogging interest is getting the at-large public back ON it as key to understanding the world we live in, and as more probable genuine leverage where there has been fraud or withholding of accounts — as opposed to “ineffective” or “not producing advertised results.” I am living proof it can be done, with diligence, persistence and basic common sense, and it can be done while under chronic personal duress.

I am every day, most days, reading tax returns of “advocacy” groups or websites claiming new breakthroughs and concerns for the entire nation (and/or world) to be trained and certified into replicating, especially when it comes to prevention of child abuse, domestic violence, poverty, evening out income disparities, and multiple nonprofits sychronized around the same media campaigns. Some days I am almost in shock at the findings — and hard put to publicize them when most people are synchronized with major media scandals.

I do drill-downs and post results; those visuals, annotated images, and narratives help connect the dots where simply listing titles and topics doesn’t. Ideally people will learn to do this themselves (when motivated and can carve out the time to focus on this INSTEAD of the social media sound-bytes, buzz-words and trying to build readership on social media recirculating the storytelling, cause-based rhetoric which censors both vocabulary concepts and basic operational concepts…)

This is serious subject matter, and it’s no time to go to sleep cognitively on understanding the reporting vehicles which connect public to private (and public to public|private to private) enterprises and just the level of “scam” that exists — NOW — in most “good” causes being philanthropically promoted by very rich and very famous people, often entrepreneurs whose products have changed the world. That doesn’t make them particularly ethical. It makes them entrepreneurs whose business models have succeeded resoundingly. And from what the tax returns and corporate filings are telling me — this is an entirely different mentality (caste-wise) which depends on most people to consider themselves mentally incompetent (or the alternative, to through association, consider themselves somehow wiser).

Learn to read more of the financials AND talk about them in their own terms — not “cause-based” PR terms. I’m not an expert, but I have made diligent progress over time, and developed an instinct (often rewarded when I follow through — and NOT before) for something “off,” whether or not I can get to it in the same week, month, or at times even year.

WHAT’s BELOW HERE SHOULD BE CONSIDERED MORE OF A “TABLE OF CONTENTS TO THE FRONT PAGE” THAN A FULL REPORT.

Thanks//LGH!

~ ~ | | ~ ~ | | ~ ~

(As written, these subsections (from the Sept. 2019 revisions) were not in numeric order, and on the subsidiary page, they are not=, but for simplicity in these December updates, I’m putting them in chrono order as labeled (not by date)… I also made their titles bold font blue, not maroon (as shown above the bulleted post titles with shortlinks)… The total is 6 Subsections; a few represent text shortened via condensing onto a pdf, one represents text added to an existing “summary” type post (available under Sidebar under “More Resources” Text widget). #5 is the Blue Jay Gravatar, showed in part above also.//LGH Dec. 27, 2019.

SUBSECTION #1: SEVERAL PARAGRAPHS & IMAGES MOVED 9/2/2019 TO:

- ‘From The Beginning, March 2009, FCM Has Been More About This Organization Than Me: (FrontPage Sept. 2019 Subsection #1) (short-link ends “-aUu”). This material dates to probably Dec. 2018.