Archive for the ‘Business Enterprise’ Category

Many of My Sidebar Widgets, Some Mostly Text, Others Mostly Links, Now Live Here [Published July 9, 2019].

Whether New to You or Just a Helpful Review, Many of My Sidebar Widgets Now Live Here

Post title: Many of My Sidebar Widgets, Some Mostly Text, Others Mostly Links, Now Live Here! [Published July 9, 2019].. (Case-sensitive short-link ends “-abt“). Was started June 27. This post may be revised (as may also be that sidebar) after first published. Current wordcount, almost 12,000 words (incl. those sidebar text widget contents).

Do I need to explain “Widget”?

I say “Widget” because WordPress Admin Dashboard does. Reviewing this may explain why the post looks the way it does.

This link describes the difference between (<~~cool website) “Widgets” and “Apps” — in reference more to cell phones but still helpful. The word “widget” in general seems to mean a “sort of thingie which can be interchanged with other thingies in our manufacturing or assembly process.”

SHARE THIS POST on...

Mix ‘n Match Misleading Terms: QIC, Coordinating Councils, Collaboratives and Commissions | Which Organizations Use Them | Which Parts of Government Control and/or Fund Them…(June 16, 2019)

The moral of this story? What’s my point in this post?

Mix’ n Match Misleading Terms: QIC, Coordinating Councils, Collaboratives and Commissions | Which Organizations Use Them | Which Parts of Government Control and/or Fund Them…(June 16, 2019) (Short-link ending “-9ZS.” About 15,000 words; about a third of them subject to “sudden post-publication re-allocation”),

(By definition, almost, any post this length needs about one-third, one-half or even two-thirds moved elsewhere! We’ll see! Tags to be added within 48 hours, I want to make sure tags naming nonprofits include any related EIN#s).

This post has been a long time in draft– in fact it stretched I see from Memorial Day in late May right up to Fathers’ Day mid-June, today. Finding a stopping point on endlessly connected issues, some of them disturbing, new-to-me examples of the same theme, was a challenge.

I’m writing these first paragraphs just before publishing. They are my personal expression and reactions, not the main substance, the arguments and supporting exhibits/illustrations below. I recommend just reading straight through them. It was written in one sitting, copyedited and developed some, developed sections off-ramped for further detailing.

My arguments begin with a Q&A “Think About It!” section in this color and after that, it’s showtime.

When you have read even further down and see these two images (together, my last ten posts from the sidebar), you are near to the starting point of this post…they will be on the right side.

When you have read even further down and see these two images (together, my last ten posts from the sidebar), you are near to the starting point of this post…they will be on the right side.

Some of the showtime introduces in detail (texts, links, images) certain off-ramped material which has gripped my attention. I am increasingly shocked by the blatant omission, misdirections, indications of new age terminology spun off more ancient forms of spirituality behind backers of “early childhood development,” some aspects of which definitely raise a few red-flag alerts on the touchy/feely healing-from-trauma involving children aspects. (Somatic Meditation, Integrative Manual Therapy Meditating with the Body®

In the Tibetan Buddhist tradition, the body is considered the gateway to enlightenment—to discover the body is to discover awareness—to uncover the most direct and effective path to profound spiritual transformation.

Commentary: That’s fine, but spiritual transformation should not be the goal of public policymaking aimed at institutions which will be and are sponsored by U.S. federal agencies. We have no official religion on this country — not “new age” not Buddhism or Hinduism, nor the Judaeo-Christian-Islamic-kind. Whether from the one aspect, sex and the body is “bad” except as religiously certified (and women are second-class citizens), or sex and the body are not only good, but a pathway to the divine, a debate that’s older than the Bible, I think the aspects of personal boundaries is a live issue, especially where children are involved with teachers and in association with university-based child care clinics or centers.

Neither viewpoint should be imposed upon or snuck in the back door of public-funded programs under the label of science — which, face it, public schools and Head Start / Early Head Start programs (along with many others) certainly are; in part because very religious people continue to flock towards situations where they can impact, influence, and mentor others: the fields of psychology, psychoanalysis and interfacing with traumatized adults and children attract people of such mindsets. The coaching/mentoring field is full of organizations and associations run by gurus and evangelists for their own world views. NOT my main concern in this situation, though. Lack of accountability and adequate terminology to track the accounts, is.

This topic came up (this time) along with FrameWorks Institute and Harvard University’s new Center on the Developing Child only because the Hemera Foundation, among its top investors (ranked by cumulative amounts of donations) was an unknown to me. Understandably — no website up, only formed in 2005, and registered outside the United States run by someone who’d spent much of her young and adult life also outside the U.S.

(Blog Admin/Writer) (I) decided on reviewing this years later to miniaturize the font for this section. It may affect photo layouts.//LGH))

Even without that fascinating, and due to Caroline E. Pfohl‘s (Wellesley, Wharton, London School of Economics) Hong-Kong connection, historically interesting aspect (relating to the Hemera Foundation incorporated 2007? in Bermuda (listed alpha, it’s Reg. # 40623, but you cannot view without log-in), but run by ‘Hemera Regnant, LLC’ in Boulder Colorado.

Ms. Pfohl at one point (? per Philanthropy Impact) was the daughter in law in a very wealthy and well-known Hong Kong family (and philanthropists) line and involved with the Robert H.N. Ho family foundation and was chairman of it until 2010 (See image nearby). Ms. Pfohl now seems married to “Dr. Reggie Ray” Dharma Ocean Institute director also in Boulder. || What about donations to fake entities (also discovered), ongoing involvements with public/private alliances (some even called that in their business names), all creating major spin?

Robert H.N. Ho Family Foundation 2010 Press release (Appointing successor to Chairman Caroline Pfohl-Ho, gives a bit of foundation context. See also Hemera Fndtn (Bermuda-based, U.S. Registered agent via an LLC in Boulder, Colorado is Ms. Pfohl who seems now re-married. Hemera Foundation (previously unknown to me) listed as a top funder at Harvard University’s Center for the Developing Child, established in early 2000s.

**See pp. 27-28 of “Investing in Bermuda, A Piece of Paradise | Opportunity for Foreign Investors” which specifically names Hemera Foundation along with Atlantic Philanthropies and others as among those helping start the Bermuda Community Foundation formed during the 2008 financial crisis, and the inset on the next page about how, conveniently, how some charities need not register in Bermuda. Or, (2015) (“Zero to Three in Bermuda” (Hemera working through that Bermuda Community Foundation, with a BSMART1 Foundation: brain science, early neurodevelopment, etc.)) Hemera Foundation also contributing to Harvard University’s Center mentioned below.

“Hemera” is the name of a Greek goddess of the day, with her brother “Aether” god of the light, both of them sons of night and darkness. (Source: GreekLegendsandMyths.com) They are said to pre-date the gods of the Pantheon (Mt. Olympus, etc.). Interesting choice for a foundation name.

Here’s a quote** from that “showtime” on off-ramped material section, below the first Q&A “Think About It!” blue section on this post and borrowing (bright-yellow highlit) a question from it. Definitely one to keep an eye on, which is hard because of all the non-entities citing their famous donors, and at least one of their famous donors, primarily a grantmaking (front) based in Kansas with strong Buffet family flavoring (plus, as typical in the field, Annie E. Casey Foundation and others).

SHARE THIS POST on...

What’s ARKANSAS** got to do with H.Con.Res.72? (Passed 2018, U.S. Congress Senses that State Courts Sorta Oughter Better Prioritize Child Safety in (and IMPROVE) Custody and Visitation Adjudications)(Published May 26, 2019)

This post was promised earlier in a sort of mini-series of posts published in early May, 2019. It has been referenced in some of them. Here’s that follow-through.

My revision history shows last viewed or saved May 19, then May 1, except now (May 26) adding a PREFACE with (1) a short section with link to some my previous statements why I as a domestic violence and family court survivor (and mother) oppose H.Con.Res.72, and the people who have let Congress off so easily without exposing the networked interests in waging continued war against women and for men, classic “divide-and-conquer” methodology, to the point that no one, essentially, seems to be following the accounting trails, structured similarly, funding both sides of that “war.” (2) some connecting comments (that happen to relate to more recent examples I’ve seen) and (3) what I consider related, a section on BCCI, seeing as this topic includes a state where that played a key role in the 1970s, 1980s, and 1990s — and in who’s been U.S. Presidents since.

Today’s PREFACE is about one-quarter of the total post written almost a month earlier. At that time, I drilled down only until bogged down on the subject matter of the post title: “What’s ARKANSAS got to do with it?” Overall, not just in this region, the situation is disturbing and alarming.

What’s such a powerful person** with Clinton Administration connections (like his father) doing on the board of such a tiny nonprofit (and if the topic is that important, why is it so tiny — and why is its own website so incomplete? (Naming only one of two related entities that are obviously connected — as a look at tax returns quickly shows)… [**Nelson Edward Peacock]. [<~~ that ‘Legistorm’ bio includes Congressional and Lobbyist Involvements, including for (I just noticed) “BSNF Railways” in 28 states and three Canadian provinces; just bought by, or became a subsidiary of, Berkshire Hathaway (Warren Buffett) in 2010] What’s with the Wal-Mart heirs in that area seeking to regionalize it across the state border by way of the Urban Land Institute and other public/private projects which just cannot be tracked, really, although they certainly can be advertised.

In fact, what’s with Arkansas?

See my Sticky (now about 3rd from the top of this blog) post called:

Screenshot from my May 2, 2018 Sticky Post, screenshot of my section with reasons why I object to H.Con.Res.72. Annotated image to lower left shown nearby (for May 26, 2019 new post on Arkansas & H.Con.Res.72

On that link, for my take on this Resolution, scroll down (considerably) to a portion that looks like this: (see screenshot to right with two enclosed images. I realize they’re too small to read; annotated image and its caption inset lower right also provided below-left, along with reasons (3) and (4) (in green) for my objections:

{Pls. Click Image to Enlarge if needed} HouseResolutn72@Congress’gov (115thCongress, Bill Summary), with my indignant annotations. Proofreading Correctn to Top Comment: “politically viable” should be “politically VOLATILE.” (my “word-o”|uncorrected it reverses my intended meaning!). The pink underline (mid-image) should also cover “perpetrators” on following line, to the end of that sentence.

(3) Seeks to create more specialized professionals and pay or incentivize them with more public funds to detect and address abuse (see annotated image below). As did the Family Court Enhancement Project already….

and,

(4) Continues an existing uniform, unilateral derailment of any purposeful consideration of the economics | built-in-by-design conflicts of interest typical of a typical family court jurisdiction.

SHARE THIS POST on...

Women Judges still form Funky-filing Nonprofits to Run Fatherhood Programs | Men Judges still form Countywide DVCC’s + Obfuscate the Funding. Santa Clara County, CA (Six Years Later)

Women Judges still form (funky-filing) Nonprofits to Run Fatherhood Programs | Men Judges still form Countywide DVCC’s + Obfuscate the Funding. Santa Clara County, CA (Six Years Later) (short-link ends “-9YW” and about 10,000 words long. Post written May 20-25, 2019, updated May 26).

“PREFACE”

I’m publishing this post “as-is” because one cannot squish too much documentation into one place. There are more things I could say or links include, but this post “as is” says plenty.

I like to triple-check statements; there are one or two I haven’t yet, regarding research done six years ago. In double- and triple-checking, more information and more understanding of the existing connections comes into focus for me as a blogger, which I then naturally want to reference or summarize.

Without a more direct, immediate, known (and prospectively more interactive) audience for this blog, I cannot put more days into it.

Most people I know do NOT go around reading business entity filings and tax returns — I do. I do it ALL THE TIME. Over time this has also developed a general, mental database of key organizations, awareness (generally) of how they tend to spin off over time, or sometimes I can catch a new one as it’s forming, or has just formed.

The issue, however, is with whom to talk about it. Those involved, even if as volunteers or volunteer board members, in the networked organizations are generally already committed to their ongoing operations; those not involved and often not local (as the networks are coordinated nationally and at times internationally) in my experience (and with current connections) either not alert enough to even acknowledge the importance of reading business entity filings and tax returns as indicators of the values of the organization’s leadership, or are overwhelmed possibly with their own court cases involving still-minor children.

Those who’ve aged out if not already aligned with the (usual) family court reform group loose (or tight) coalitions tend to want their own lives back, or just not to be bothered. Those who haven’t directly experienced this firsthand (which is to say, those “on the sidelines”) generally seem to fall along the usual religious (religious or not), political (left or right persuasion) dividing lines and not about to cross them seriously, either.

Those involved, even if as volunteers or volunteer board members, in the networked organizations in many cases, (specifically, as mentioned on this post, as mentioned on most in the blog), will be also judges, or retired judges — and other court-connected professionals continuing to push programming put in effect in the 1970s, 1980s, 1990s, first decade of 2000s, and now in the second decade of the 2000s fast approaching its end. These programs will also be pushed, promoted and if possible perpetuated, regardless of which political party is in power, or who is U.S. President. It’s an ECONOMIC matter.

I could post more tax returns or charitable, corporate registrations on this post as simple links (without the images). I especially could post EVEN more on the connection between the “woman-judge-formed nonprofit” and “MACSA,” and recent findings on the (very much related) background and filing habits of the local (county) fatherhood collaborative, which I have seen and saved much of it as computer files or images, but it will not all fit in a single post. The connections between MACSA, the nonprofit, and the county probation department (and with it, under “fatherhood collaboratives” also county-based) speak loudly as to the origins of that nonprofit.

(MACSA = Mexican American Community Services Association: Bay Area News Group March 6, 2014 article describes its woes, most of them involving improper handling of financials, IRS-revoked nonprofit status for non-filing (with the local DA’s office having seized its paperwork possibly related). Notice the years..)

I have one or two statements I’d like to, and will try to, triple-check (specifically the fiscal agent connection between the DVIC and DVCC referenced below), but as a reminder, no matter how formal it may “feel,” a blog is an INformal medium, and I am a volunteer investigative blogger all these years. Last year I left one state and relocated to another for a fresh start, which requires major energy still, and I’m recently, technically speaking, a senior, and have always been a mother, whether or not permitted to function as one over the years.

MACSA (The Mexican American Community Services Agency) existed 1966-2013 | CalEntity C0512046, Status ‘Dissolved’ per California Secretary of State’s Business Entity Search, re-checked in May 2019

The situations I’m speaking of in this post are typical, present multiple red flags, and should be noted, and watched. It may take some time to become familiar with the setup, the terminology and where to look filings up, but that can be learned, and look-ups, up to a certain point, can be done.

I think the blog’s limits structurally on how it can deliver what I see needs to be delivered, is reaching its boundaries and think constantly about what other communication and message-delivery options exist that I could remain involved in — or find an ethically and intellectually (diligent fact-checker) responsible person or group of people to delegate them to. //LGH May 25, 2019.

Originally, my purpose on this post was to preserve the text and story within a sidebar widget on this topic; administratively I needed it removed from the bottom right sidebar. That text is below, in a narrower column, and beneath it a few footnotes from my substantial (extensive / long) updates on the top.

These topics are still relevant, and this is in part a re-statement of them (followed by the preserved text).

-

- MACSA (written out) in San Jose: The IRS tax-exempt organization search shows when it became “status revoked” (2012)

-

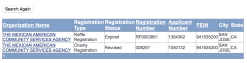

- MACSA (bottom row is the entity, top, the raffle only), Status “Revoked” (Details show, since 2014).

-

- MACSA tax returns by EIN# search only go up through 2009 (but look at the size in $$ assets) and be aware much of that was public funding.

(Above image gallery: I found a MACSA EIN# 941635200 from the IRS which also noted it was revoked in 2012. I see three tax returns from FY2007-2009 showing several million dollars’ worth of assets. It eventually registered as a charity in California; the “Details” page are full of demands for missing or incomplete information, and notices of ITS (Intent To Suspend). To view, you can repeat the search, or (for a snapshot as of several years past “Revoked” status, click “MACSA California Registry of Charitable Trusts | Details“~~>MACSA (TheMexicanAmericanCommunityServicesAgency) CalEntity 512046, EIN#941635200 CalifOAG Charity (Status ‘Revoked’ 2014ff) Details (RelatedDox Links Still Active) @ 2019May link added 5/26/2019. Note: for pdfs (vs. plain images) on this blog, you must first click the link to see page with blog & post title and beneath it a small blank page icon, then click on the pdf icon to load the document. Bonus Attached Info: When pdfs are printouts of California Registry of Charitable Trust “Details” (any entity), scroll down below ‘Schedule” to the bottom of the resulting document: any links under “Related Documents” for the filing entity should still be viewable by clocking on them.) (The California OAG RCT of course at any time may change how it loads or the user interface on this database in which case some of the above notations may not apply).

The latest charity renewal for MACSA (for FYE 2008) shows that about HALF its $10M revenues were from government sources. It was status “Revoked” since 2014 (as a California Charity) and as a tax-exempt organization, 2012 — however as late as June 2017 (see colorful image above) it was being positively referenced in association with a Santa Clara County Fatherhood Collaborative — from a University of Texas-Austin, LBJ School of Public Affairs, Child and Family Research Partnership (CFRP) in a “Policy Brief.” That colorfully annotated image and link to it above comes up again soon, below.)

This post references Santa Clara County “Domestic Violence Intervention Collaborative” (<~~DVIC is a nonprofit | “DVCC” is a named “Coordinating Council” under the county’s “Office of Women’s Policy” (OWP created in 1998)) and through it, at that level one of just two ex-judges* I just featured in the last post, Classic AFCC Combos, Collaborations, and Commonalities (Ret’d California Judge/Consultant Leonard P. Edwards, Texas Supreme Court Justice Debra H. Lehrmann) and What’s WITH Middletown, Connecticut? . *He’s ex-judge because he’s retired, she’s ex-judge now only because a state supreme court justice, is no longer called “judge.

That nonprofit DVIC wasn’t the main focus of this post but arose in connection with another nonprofit, referenced in the title which I am now reminded (through revisiting) originally framed its reason for existing as family violence prevention, too.

The relationship of the DVIC (nonprofit) to the DVCC (coordinating council) is a little complicated. I think that the DVIC was the fiscal agent for the DVCC, although with one being county-office-associated and the other not, that doesn’t even make sense.

The concept of “coordinating councils” isn’t complex, but I wonder how well the significance is generally understood; they’ve been around in reference to different subject matters, and when it comes to “DV” seem to take on a specific flavor.

The post title alone doesn’t reflect also how Judge Edwards’ “consultancy” was at the highest state level, but the post does. Before retirement in Santa Clara County, and again, he was and probably still is active in at least three very controlling and significant membership associations — AFCC, NCJFCJ and (as to child welfare), NACC.

That retired Judge Leonard P. Edwards founded the Santa Clara County Domestic Violence Coordinating Council (DVCC) is stated in this glowing commendation from California CASA Association mentioned among other accomplishments: he was also the first juvenile court judge to receive a special award from (yet another nonprofit, PRIVATE, association, the “NCSC”) in 2004, as the NCJFCJ’s publication reminded readers in 2005 when reprinting a 1992 article from Judge Edwards on “the Role of the Juvenile Court Judge.”

NCSC = National Center on State Courts is not the major focus here, but I’ve posted on it (June 30, 2017, split off from Oct., 2014, “Do You Know Your: NGA, NCSC, NCSL, NCSEA, NCJFCJ, NCCD, NACC, and NASMHPD, not to mention ICMA?) and often call attention to it.

Read the rest of this entry »

SHARE THIS POST on...

Smoking Cessation/Tobacco Control Litigation I See Is By Design Guaranteed, (Like Domestic Violence Prevention and Services) To Continue Incessantly. Meanwhile, a Wide Swath of Northern California Is Smoke-Filled and Lit Up, But Not by Tobacco. (October Local News and Blog Updates)

__

Smoking Cessation/Tobacco Control Litigation I See Is By Design Guaranteed, (Like Domestic Violence Prevention and Services) To Continue Incessantly. Meanwhile, a Wide Swath of Northern Cali fornia Is Smoke-Filled and Lit Up, But Not by Tobacco. (October Local News and Blog Updates) (case-sensitive short-link ending “-7Lp”)

Post Technicalities: Tags may be added later. After over a week reviewing and supplementing this post, I’ve decided to “punt” (publish). It MIGHT also be split later, but the sections on exploring national DV networking over the years (from key organizations’ narratives) and “Health as an Asset,” an academy (“ABIS”) globally networking under the “Chatham House Rule” (basically, anonymity)(which brings the topic to the RIIA / Royal Institute of International Affairs in London and its historic intentions, as expressed in its founding documents) towards the bottom, which has a sequel, actually belong together. And this still IS “Domestic Violence Awareness Month,” for what that’s worth, in the USA..so I took a closer look at how certain organizations like to collaborate for a unified voice, and consequences of that collaboration, down the road a few decades….//LGH, Oct. 20, 2017

Or, you could call this “October Local & Posts-in-the-Pipeline Update” which is how it started out, attached to another post started earlier I’d hoped to publish with just a brief update.

As my About Holidays / Personal Backdrop” (posted Oct. 10)** says, I took a brief, about half-month, pause while handling (different kind of writing required) personal things and am now catching up on some of the posts already in the “pipeline” referencing, basically and most recently the themes of (a) Big Tobacco Litigation/Smoking Cessation Control (Public policy) Efforts and (b) The Problems with Problem-solving Courts (“Collaborative Justice”), which includes the development and implementation nationwide of family courts, too. [** after next few reminder images…]

I wrote about an East Coast/West Coast connection involving one government sub-sector (Administrative Office of the Courts, under the Judicial Council of California, the ruling body of the Judicial Branch in the state) with an improperly named non-entity (it’s not its own legal business OR government entity) — the “Center for Court Innovation” in New York. You will not find it registered under that name on CharitiesNYS.com or Business Entity search, and so far as I know, it’s not a trade name of some registered entity — because the EIN# associated with it, generally speaking, belongs to a private foundation, “Fund for the City of New York.”

Four logos show sponsorship (not membership) of the Executive Session for State Court Leaders” (click image to enlarge, for fine-print commentary) as I recall. Only 1 logo represents part of government (BJA is under the USDOJ) directly; the other 3 (including Harvard) count as “tax-exempt, privately controlled entities” even though the NCSC Board will have public officials on it.

I talked about how organizations like the NCSC got involved and discovered yet two more (subsequent to “The California Story” published in 2005) 501©3s promoting the same “collaborative justice” concept, keying off the concept of drug courts:

Fund for City of New York is one-half (the Private) half of the Public/Private (agreement, project, collaboration — whoever it’s defined) comprising the “Center for Court Innovation”. Look at the affiliations of the Board members — former NY Attorney General, Designer of the World Trade Center, Adm. Judge of the City of NY…!

(There’s also a foundation to go with this one).

**(The rest of that title, the same link as just given above: “….Speaking Personally (Personal Backdrop to Post-PRWORA Social Policy towards Women Who ~Just Say No!~ to Abuse and Proceed in Misplaced Belief They can actually Exit it) [started Sept. 18, Publ. Oct. 9, 2017, see also Collaborative Justice post/page].”(ends “-7AD”)

The other “Collaborative Justice” non-profit showing clear judicial membership and sponsorship, as well as an MSW involved in “Children and Family Futures.” I won’t say more on that in this post, just pointing out that the process seems never-ending:

CCJCF-related, image series labeled: “Search for CCJCF President turned up EARLY Annual Rpt (Final Draft) WITH EIN# attached and its Significant Others (Judge Lynn Duryees, Peggy Hora)”

[Image may be added here post-publication, can’t locate a certain annotated one just now. It may be on the bottom of the related page]

One post in the pipeline taken from part (b) above again (“Governance, the Final Frontier,” now in draft, full title further below) reminded me of how early (how long ago) I’d realized that the “powers that be” within the domestic violence field obtained, and maintained, control over the field with an agenda to “therapize” the nation’s language of crime and consequences under the health, social science, and behavioral modification treatment [“therapeutic jurisprudence” and other concepts] paradigm — while still claiming to be tough on crime and domestic violence. And that one of the ways of doing this to mimic popular, grassroots demand from multiple seemingly diverse platforms (organizations) was having already-established tax-exempt foundations first internally sponsor projects, then spin off the projects off into more 501©3s (nonprofits) which, while the names may be new, the world view, personnel, response to the problems and practice of letting philanthropists run government or organize with intent to run it, is not. In other words, by setting up interconnected nonprofits collectively run by people of, except perhaps subject/topic focus area, the same general persuasion, having been so persuaded possibly in part because alternate viewpoints or alternate solutions to the problem were out-funded, and out-maneuvered.

[Phrases above in this color were added long after the original paragraph; it this is too much overexplaining, read around them.]

Both this post and the one whose title shows next, linked from the “Collaborative Justice/Problem-solving Courts” page, should be published today, Oct. 20, 2017, or within 48 hours of each other. (That “today” date kept getting moved back as I continued adding to the top part of this post!) The one you’re reading now will be published first.

I’ll repeat that link near the bottom of this post.

VERY early on, assumptions about WHICH are the KEY POINTS IN (foundational to) any new field or regime (for the DV field, that treatments and interventions, such as batterers’ intervention, or supervised visitation, mandatory mediation, parent education, etc.) become foundational, basic for that new field or regime’s claims to even BEING a field of practice or a new profession or area of professional practice (example: “fatherhood” or “domestic violence PREVENTION”). Assumptions and omissions of relevant information which might speak against that selection of points get “baked-into the infrastructure and system” (including to its literature and downloadable curricula, webinars, etc.) as entrenched positions, and continually a part of whatever solution is chosen.

This proprietary, linguistic control makes later protest by people harmed by such policies, even if among the classes the policies are allegedly representing in the first place — for example, survivors of domestic violence, and/or child abuse who, with full information up front might have made different choices in picking their court battles, or how and how hard to fight back once they were dragged into one — an even heavier burden and uphill battle. The public is fed information leading (or at least encouraging) readers/viewers to believe (until personally involved) that “the experts are on it,” so where there’s evidence to the contrary, maybe it was just the family’s problem, or one of the family members.’ Or a rogue judge, or a local problem..

After all, don’t we hear about domestic violence on TV shows, sometimes in a movie, in ads, and after headlines involving recent roadkill, perhaps from experts on one of the major organizations’ comments?

A SHORT SECTION ON THIS, FOLLOWED BY MORE ON THE NETWORKS:

Who can even find the long-standing/oft-quoted SF Domestic Violence Consortium? What does its spokesperson do for a living? Take tax-free donations (It’s not an incorporated entity, but its “Executive Director” maintains apparently a speed-dial on some local news media with each new domestic violence vitality — year after year — or otherwise disaster that has potential for making national news too.

Looking at this one, I also took a quick re-view of California’s registered and still active known major DV organizations, including (but not posted here) the “NNEDV.” I also added a section in which one of the networked entities did us (belatedly) a courtesy summary of the networks themselves, nationally, that is. Recommendation? Pretend this is a conversation, and just deal with its about 15,000 words as they come up. When you see a new section coming up, so be it, and remember that some of the material that inspired a post may (in my writing style) still end up closer to the bottom, while what’s in between is, to say the least, “illuminating.”….

Read the rest of this entry »

SHARE THIS POST on...

About Holidays, Speaking Personally (Personal Backdrop to Post-PRWORA Social Policy towards Women Who ~Just Say No!~ to Abuse and Proceed in Misplaced Belief They can actually Exit it) [started Sept. 18, Publ. Oct. 9, 2017, see also Collaborative Justice post/page].

I might as well get this over with, and am taking the opportunity at the same time to say I finally published a related PAGE, How and When Problem-Solving (make that ‘Collaborative Justice’) Courts were Institutionalized and other Consolidate/Coordinate/Standardize/ PRIVATIZE Stories at Courts.CA.Gov (Page started 8/29/2017, published Mon 9/18 evening. With case-sensitive shortlink ending “-7w9″).

Together, that page, another post introducing that page (full title soon, just below) and this post About Holidays, Speaking Personally (Personal Backdrop to Post-PRWORA Social Policy towards Women Who ~Just Say No!~ to Abuse and Proceed in Misplaced Belief They can actually Exit it) [started Sept. 18, Publ. Oct. 9, 2017, see also Collaborative Justice post/page](case-sensitive shortlink ends “-7AD“) are “good stuff” and history on some major program-propagation vehicles in New York and in California, with more in their middles on Minnesota-related events, people, and even a few nonprofits.

What’s here below was originally an insert or aside. At the bottom here, I again provide the link to both the page and my post introducing the page. I hope readers will go back and read both if they haven’t yet.

There are reasons we are continuing to have “family court fiascoes” and destructions of household wealth generation after generation by way of prolonged litigation IN these courts.

Why not take a closer look at how they were assembled, systematically, in recent decades (generation or so) and the pieces from which the parts comprise the whole, or the engine, chassis, fuel, guidance system, [I’m no auto mechanic, but consider the essential parts — and the roads as part of the infrastructure too] and ensuring a constant stream of passengers, with “no stone left unturned” and no child, or life, left unscathed….?] That’s what I tend to do, when not speaking personally..take closer looks. Lots of them.

“ABOUT HOLIDAYS, SPEAKING PERSONALLY:”

About Holidays, Speaking Personally (Personal Backdrop to Post-PRWORA Social Policy towards Women who Say No! to Abuse and Proceed to Exit it) (WordPress-generated, case-sensitive shortlink ends “-7AD.”)

This post, while written (except this foreword) around Sept. 4, Labor Day Weekend 2017, was taken from another post then still waiting publication; its full title (and basic background-color) is “Introducing A New Page, How and When Problem-Solving (make that ‘Collaborative Justice’) Courts were Institutionalized and other Consolidate/Coordinate/Standardize/PRIVATIZE Stories at Courts.CA.Gov. AND Some of the Backdrop (Personal Experience of Turn-of-Century Social Policy towards Women Reporting Abuse and Their Efforts to Exit It… ).”(case-sensitive short-link ends “-7xs“)

Exactly one week later, in fact another historic (but not “holy”!) day in recent history, I was still working on both post and page, as I was over Labor Day weekend, a major US holiday from September 2, 3, and (Monday) Sept. 4, 2017,* through to that day, Sept. 11, 2017…

{*The aside added for international visitors to the blog. I don’t know all their national holidays, and they might not know all ours, either. While this blog covers some international issues because it covers private associations dealing with US courts — many of which make sure to advertise that they have an international membership— FamilyCourtMatters still primarily addressed to people dealing with Life In The USA… because the courts here are tax-supported and public institutions in every state, and in territories, of the USA. We pay plenty for them, while we also through our system here (as to the income tax, corporate taxes, and tax-exemptions) sponsor, incubate, and overall, encourage the formation of tax-exempt corporations to fix whatever national, state, or local governments omit, forgot, or “got wrong..”}

BELOW HERE (within this blue box) is “Soap Box” talk on public vs. private. If you “get this,” skip it this time. If you don’t, please consider the stakes are high in blurring one with another, which is a known practice and agenda now commonplace in the country (and not USA only).

These tax-exempt and other corporations can legally register as domiciled in one place, but operate and influence operations across state and national lines. But the family courts regulating life within the states are subject to state legislatures for individuals once they obtain jurisdiction over a case — and through that, the family members involved — do not have innate jurisdiction over people outside the state except as related to something anchored in it. There’s a division, in other words, between jurisdictions within states, and federal. What I’m saying here – it seems to take corporations to overcome legal boundaries to representative government at the state level — and that seems to be the intent and purpose of a variety of such corporations who would rather “legislate” or at least influence, rule, and have power, over whole regions, or nations, at a time, and the streamlined ability to also influence legislation in multiple jurisdictions without having to fight it locally, place by place — and deal “face to face” with those who might, were they aware of the purposes — have cause to oppose them. (See “Big Seven Associations” and/or the variety of “Do You Know Your NGA, NCSC” etc. posts I’ve written within the last year, or maybe two.. for how this seems to work when those on the private corporations ALSO hold public office, either concurrently, or in revolving-door fashion, recently…

{{As I understand it, there ARE no “regional governments” under the US Constitution, that I’m aware of. Some people have a problem with that (search “functionalism” on this blog for more info), and want it changed. The more and more functions that can be “outsourced” to regionally organized private-sector organizations (or JPA’s — Joint Powers Authorities) — the less and less individually responsive less-than-regional governments become. They feel the pressure and appreciate the prestige of “belonging” as evidence of good governmental behavior.

Sure, federal government’s Executive Branch Departments (like HHS, which was formerly — taken together with the part that split off, the Dept. of Education and any other — “HEW”) organize operationally by regions (cross-state lines), as do Districts of the Federal Court system yes — but even those are not independent government entities.

To organize legally cross-jurisdiction WITHIN government here, one must either be anchored in some part which IS either federal OR state, i.e. be state government or something underneath it– or simply be a corporation, including tax-exempt ones. Joint Power Authorities such as I’ve been blogging, like WestED, SWRL, or FWL (Far West Labs, South West Regional Labs — subject matter, education) still must anchor with a state domicile. WestED’s state domicile, so far as I know, is in California, although other states are spanned in its OPERATIONS (shared programming).}}

That’s why, at a time when “Public/Private Partnerships” (or, strategic operating relationships in the forms of Memos of Understanding — one shown below here as to CENIC and California’s HighSpeedRail Authority) are MOST popular with those already in power — we really should be able to tell the difference between that which is public — and its LEGAL power over individuals, including the power to tax, incarcerate, seize assets, seize children, etc. — and that which is NOT public, over which when we are not consumers of the product or entering into conscious contracts with the corporations, we don’t have many real rights. So government uses corporate to cross jurisdictions, and to (as privatized) avoid full responsibility for its actions, and streamline (efficiency) and corporate uses government to encourage conditions it finds conducive to operations and bottom-line profits. This may or may not include the public interest or health; it depends on the situation. [[end of “SoapBox” commentary.]]

Personal timing & publication dates:

The weeks between Sept. 11 and now (early October, 2017), I was working again on some personal writing for an ongoing situation, which was because of its nature and, shall I say, “tenacity,” triggering PTSD and some deep, deep considerations about how far I should or dare take the push for justice in that situation and with these particular individuals who have gained a legal inroad into my life recently, caused damages, and then inflicted further distress through minimizing/dismissing the same. Classic gaslighting and strategy for controlling personalities and/or abusers.

In “About Holidays,” I also speak about some of the long-term tenacity of the prior personal situations, without naming names — because the names aren’t the point. The patterns are. I realize this type of communication is anecdotal, and speaking about it here is for general info.; expressive, not presented as a basis for policy.

When that communication (or at least the initial stage of it) Sept.11 / end of Sept. was handled (or, at least, delivered) I worked again diligently to update this post’s Table of Contents page, a project I am finally, for the most part, satisfied with (for now) and which led to more fascinating subject matter to research, involving consolidation of telecommunications (broad-band-providing) companies servicing government entities (like schools, public and private universities and research institutes), and such.**

**[Corporation for Education Network Initiatives in California, “CENIC.org”; its network “CalREN,” and as it’s a membership association, one of its Auxiliary Associate members (in fact the only one currently) “City of Hope” (hospital, institute, development corporation, foundation all inter-related) and dark-fiber network subcontractor, “Level 3 Communications” with its own fascinating history, intersecting with some of the giant telecommunications providers (esp. broadband) mergers of the turn of the century — and its predecessor entity “Kiewit Diversified Group,” which came out of Peter Kiewit & Sons (or similar name), the construction industry. This is basic communications history in the US, and fascinating. It also speaks to the access to high-quality internet capacity and speed of higher education institutions (membership to CENIC or groups like it) vs. the average person, who is the subject matter of so many of the programs, including the social science R&D, federal designer family, poverty research, behavioral mod etc. — while when working as employees, contributing to support the same infrastructure financially based on the trickle-down premise.

Californians are aware of longstanding plans, highly political in nature, for a high-speed physical, commuter (to carry human beings!) rail system connecting Northern Cal. to SoCal (take another look at the map of the USA and see — that’s a good distance!).

So, it looks like CalREN’s (CENIC’s network name) involvement with this high-speed rail project may result in communities along the intended route getting an upgrade to their free? Broadband service. Amazingly, the researchers figured out that poorer, less-educated people living in rural areas are less likely to have internet connections –aren’t they smart? Courtesy “California Emerging Technologies Fund” field research poll, I see.

CENIC article referencing Calif. HighSpeed Rail Authority (a gov’t entity) plans to make broadband communities. CENIC is private nonprofit, so that’s another Public/private partnership, assuming it goes through.

Announced at “Cenic.org” · PRIVATE UNIVERSITIES & NPS, RENS & NRENS

In general, the HSR will connect Los Angeles to San Francisco at 200mph or in about 3 hours by (2025? see info). Another phrase that comes up is “Silicon Valley to Central Valley” with Central Valley being an area where unemployment (and poverty) are high. I see from HSR website that ARRA funds were involved:

SACRAMENTO, Calif. –The California High-Speed Rail Authority today announced it has met federal American Recovery and Reinvestment Act (ARRA) of 2009 requirements by fully investing the more than $2.55 billion granted to the State since 2009 to build the nation’s first high-speed rail system. These funds have helped to create thousands of new jobs and generated approximately $4 billion in economic activity in the Central Valley and across California. Read our News Release to see what Board Chair Dan Richard is saying about meeting the ARRA deadline. For more information, read the full Investing in California’s Future through the American Recovery and Reinvestment Act of 2009 report.

Wow. I remember where I was in high-employment area SF Bay Area in 2009, after child-stealing events, retroactive reduction of child support arrears owed, dramatic curtailment of my own work as I went repeatedly to court in an attempt to resolve the household who stole the kids’ reluctance to comply with court orders granting me: visitation, or even at its lowest point, weekly phone calls placed by the children (after my attempts to reach them weekly went unanswered time after time), and by 2009 I had not one job in the profession left. No one in the agencies or law enforcement seemed to care about enforcing any court orders which would mitigate the situation, and I was running out of the wherewithal to keep coming back to court (let alone even get TO the courthouse) time and again. During that time I had not yet “figured out” what I have since (on this blog) regarding potential financial DISincentives for continuing any government OR nonprofit advocacy group, i.e., the whole systems, to protecting maternal parenting time once it’d been eradicated without legal cause stated on the record, let alone proved on any record…

In other words, those “access and visitation” grants aimed at increasing non-custodial parenting time, apparently lost their motivational impact when that non-custodial FATHER time had been increased to 100% and mother’s to “0%.” I had never been offered or encouraged to do supervised visitation to prevent the stealing in the first place, and when it was brought up, a commissioner said “there’s no money for it here..” — AFTER which I realized, well, yes there was, in the form of those grants to the state of California for such supervised visitation and exchange — to protect the children from being stolen, and myself from injury or repeated forced dealings with traumatic situations absent support for them, in the context of known prior domestic violence…

That fall 2009, I also had learned my children had been abandoned by their father (physically and it appears financially) and was dealing with both stalking while attempting to extract information from ANYONE involved on WHEN this occurred (including what month/year) or in what manner (two conflicting versions were presented by the ex-girlfriend and my ex-batterer (husband) and father of two children by then both almost adults, with me. Abandonment is also a felony, so I was working through both shock and again attempting to speak with law enforcement on this (district attorney’s office, as I had when they were stolen the first time three years earlier). This went nowhere — other than that in my need to speak to their father for this information, he somehow decided again to claim me “before God” as his wife, resulting in the need to at this low point now deal (again) with the stalking issue — which was terrifying… especially without funds to leave the area even temporarily which was a need.

But that commentary is getting ahead of the subject matter of this section…. Just correlating the State-level developments with my personal timeline developments. Back to “HighSpeedRail”….

Read it from the HSR.CA.GOV (HSR=”High Speed Rail”) point of view — this is their MOU (Memo of Understanding) which, actually, clarifies that one is a 501©3 and the other a state agency, and that a partnership, this absolutely does not make!. The signatures of each party are shown — but not dated (so this is probably not an executed copy of any MOU, despite its title page):

MOU as shown (Nov. 2016) header.

REGARDING OTHER CENIC or “NATIONAL LAMBDARAIL, LLC” referring to a different kind of “rail” with different kind of cargo (the optic fiber kind) images I may include below — these are obviously another story waiting to be posted (here — it’s already posted elsewhere!), consider these footprints and reminders for now.//LGH 10/9/2017

This excerpt of a Form 990 shows Nat’l LambdaRail as a related entity of CENIC, though not the largest one… || … “NLR” has a major, and dramatic though short history, and was purchased in 2011 by a billionaire from its university (public/private) membership. Won’t fit in a single caption. Stay tuned (or look up yourself!)It is a 12,000 mile optic network and the first one to go transcontinental (See Wiki or Bloomberg.com for more; also IO.com)

just web page header.

CENIC corporation, California Registry of Charitable Trust (search results page)

These sprang from an unusually-named corporate (nonprofit) visitor to the blog, but in general reflect major themes and turning points in U.S. history, i.e., control of access to the internet, and characteristics of the organizations controlling this access. For the general outline, see my 2017 Table of Contents page, about half-way down, and the bottom section, and the second section of my Oct. 9, 2017 post talking about SIZE STILL MATTERS. …..

WOW: See that image on National LambdaRail, LLC, above? Well: from Wikipedia:

…National LambdaRail was founded in 2003 and in 2004 its national, advanced fiber optic network was completed. In addition to being the first transcontinental, production 10 Gigabit Ethernet network, National LambdaRail was also the first intelligently managed, nationwide peering and transit program focused on research applications.

In 2008, a company named Darkstrand purchased capacity on NLR for commercial use.[1] By the end of the year the Chicago-based company was having trouble raising funding due to the Great Recession.[2] On May 24, 2012 the NLR network operations center services were transferred to the Corporation for Education Network Initiatives in California.[3] In October 2009 Glenn Ricart was named president and CEO.[4] On September 7, 2010 Ricart announced his resignation.[5]

In November 2011 the control of NLR was purchased from its university membership by a billionaire Patrick Soon-Shiong for $100M, who indicated his intention to upgrade NLR infrastructure and repurpose portions of it to support an ambitious healthcare project through NantHealth.[6] The upgrade never took place. NLR ceased operations in March 2014.[7][8][9][10]

Bloomberg.com on National Lambda Rail. Bloomberg.com gets its data from S&P Global Marketing, part of S&P Global Group (S&P = Standard & Poors, probably)

http://internet2.edu/news/detail/3695. Not shown — this is a 2003 article. See Wiki for follow up info on NLR.

Please click link (or image to enlarge) and read: https://en.wikipedia.org/wiki/National_LambdaRail#cite_note-5

At Bloomberg.com, but can’t read more w/o subscription to “Professional Services.”See more at NLR “Wiki” page.

Internet2® started in 1996 and has a timeline. See website for more info.

Internet2® doesn’t post its financials With offices in these states, perhaps they could be found. If “internet2” isn’t an entity, then some membership organization ENTITY does have financials somewhere…

Found at Internet2.edu home page, blog article Sept. 17, 2017.

Separately, which I know from email news alerts and family court reform advocacy groups’ social media sites, there are also pending “current events” in local (California) “family court reform” news making the rounds which I feel urgent to address in new posts. I have an idea of a better way to present the situation to people new to it (those familiar with it are welcome to watch from the sidelines, or inbetween rallies, re-blogging, or complaints about the overall injustices in the system, judge by judge or jurisdiction by jurisdiction, something I can’t remember the last time I EVER signed onto that approach as halfway sane, or effective, given the disparate resources….). Some of that way is blended into this otherwise more anecdotal, expressive post about the personal backdrop to our so-called problem-solving courts.

I keep hoping to squeeze enough blogging and activism in between my own ongoing, though more periodic, life events which have been incited by the systematic disruption of my household, work and relationships through the family court and now, probate court, systems and self-important, self-congratulating, and overlapping circles of well-endowed and court-AND social-service-systems-connected “fauna and flora.”

That is, just as in any domestically violent relationship, while there may be at times a “plateau” between incidents (events), during which not a whole lot can be done to push them forward (whether through availability, regulations, or simply personal stamina), and then, responding to moves the individual (here, me) might make to change the status quo or resolve the conflict — there’s an escalation, or other way in which “power-over” is communicated. This communication may be first made in private, but sooner or later can be gestured towards (by the abuser) should it go public, “we attempted to communicate with [____].” Communicate in that context is a euphemism. Something WAS communicated — message of intent to continue the dynamic was sent-and-received — but it’s not what witnesses or outsiders are, for lack of tangible substance, or facts in context, unable to do anything other than assume might be meant were both parties above-board and honest. [I don’t know how that last sentence in green may read to others, but I do know what I meant. There are just multiple layers of meaning, and a style of speaking — which I hate! in trying to actually get down to the facts and resolve the situations — which is more theatre than written communication of important truths. It’s for show, but only those closest to the situation and “in the know” about the overall pattern of the relationship in question, realize how fake it is.

So, again, stamina, or consequences, etc. I don’t know how much longer this can be kept up, either the personal fight, or the writing. It worries me, and may be prompting to get what’s done already in order, backed up, and on-line. And it’s no way to live… with constant risk management while resources are drained, year after year.

Moving on….

Blogging Context/Sequence:

“Introducing A New Page… Problem-Solving (‘Collaborative Justice’) Courts…,” (for short) has a case-sensitive short-link ending “-7xs” and is now published.

See next inset block:

[That] page (#28901) I have named: How and When Problem-Solving (make that ‘Collaborative Justice’) Courts were Institutionalized and other Consolidate/Coordinate/Standardize/ PRIVATIZE Stories at Courts.CA.Gov

I was talking on [the] post — NAATPN, Inc (2000ff, Total Current Assets, $0) and Caffee, Caffee and Associates PHF, Inc. (Hattiesburg MS, 2003ff, Total Assets $0, Tax Filings Questionable), and others trying to squeeze a California Race-Based Stop-Smoking Network (AATEN) into that recipe. .. [Published 8/28/2017 evening and as usual may be updated for clarity, basic copyediting, or length (splitting)//LGH] —— about how the 1996ff (PRWORA-related) events overlapped with my current blogging interest, the 1998 (Tobacco Master Settlement Agreement) events, and similarities (not to mention overlap) of involved networking nonprofits, along with the stories told the public omitting the details of Who’s Who and the gradual, (dare I say “progressive” in today’s political climate, but referencing the generic, not political, meaning of the word?) incremental erosion of local or even state-level accountability to citizens living within those state, as opposed to privatized special-interest nonprofits continually telling us all that the same are protecting against other privatized special-interest FOR profits as though these two were unrelated….

Again, the genealogy (so to speak) of that page, includes ITS originating post, on the NAATPN. So, the sequence is from NAAPTN {already published} ==> Page “How and When Problem-Solving..” ==>Post “Introducing New Page” + ===> before I publish either that Page (or the post introducing it), I sequestered my expressive/reflective section “About Holidays” which you are now reading.

The originating post (“Introducing a New Page…”) will contain some lead-in and concluding material from below for a “footprint,” as is my writing style.

Impediments / Other reasons for the delays:

SHARE THIS POST on...

Even More Considerations on NASMHPD (and DBSA, and NAMI), and MHA. See Also Recent Epidemic? of Attorneys-General Suing Big Pharma over the Opioid Abuse Epidemic. [Publ. July 6, 2017]

The theme, continued, is still …”DO YOU KNOW YOUR NGA, NCSC, NCSL, NCSEA, NCJFCJ, NCCD, NACC, NASMHPD, not to mention ICMA?”

Even More Considerations on NASMHPD (and DBSA, and NAMI), and MHA. See Also Recent Epidemic? of Attorneys-General Suing Big Pharma over the Opioid Abuse Epidemic. [Publ. July 6, 2017] (post short-link ends “-79i”)

This post being published July 6, 2017 evening is about 8,000 words (shorter, for a change!). It comes in two basic sections — ICMA-related, and The Four Organizations-related (NASMHPD, DBSA, NAMI, and MHA). I might later add more images showing the networked DBSA entities, but as written, I feel it’s written clearly enough (especially with the visuals) to be published now.

“DBSA” stands for Depression and BiPolar Support Alliance, formed in 1985 in Illinois. “MHA” stands for Mental Health Association.

An aside, for this post, who is ICMA?

It takes a few paragraphs and several images, but I’ve used the reference in post titles and themes often enough I felt it time to identify the acronym “ICMA” here again.

While I’m including information from its website, on a related entity and a partnering entity before getting into the main subject matter, remember that this ICMA section and information near the top of this post is included now only for a point of reference in the landscape of membership organizations involving public employees, and for awareness of its existence, and some of its scope — not as main post content. As I showed before, along with the NGA and others, ICMA is considered part of the “Big Seven Associations” by those so-associated (!):

The “Big 7” is a coalition of seven national associations in Washington, D.C., whose members represent state and local governments. The leadership of these organizations works together regularly to discuss issues of mutual interest affecting state and local governments. Members of the “Big 7” include: The National Governors Association, the National Conference of State Legislatures, The Council of State Governments, the National Association of Counties, the National League of Cities, The U.S. Conference of Mayors and the International City/County Management Association.

There’s a wikipedia “stub” (doesn’t say much, except that they are influential in lobbying for their interests) on “the Big Seven,” and as you can see, the ICMA (the “C” standing for the two-word descriptor (adjective) “City/County” seems to show up in its logo):

The Big Seven is a group of nonpartisan, non-profit organizations made up of United States state and local government officials. The Big Seven are:

- Council of State Governments

- National Governors Association

- National Conference of State Legislatures

- National League of Cities

- U.S. Conference of Mayors

- National Association of Counties

- International City/County Management Association <==

These groups are influential in national government, often lobbying Congress to represent their members’ interests.

References[edit]

- Patterson, Bradley H., Jr. (2000). The White House Staff: Inside the West Wing and Beyond. Washington, D.C.: Brookings Institution Press. pp. Ch. 13. ISBN 0-8157-6951-2.

Bringing up the “power of the GASB” (a post I’m still working on talks about how), know that a tax-exempt foundation in Norwalk Connecticut, the “Financial Accounting Foundation” (FAF”) actually set up and controls both the GASB (Government Accounting Standards Board), some time after the FASB (Financial? Accounting Standards Board) for the private sector, in the early 1970s. They delegated powers to the respective boards, but still maintain ultimate (veto, etc.) power over them.

(This diagram also on FAF “About” page, shown nearby)

FAF outlines its identity and purposes (FASB and GASB)

Rules change from time to time, and rule-changes can make or break a city county, or possibly even state — and often around the issue of pension funding. So in 2012, “The Big Seven” responding to a rules-change drafted a policy response for how much people should contribute to their own pension plans (ARCs and Annual Designated Contributions):

“Big Seven” Focus on Pension Funding Policy October 01, 2012 (found at “leg.Wa.Gov”) WASHINGTON—The executive directors of the Big Seven state and local associations today released draft “Pension Funding Policy Guidelines” for state and local governments. [Same announcement on the same date provided through National League of Cities, this one with a link to the (2page) guidelines.**]

The Governmental Accounting Standards Board (GASB) recently issued new standards that focus entirely on how state and local governments should account for pension benefit costs. However, they did not address how employers should calculate the annual required contribution (ARC). To assist state and local government employers, the seven associations are engaged in an ongoing effort to develop policy guidelines. [[some points raised. Note: this doesn’t have an active link to that released draft, just advertised it on an NGA website, apparently.]]

“Government leaders have to make difficult budget decisions every year, said Robert J O’Neill, ICMA executive director. “Having a rational way to calculate their annual required contribution helps them stay on track to meet their retirement obligations.” [[Para. listing “The Big Seven” omitted]]

The National Association of State Auditors, Comptrollers and Treasurers; the Government Finance Officers Association; the National Association of State Retirement Administrators and the National Council on Teacher Retirement helped draft the guidelines.**

**Link to the Pension Guidelines (now almost five years old) shows why (see last para. in quote) those particular organizations helped draft — because the Big Seven asked them to! (next screenprint) as convened by a “Center for State and Local Government Excellence” which the guidelines don’t bother to mention is taking ICMA Retirement Corp funding and working with them:

Natl League of Cities Oct 1 2012 Link to 1209PensionGuidelines

(annotated excerpt from 10/1/2012 Big 7 Pension Guidelines (a 2pp release)

What’s ironic about this — the Big 7 Associations advising governments how to address pensions are themselves subject to FASB (not GASB) standards — because they are in the private sector. This information was a search result on “The Big Seven” but included because in the ICMA section below, an entire corporation managing public employee retirement plans for ICMA (it’s called ICMA Retirement Corporation) comes up. The convening organization is an LLC listed in ICMA-RC’s “Sched R -Pt I” (disregarded entities, at the same street address and floor like its other Sched R Pt. I Disregarded entities. It is controlled and apparently funded by ICMA RC to conduct research on municipal and local retirement plans, specifically. Website says it was created for this purpose in 2007.

Take a look at the FY2008 ICMA RC Salaries (totaling $13M for Part VIIA — includes not just Directors and Officers, but also Highest-Paid and Key Employees). In later years it’d be $19M !! I see the President at this point had a salary of four million dollars and at least three others, over $1M each….

It’s not the primary purpose of this post, which focuses more on the four entities in the title, all dealing with and named after topics surrounding “mental health,” and involved individually and at times with each other in the strategic push for a paradigm-shift, intended to make and keep, nationally and by communities, provision of mental health services a regular part of basic primary health care, and so covered by insurance for that primary health care. To do this, considerable marketing and social communications sector, and affiliate organizations are involved.

I’m including the short(er) section on ICMA up front because I think it’s time to do so. There’s also a certain element of comic relief — well, at least of comedy. You’ll see….

(These might be separate entities also; however I saw that the California group merged into the main one).

After looking more closely I see what ICMA’s acknowledged partner “Alliance for Innovation, Inc.” f/k/a The Innovation Groups” is doing, or at least how it’s been operating (since 1979, it says), although why ICMA would partner with such incompetence (speaking as to their tax returns), one wonders…. The Innovations Groups is plural because it has regional offices and at least one merger (for the region “California-Colorado-Nevada-Arizona”) in its 40-year-plus history. (See two images from their “founding documents” — link part of the California OAG link provided below). “The Innovation Groups, Inc.” is the prior name (one of several) for what is now “Alliance for Innovation, Inc.”

Alliance for Innovation, Inc. also registered in California (now as a Florida Organization with an Arizona Entity address) since 1991, but quit filing with the Office of Attorney General Registry of Charitable Trusts (“OAG RCT”) its required annual tax returns and RRFs — with the annual fees based on revenues — (as a 501©3) since 2006, was not marked “Delinquent” until August 2010, despite its last known annual revenues being over $1M, and remains active as a corporation. In other words, it wasn’t “FTB Suspended” by the Secretary of State, nor is there even any uploaded information that the California OAG even ASKED it for the about eight years of missing tax returns AND RRFs, or threatened suspension if they didn’t cough them up — which it does for other entities. I wonder why not…and am tempted to compile enough related facts to write a letter (anyone reading this, also feel free to, or call to find out if there is some legitimate reason).

If you’re curious about that aspect, look here (about 2pp): AllianceForInnovatn (does bus w ICMA) Calif OAG Chart Details EIN# 591936650 No Filings Since FY2006 not marked Delinq til Aug2010 – WHY? I didn’t address the OAG delinquency in the section on ICMA (tan background color) below; there’s plenty of other things to report. Note: The many links on the above pdf to uploaded filings that were made (towards the bottom of its about 2pp) should still be active; they won’t fade with time unless the OAG moves the documents.

ICMA INFORMATION:

“ICMA is the professional and educational organization representing appointed managers and administrators in local governments throughout the world. It sponsors, develops and implements a number of programs that provide local government managers and administrators with expertise on a variety of topic areas.”

| ORGANIZATION NAME | ST | YR | FORM | PP | TOTAL ASSETS | EIN |

|---|---|---|---|---|---|---|

| International City/County Management Association | DC | 2015 | 990 | 65 | $15,057,789.00 | 36-2167755 |

| International City/County Management Association | DC | 2014 | 990 | 63 | $15,570,124.00 | 36-2167755 |

| International City/County Management Association | DC | 2013 | 990 | 58 | $16,443,151.00 | 36-2167755 |

Since 1914 (odd timing, 1 year after the income tax was established through US Constitutional Amendment). Tax returns show it’s an IL corporation with a D.C. address and two related (Sched R) entities, one I reference below, and the other is an REIT holding their D.C. Headquarters. They receive income from both (see Sched R), and spent around $7M in overseas activities (Sched F) the last year shown above, FY2014 only. They took in $11M+ Contributions and $11M “Program Service Revenues” (including membership fees, a good chunk” and, per page 1, spent over $12M on salaries (158 employees) and over $12M in “Other Expenses” resulting (when combined with $349K grants to others) in an about $250K Deficit. The year before they had radically higher contributions ($18M) but still overspent the budget. The related “ICMA Retirement Corporation” while I’m here, has its separate tax returns. WOW.. An entirely different picture. Also, this one is FY1972 (it says, started with help from a Ford Foundation grant) and a Delaware Corporation — same street address except the Suite#. The difference in size is predictable because after all, it’s handling retirement plan benefits:

Total results: 3. Search Again.

| ORGANIZATION NAME | ST | YR | FORM | PP | TOTAL ASSETS | EIN |

|---|---|---|---|---|---|---|

| INTERNATIONAL CITY MANAGEMENT ASSOCIATION RETIREMANT CORPORATION | DC | 2015 | 990 | 53 | $489,002,619.00 | 23-7268394 |

| INTERNATIONAL CITY MANAGEMENT ASSOCIATION RETIREMENT CORPORATION | DC | 2014 | 990 | 54 | $493,889,563.00 | 23-7268394 |

| INTERNATIONAL CITY MANAGEMENT ASSOCIATION RETIREMENT CORPORATION | DC | 2013 | 990 | 51 | $452,312,085.00 | 23-7268394 |

SHARE THIS POST on...

Yes, Broken Courts, Flawed Practices, and the Parade of Fools: (Pt.1(a) Intro, Context) [Last post of 2014, publ. June 29, 2014].

From this post as first published:

This post is about advocacy group supporters and followers failing to set standards and keep their own leaders ethical. In a larger sense, the same goes for all of us as citizens, supporting by personal energy and labor (i.e., government revenues) — how can we keep leaders honest or ethical if we don’t have a grasp of what they are doing, what they are paid to do, and how the system is organized? ….

It is a natural continuation of the recent (and from May 2012) “Parades, Charades and Facades,” and my posting this is keeping a personal promise (to myself) for the year 2014, to expose what’s underneath the rhetoric.

I had no way of knowing at the time, but this became my last post of 2014, and I didn’t post anything for the entirety of 2015, for another round in the court system and while handling (yet) another round of family-generated problems putting my housing at risk through previous rounds which destroyed a sustainable profession (through the family courts) which was then used, apparently behind my back, to take control of an inheritance, and all but “dare” me to challenge the current status quo.I tend to challenge any current status quo which forces competent individuals onto food stamps needlessly, and continues to harass and interfere, cyclically, as I am noticed to be engaging in obtaining replacement work. This was coming to a head in summer 2014, which also may have prompted my desire here to lay out the elements clearly, naming names, as to which organizations occupied what status on the family court reform (and associated “domestic violence prevention” food chains, and how I came to understand where they were on that food chain.

In late 2019 I am coming back to review this post along with a few others which engaged in the “Our Broken Family Courts Initiative” (i.e., the Cummings Foundations, legal domicile Nevada, field of operations it seems, they’d chosen for some reason nearby Arizona.

I noticed it lacked my usual “Title & Shortlink” format, so came here to add one, to add the date published to the title itself, and these comments. It’s clear I considered this even in 2014 an important point to make by the next update section.//LGH Dec. 7, 2019. Here’s that Title now:

(short-link ends “-2ug”). Having also now noticed this post is an obnoxious 25.4K words long, I’ll see if/when I might get to an abbreviation and/or re-posting of key parts. That’s not a promise, just a recognition of the need! NOTE: This post has comments (some dialogue with readers) and more helpful links. Most posts don’t have comments; these are worth reading (and found at the bottom) as are I still believe its extensive list of tags.

//LGH.

[Published June 29, 2014; Post in edit mode late July-Aug. 2014; expanded to almost double the size,nearly 24,000 words; with background info….In most posts, a lot of the length is simply quotes, my style is not just tell, but “show and tell.”]

February 2016 Personal Update:

Without changing the contents here (except one paragraph or so, cleaning up some formatting and adding tags), I’ll mention that the MAJOR break in posting anything between June 29, 2014 and early 2016 came because my personal situation heated up so much after I went public on fiduciary abuse by an older sister — who’d played a crucial role in supporting/enabling (if not inciting) our original “custody war,” after playing a negligible, passive, codependent, domestic-violence-enabling role the previous decade, after learning that I was a battered wife and mother and seeking intervention.

From summer 2014 – early 2015, the situation went into probate court — lasting in total, nearly a year, to finish transition. Throughout 2015 I was working with and renegotiating standards with personnel in control of my resources, and continuing to withhold access to evidence of the paper trail….From summer 2014 – 2016, I was still writing things up, investigating, communicating privately with some individuals — but also had to spend major time, that’s writing time, and to lawyer, sister, starting with unearthing a written commitment on her part, yes/no — are you resigning or not? Then, requesting to settle out of court (which is possible under California code and the individual trust), which (of course) was rejected, stringing the process out, adding more professionals (not that I had some for protection on this end).

In 2015, a major transition dealing with new people — major negotiation time, and now as the year 2015 closed out and so far in 2016– I find myself again fighting for housing, and to obtain financial records, which certain people don’t want found. Both my (so to speak — father no longer involved, and I was prevented from continued involvement years earlier) young adult children now being out of the state, I had hoped to move on with life, and promptly move out of present housing. I found — “not so” from certain personnel, and that “not so” is in one of the most effective forms of messing with other human beings — litigation absent the supporting facts (and here, even proof of standing) as a form of extortion, which like some of the other things this blog talks about (child-stealing, wife-beating, stalking, terroristic threats on individuals, statements under penalty of perjury which are, well, known to be falsehoods by those speaking, these are criminal issues.

In these conditions, struggling with wordpress HTML and getting out a post, wasn’t going to happen. I’ve been working at a different format to start uploading what did, still, continue learning during the non-posting time. We shall see…. Anyhow, that’s why no follow-up parts to this post occurred, much as I would’ve liked to complete them. There are plenty in draft, and I am posting again. There are still plenty of survival-level challenges, which means that about the only relief or “down-time” still involves this kind of blogging anyhow —

––and in continuing to blog I am still thinking about the next generation, particularly of those who may have been trafficked, traded and repeatedly disrupted (UNLESS they come into an abusive home, it seems — then the “don’t disrupt” theme seems to prevail) like commodities between and among parent/non-parent caretakers — all rationalized and presided over in the institutions run by privately-networked in organizations & with those in government positions people (judges, experts, and social science research & demo projects building their resumes and journaling their findings) “IN THE PUBLIC INTEREST” and in the name of “NON-ADVERSARIAL COURT PROCEEDINGS,” “REDUCING CONFLICT” and of course Treating and Healing the scourges of wife-battering and child abuse [“SUPERVISED VISITATION / BATTERERS INTERVENTION”], for “Futures without Violence” “Safe Horizons” “Justice” (a common label on oh so many organizations), FAMILY reunification, preservation, (…. Responsible Fatherhood, Healthy Marriages, Access and Visitation — all such good, wonderful, noble things…) and my favorite term when applied to what allegedly MUST happen between perps and those perpetrated-upon: “CONCILIATION.” Unless parental alienation was perpetrated upon someone in a high-conflict relationship, in which case cold-turkey quarantining of the offender with de-programming for the alienated minor children.

Maybe we should call these courts something more appropriate to what takes place in them — like virtual auction blocks, or stock markets in human lives, with some able to profit so well in the field, they can as majority shareholders, demand changes in management, streamlined efficiency and increased return to shareholders, futures, options, the whole deal, on the profits of churning individual human beings’ relationships under the banner of helping society — and of course anyone “low-income” adjust to business as usual.