HealRWorld CEO Michele Bongiovanni stated, “HRW is proud to partner with NJII in the new global accelerator and offer a three pronged value proposition: access to sustainability innovation for the corporations, for small innovative companies real world challenges, coaching and funding, and curated deal flow to investors.”

Interlocking, Dysfunctional Definitions, Cont’d: “NJII, a NJIT Company,” and (how, exactly, NJ became) “the State of Innovation.” [“Incorporated” March 17, 2019]

Interlocking, Dysfunctional Definitions, Cont’d: “NJII, a NJIT Company,” and (how, exactly, NJ became) “the State of Innovation.” [“Incorporated” March 17, 2019] Published March 20; 8,600 words, including some repetition. Shortlink ends “-9wS

This post is not a business entity or doing commerce, so technically speaking it’s not “incorporated” in any state for doing commerce (tax-exempt or not) within the state. However, if you consider my “body of work” in this blog, and that I just injected another post into it, with its separate page and personality (so to speak), in the generic, broader sense, I did “incorporate” it. (Corpus, habeas corpus, corporation, corpse, “corps,” corporal, corporeal, corpuscle: common roots):

This post was inspired first, by a recent Bloomberg.com co-sponsored Tweet, leading to a sponsored article, When Innovation is a State’s Main Industry, March 5, 2019: that’s where I started looking.

MAY 14, 2018, New Jersey Innovation Institute (“NJII”) and HealRWorld® Form Sustainability Accelerator”

Second, and within just a few days, having read the article and begun looking at websites, I also picked up on one of its projects launched under “HealRWorld,” announced in May, 2018 (This link drops many involved names See nearby link with NJII logo, “New Jersey Innovation Institute and HealRWorld® Form Sustainability Accelerator”).”

Among those names dropped is an easily searched name (because it belongs to a Greek Orthodox priest; the Greek connection had already surfaced via maternal family line of HealRWorld CEO/Founder (Michele Vonetes Bongiovanni).

May 14, 2018, NJIT announces the launch.

Sept., 2018, Institutional Investor article, “Priest, Hedge Fund Manager Charged with Fraudulent Short-Selling (of “Ligand Pharmaceuticals” based in San Diego, CA). The SEC charged, said priest vows to challenge and said it’s retaliatory for whistleblowing on accounting fraud at Ligand. RECENT news as you can see. Related, under SEC, reads (also Sept., 2018), “SEC Charges Hedge Fund Advisor with Short-and-Distort Scheme”

{He charges SEC fell down on its duties. Went looking, 3/21/2019; this is from Lemelson’s Amvona blog; posts a letter to the SEC cc’d to various authorities, warnings in 2016, etc. (TheLanternFoundation (<=FY2014) is a 990PF with small amount of investments in the Amvona Fund, EIN# 461737666 in Massachusetts}}

http://njii.com/sdgaccelerate/. Oct. 1, 2018, shortly after “Priest, Hedge Fund Manager Charged with fraudulent Short-Selling Scheme (Charged by the SEC). Click link and read agenda to see that only 5-15 minutes time was allotted to the many, well-connected individuals. Entire event only 3hrs long.

Also referenced (a different presentation, similar theme) at NJII.com/SDGaccelerate/, featuring a video message from NJ Governor Murphy, here, mentioning yet another involved nonprofit and more clues, though no direct links, to Who’s Who). (See nearby image, “The Global GOALS”).

RE: NJII + HealRWorld + the UN Summit on SME’s to further the UN’s 17 SDG’s

That image & link, (“New Jersey Innovation Institute and HealRWorld® Form Sustainability Accelerator“) was the first NJII project beyond the usual and overall Public/Private Incubator Accelerator situation which caught my attention as having too many unanswered questions about who was (ownership) and what is/are (type of business entity and/or product) was this “SME”and why was it chosen.

The situation and concurrence of people and organizations with disturbing lack of transparency even without the SEC report above had set off several of my observational alarms, from the start.

ALSO involved is the ICSB (International Council for Small Businesses) whose editorial offices are housed at and whose current Executive Director is at George Washington University (MBA and PhD) but originally from Egypt: Dr. Aymen El Tarabishy. He is popular, by having been voted “Outstanding Faculty Member” by the students, every year from 2010-2015, and:

Dr. Tarabishy is the only faculty member in the GW School of Business that teaches in two nationally-ranked programs. He developed the first Social Entrepreneurship and Innovation and Creativity courses offered to MBA and undergraduate students throughout the GW School of Business.

Dr. El Tarabishy is the originator of the United Nations International Day for Micro, Small and Medium Enterprises (MSMEs Day) that will always be celebrated on June 27th. MSMEs Day recognizes the important of entrepreneurs and small businesses worldwide.

MSMEs: Micro-, Small, Medium Enterprises.

(Link to that April 11, 2017 UN resolution”A/RES/71/279 reaffirming prior resolutions also, as to 2030 Agenda:

…Reaffirming also its resolution 69/313 of 27 July 2015 on the Addis Ababa Action Agenda of the Third International Conference on Financing for Development, which is an integral part of the 2030 Agenda for Sustainable Development, supports and complements it, helps to contextualize its means of implementation targets with concrete policies and actions, and reaffirms the strong political commitment to address the challenge of financing and creating an enabling environment at all levels for sustainable development in the spirit of global partnership and solidarity,

“sustainable development in the spirit of global partnership and solidarity”.. such a thrilling call to action, especially if one is in the business of providing finances or software platforms from which to unify the planet.

Compare with ICSB’s stated purpose (on its tax return):

TO PROVIDE EDUCATION, RESEARCH, PUBLICATIONS, CONFERENCES AND OTHER INSTRUCTIONAL & TRAINING FORUMS FOR ITS MEMBERS AND OTHERS AIMED AT IMPROVING THE MANAGEMENT SKILLS & UNDERSTANDING OF SMALL BUSINESS THROUGHOUT THE WORLD

and, under its third category of “Program Service Accomplishments” (shown below as an image and link to tax return also provided), you can see where the UN might come in. Incidentally, this doesn’t show that year’s accomplishments, as the IRS form directs. It talks about purpose:

SPECIAL PROJECTS ICSB, FOUNDED IN 1955, BRINGS TOGETHER MAJOR ORGANIZATIONS LIKE THE WORLD BANK, THE UNITED NATIONS, AND THE INTERNATIONAL MONETARY FUND (IMF) WITH PRIVATE SECTOR COMPANIES LIKE VISA INC ,SAMSUNG, DELL INC ,GALLUP INC ,CAPITAL ONE AND WITH UNIVERSITIES FROM AROUND THE WORLD (70 PLUS COUNTRIES) THIS KNOWLEDGE SHARING AND COMMUNITY BUILDING PLATFORM IS BASED ON THE SOLE PURPOSE OF PROMOTING ENTREPRENEURSHIP AND SME DEVELOPMENT WORLDWIDE THE NOTION OF DOING WELL IN BUSINESS IS ALSO TIED TO DOING GOOD FOR THE LOCAL COMMUNITY, NATION, AND THE WORLD TOPICS LIKE SOCIAL ENTREPRENEURSHIP, CORPORATE SOCIAL RESPONSIBILITY, AND CREATING SHARED VALUES ARE EXPLORED WITH AN EYE TO CREATING A POSITIVE IMPACT FOR THE FUTURE ICSB CURRENTLY WORKS WITH PRIVATE SECTOR ORGANIZATIONS LIKE VISA INC SMALL BUSINESS TO SUPPORT A GROWING NETWORK OF SMALL BUSINESS OWNERS WHO ARE COMMITTED TO MOVING THEIR BUSINESSES FORWARD BY GAINING NEW KNOWLEDGE ICSB HOSTED EVENTS, FOUND SPEAKERS, AND CONDUCTED RESEARCH FOR VISA INC

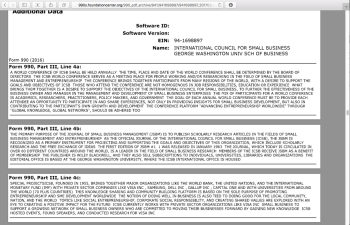

It was tough locating the ICSB’s actual EIN# (it’s not posted on their colorful website), however that EIN# is 941698897. On FY2016, the latest return shown at my usual provider — which I learned has recently merged? with or bought the trademark Guidestar® and/or its data and now is labeled “Candid“– there are internal financial inconsistencies which would affect the expenses and as a result, net assets balance, as well as missing paperwork (Schedule R, which should list George Washington University as a “related” organization but does not. It does aknowledge separately (Schedule O) that GWU pays ICSB Exec Director’s salary, which ICSB then reimburses). Link and some description in next paragraph.

{{March 21, 2019 — I kept looking. That’s only the beginning of the anomalies for this CALIFORNIA legal domicile entity calling itself (though not registered there as a corporation) a legal domicile District of Columbia entity, on tax return header pages…}}

(ICSB Tax Return FY2016, YE March, 2017 claims “0” employees, but about $167K salaries for them. The only paid officer, Dr. Tarabishy, received “$40,000” (even for 25 hours a week, with his qualifications, not much!) under “Received from Related Orgs” per Part VIIA, but then credited as from the entity (Part IX, Expenses). No page for Sched R (which would identify any “related entity” paying the only paid officer here) is uploaded. I haven’t checked other years yet). Lists “California” as another state it must file in.

-

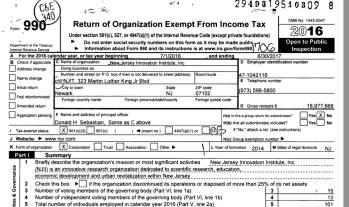

- ICSB FY2016, EIN#941698897, housed at GWU School of Business in D.C. ..Link to Entire Tax Return (from FoundationCenter’org)

The main assets are listed as “intangible.” If you’ll notice that Page 2 (Program Service Accomplishments) is artificially shortened (not a full 8X11 showing; it says “See additional data” but shows the numbers (Expenses, any grants, Revenues) for Lines 4 a, b, and c. Obviously by those numbers (whether Revs are greater or less than Expenses), Line 4a and 4c activities help support line 4b. Then go to “Schedule O” and read the description for Line 4c, “Special Projects” which ties in directly to the UN projects referenced above.

See 3rd image (explanation for “Program Service Accomplishments” labeled Special Projects, Line 4c; I also quoted it above in normal-sized print.

This membership organization’s name came up with another presentation featuring (Guess who: again, — HealRWorld®) which is why I looked it up. The images will not upload, but here are similar and searchable links:

- https://www.marketwatch.com/press-release/icsb-and-argentina-mission-co-host-first-ever-small-business-knowledge-summit-at-the-united-nations-2017-05-11

- (may be same article: Note: The current date always displays at top: Look for the article (press release) date, May 11, 2017):

ICSB and Argentina Mission Co-Host First-Ever Small Business Knowledge Summit at the United Nations

- Unify Earth Systems Ltd, which I was looking for (pre-publication) I see is a Bahamian-based technology company. Blockchain3.0 and “humanizing the blockchain.”

- (From an April 26, 2017 preview of the upcoming summit):

The MSME Summit will additionally lay the foundation for further discussions at the 62nd ICSB World Conference in Buenos Aires starting June 27, the First Annual UN MSME Day. The theme is, “Towards a New World Mobilized by Entrepreneurship & Innovative SMEs.” The world’s foremost experts and thought leaders in entrepreneurial research will come together to share their knowledge and expertise and discuss the latest trends.

etc. Bahamian business registry not searchable without a valid credit or debit card (Not going to provide, so I DNK whether it’s free to just look). Brief history of Bahamas with map shows history of enslavement dating back centuries, prosperity (because near shipping lanes) during American civil war, later American Prohibition (i.e., rum-running), final independence not until 1973, and it’s currently a member of the Commonwealth of Nations, i.e., recognizing Queen Elizabeth II as the head of state and the Governor-General as her representative. That’s where “Unify Earth Systems Ltd” seems to be registered, although its ownership because of the level of privacy here isn’t exactly known.

Basic (simple statements) at US Dept. of State regarding the Bahamas also points out that the main trade is tourism and financial services, as well as concerns due to its proximity to Florida. Diplomatic relations with the US were only established in 1973 when it became independent from the UK. Here is also the CIA’s “WorldFactbook” (probably one on every country). See “telephone, Telecom, internet, broadcast” sections. Also “Transnational” only mentions two items: one, a dispute about the maritime border; two, “transshipment point for cocaine and marijuana bound for US and Europe; offshore financial center”

Too many red flags there also, but I start below with the recent Bloomberg article. I have already Tweeted some of this (http://bit.ly/2ugpzSZ) (@LetUsGetHonest, Twitter thread, March19, 2019, three tweets and one reply with attached “media” (images), and some links to more information) , but do not expect a discussion to make this post. It should be a separate post. Feel free...to pay attention and cut through the PR to concrete, declarative statements about what is taking place among how many individuals with what collective vested interests.

Most relevant seemed to me how such a seemingly and (self-described as “SME”) small entity, only recently registered with the State of New Jersey DOR (2012, 2016) and in two different name formats, with the latter one NEVER being referenced in print, that I could see, in association with the brand, while the NJII itself only incorporated in 2014, could suddenly have major mentors (see “name-dropping” link above), connections to Dun & Bradstreet to the point of obtaining access to a giant data platform as is described, so quickly.

Who, really, owns whom (or owes whom) in THAT situation also speaks loudly.

Attention to wording and fine print, as well as what’s NOT shown where it ought to be by now, are clues. Conflicting self-representations (exact business type and entity) and absence of any besides one spokesperson (the “CEO/Founder” it turns out) this name, and the other associations of that person, are key.

My image is NOT interactive, but the following link IS. You can see Massachusetts is #1, Washington (State) #2, Colorado #5, Maryland #4, and NJ, here ranks #12 (follow the denser colors). CLICK~~>[//d2e70e9yced57e.cloudfront.net/wallethub/embed/31890/geochart-innovation.html Source: WalletHub

I know image is tiny! Click image to enlarge (if not on a device which has swipe features) or click here (won’t be annotated, though) link. Link’s url is also visible in image window frame at the top )

For general reference, another source, based off a Global Innovation Index (“GII”), an “evolving project” between Cornell, INSEAD (<=that Wiki, 1957ff) and WIPO (a UN agency), ranks nations by their innovation.

WalletHub then decided to, separately, rank (compare) US States as to how much they contributed to innovation.

For a visual point of reference, and a reminder that this type of comparison and globalization competition is going on, I’ve taken WalletHub’s offer to “embed this map.” Darker colors = more innovative states, ranked 1-51 (with D.C.). (To get to the interactive version, double-click link in image caption). WalletHub with its reference to the “GII” (Global Innovation Index) found while searching Twitter for the original tweet I saw a few days ago.

If you think about who or what is in Massachusetts (such as Harvard, and MIT) not to mention Washington (like, Microsoft (Nov. 12, 2018 at “BuiltInSEA”(as in “Seattle”) by BuiltIn Staff writer Alyssa Schroer; a friendly summary), Amazon…(who recently turned down NY. Detroit Free Press/John Gallagher, Feb. 20, 2019, more critical) read the closing paragraphs on downsides of major corporations setting up local HQ or here, it’d be HQ2).

Hard to tell who or what ‘BuiltIn.com” represents as a company; I’m not looking it up now, though.

The sponsored article, When Innovation is a State’s Main Industry, March 5, 2019 features NJII and downplays NJIT.

Which is which and who’s funding whom gets more than complicated on a closer look at their financials, by which I mean only the tax returns because audited financial statements for NJII (or NJIT) not posted, at least openly, on either site.

NJII is a recent 501©3 owned by NJIT, who is also its sole corporate member and controls its board. Without NJIT, NJII would be nothing. My question is, what is the real need for a separate entity? To engage in projects for which under public control, the public might have more say and more direct insight into?

NJIT is referenced in the NJ State CAFR as I mention below, but its numbers (assets, liabilities, revenues, expenses and organizational structure as would be shown in a proper CAFR) are not shown there except in aggregate with several other NJ public universities (Rutgers only merited its own column). A Wikipedia on NJIT is helpful also.

Foundation at NJIT. (Not referenced in the article, but it’s part of the package…) Being a public institution, like many public and private universities, NJIT has its own (privately controlled) 501©3 foundation showing gross assets of over $100M currently. This entity is also listed as “Related” under NJII’s tax returns, along with the public institution, both of course, tax-exempt. I’ll show these, but I also want to show the basic operating model, and why I’m red-flagging this otherwise exciting situation.

Understanding this may provides a backdrop for understanding similar themes and business models (though not so large in scope) targeting the family court system. It may help some people whose thinking is stuck in a rhetoric rut to look at an UNrelated situation for some of the labels, then go back to the family court arena, and “if the shoe fits” see where it should be worn: where these categories (labels) and the operating principles and practices to go with them, would also apply.

We MUST comprehend the difference between Public and Private Sectors within the United States of America, understand that blurring them is significant and has intent, and note carefully when accountability for public funds is moved fast into private sector — where accelerating the expansion of infrastructures and programs to run through them to benefit private, mutually aligned interests who must then sell (promote advertise, convince) all on how it WILL benefit the public, who are the primary and original investors.

We should by now know and talk about HOW the constant setup of more tax-exempt organizations domiciled in the (prosperous, developed, and highly-taxed) USA represents less taxes for corporations, and — whether or not the services compensate for this — more for individuals who function solely as employees.

Some exceptions likely would be those working in the public sector, and those working FOR the tax-exempt private sector. To the extent they retain employment and with it, connections (Career-curves) or can rotate from one sector (public) into the other (tax-exempt|philanthropic) — OR consulting for either of the above — those masters will have more to spare. Again, money is drawn to places where its owners pays fewer taxes, yet retain control in association with colleagues, friends, others who helped obtain it

Criminal syndicates, where such exist, my certainly have legitimate operations, but in general are NOT paying taxes on most of their profits either. It’s hardly fair competition being promoted IF and WHEN any such are involved; paying taxes are a normal part of (law-abiding) businesses’ overheads.

When we are talking New Jersey, awareness of that sector should not be discounted.

Major universities in other countries (I’m thinking particularly Oxford, in the UK) follow similar models research — incubate – license, commercialize, and share professionals among their universities to influence public policy in the “other” country. I see this all the time in just continuing to pay attention to welfare-reform-involved institutions (Princeton, Columbia, Yale, Cornell, and certain state universities in the Midwest and on both coasts) (and Texas) and their named and usually, sponsored, Centers, dedicated or interdisciplinary.

Oxford University’s incubator, which I blogged (link below — not on this blog) was originally called “ISIS” but I gather has since, for obvious reasons, changed that name.

That a business model is popular and exercised “globally” doesn’t make it right. Consider who controls the media and technology popularizing such models. I have.

New Jersey’s Innovation Institute promotional pages lead to more nonprofits and particular individuals (both on-site and off-site, when followed up on) which would be a research project just to understand. There is always more to understand, but generally, up to a few days of concentrated focus (reading!), keys to understanding it tend to surface, which by now (March 20), for me, have. I base what I have to say so far on both some fine print shown off-site (off the NJII and involved players’ websites), and what is specifically avoided mentioning in the promotion and sponsoring institution’s pages. Some of I have already said and shown on Twitter (link provided near top of this post; look about March 18 and following).

It was important to check, so I did: New Jersey Institute of Technology is indeed a public university and is referenced along with others under the State CAFR’s “Component Units.” However only Rutgers’ financials are listed separately, while all others are combined under “Non-major Component Units” (aggregated amounts). Link to The State of New Jersey’s Comprehensive Annual Financial Report, FYE Dec. 2017, published March 29, 2018 (meaning, FY2018 may be out soon. Url keywords “State.NJ.US/Treasury/OMB/publications…” See Note 18 as well as references in the MDA. Financials as I recall, about p. 48; Notes begin page 55)

As a component unit (of the State of New Jersey) NJIT, I think must have its own audited (“CAFR”) reports, but for all its technology expertise, I don’t see them being made easy-to-find (or even as a link under “Finance”) on their website. I have found some very old ones via Google Search, but not, so far, on actual college’s domain name. (The description on this CAFR references how the universities and colleges became autonomous in the state, versus being funded directly from the General Fund).

BLOG & TWITTER | CROSS REFERENCING MY OWN POSTINGS ON THIS TOPIC:

In recent months (not even a full year, I think), I’ve developed a tendency to start a topic on Twitter, attach some images and then continue it on the blog. As well as take blog excerpts to Twitter sometimes in response to ongoing threads. DNK how many actually read them, but better than continuous spontaneous re-writes when I’ve actually got something else on my radar, front-lobe focus as it relates to deeper themes.

This would be one of those times — the Twitter thread connected to deeply (relative to what I often produce on this blog, which while more raggedy is often deeper than standard journalism on anecdotal evidence + quote some experts, name their charities, keep that story line going on single-facets at a time of the family court systems). In posting some of the initial Twitter links (mid-March 2019) here, I still recommend, browse them only for the general flavor, then come back here for the more concentrated reading, with a systematic laying out the pieces, at the blog, here.

The situation is already complex and took me a few days to get answers on just one or two key questions (Who’s who, and why the connection). The themes are not new, nor really the practices. They’re just “more than before” and revved up on public funds, in particular, with this public (state-system) university. It also shows how one “Institute” may refer to a private nonprofit, and another “Institute” may refer to a state institution.

That the theme is also UN SDG’s on a Mid-Atlantic State bordering on New York City should also not be too surprising. It’s got major ports on both ends (Southern End — Baltimore). I’ve posted on some of Rutgers University’s contribution to that form of globalism several years ago doing the usual — tracking an odd nonprofit playing the wrong side (compared to what it was advertised as) of “Agenda21” talk in California. This effect and intent could be seen coming –and a short-cut to seeing it is not media consumption alone, but nonprofit drilldowns, an acquired taste and skill, but “Not Rocket Science.”

I’ve started a drill-down (as posted on Twitter) on one of what would seem to be a smaller player (partner) with NJII, “HealRWorld Foundation” and “Heal R World, LLC” and its interesting (“What the world needs now is more Shamaanism”) spokesperson who is also (not even mentioned on their website) married to a NJ CPA firm, but somehow has maintained a working relationship with D&B (Dun and Bradstreet) to access or create a giant databases, which it intends to license, and for which it’s already got trademarks (shown at USPTO.gov, “TESS” database).

(Michelle Vonetes Bongiovanni, on “Shift Network” (“Global One-ness and the New Business Paradigm“) website, spoke of her Peace Ambassador Training, specifically James O’Dea course.

WordPress for me has been temperamental in which images it would — or would not — upload. Without knowing why, including how much might be my own doing, I cannot guarantee when this post would be published, or when it is, whether sufficient “Show” might go with the “Show and Tell” process. However, enough leads and links are included that anyone with intent could go look him- or her-self, which is always the purpose of this blog, providing some motivation for individuals to do so.

When Innovation is a State’s Main Industry, March 5, 2019.

No author shown, it is a Bloomberg sponsored article showing NJII web frame top and bottom. Please read the whole article! Just some excerpts here, with comments between a few quotes:

[NJII] It is organized around industry verticals: biotech and pharmaceutical production; civil infrastructure; defense and homeland security; financial services; and health care delivery, with other industries added as the market develops…

Every one of those industries has direct connections to government funding, particularly with the size of the health care component, and with how many providers of database and telecommunications resources relating to it themselves (such as ICF, International — involved as grantee (and contractor) though itself already a multinational global for-profit corporation, in the “healthy marriage/responsible fatherhood” strategizing websites).

Think about the logistics coordination and communications required to wage war on foreign soils, something our country has major experience with in the 20th century.. and 21st… similar expertise would be required for nationalizing anything else — like healthcare, justice, education, criminal justice reform, child abuse or domestic violence prevention — major technical infrastructure and database maintenance is involved.

Financial services are connected because of SEC regulation and because among those served are the vast public institutional funds (i.e., pension funds, endowments, etc.), i.e., financial services as providers.

At least two of those referenced industries (biotech and pharmaceutical) have major ties, originally, back to the chemical industries key to U.S. industrial and military developments. I had previously noticed (and blogged on “economicbrain.wordpress.com” (“From Oxford to Harvard to D.C.: Feeding, Fueling — and Vaccinating — the World“) how among the largest nonprofits in Washington, D.C. was the GAVI Alliance (pushing vaccines on the developing world, with board of directors including not only royalty but also, Bill & Melinda Gates, and with its CEO Seth Berkeley, an obviously highly qualified individual also associated with patents for delivering injection-free vaccines, i.e., “PowderJect” and a goal of vaccinating ¼ billion children in developing countries by 2015). The post also referenced other major industry trade associations.

I would say it’s still probably safe to say that the pharmaceutical companies are among the largest and most highly influential companies on the planet. So it’s hardly surprising to find the State of New Jersey’s leadership eager to get in on this, especially as (despite it’s geographically great location, sharing the Port of New York, close access to Philadelphia and the D.C. area, and having universities like Rutgers and Princeton in-state). What NJ lacks in size (it’s the third smallest state) it more than makes up for in density (one of the most densely populated ones). It’s just “squished in there” between other larger or closer-to-D.C. states… And it was among the first 13 colonies with an interesting history. It boasts both the elite Princeton University, Fairleigh Dickinson, and public Rutgers is also well-known. Thomas Edison was there. Verizon’s HQ is also there, I think…

At a time when U.S. corporations are tightening their R&D budgets, and product innovation cycles are operating at lightning speed, NJII is filling a critical role in the state. NJII helps corporations develop idea-driven supply chains – by connecting talent with resources on a scale that is impossible for any single company to do…

“Our tagline is ‘A new model for business innovation,’” says Donald H. Sebastian, NJII’s president and CEO. “We leverage public funding to create the delivery infrastructure as an economic development priority that serves many. But we facilitate programming that helps individual companies grow their bottom line.”

How nice to help COMPANIES grow their bottom line. What does this mean to individual residents? Are their interests one and the same, really?

That’s the “hopefully it trickles-down” theory. All NJ residents will allegedly be better served by having their tax dollars increase companies’ (plural) bottom line, in an accelerated and incubated manner, more than it already is. Such representation of the common man (and woman)….

Critical to this approach, NJII brings together individuals from different disciplines who share a common purpose, explains Dean Paranicas, an NJII board member and President and CEO of the HealthCare Institute of New Jersey, a trade group** for the biopharmaceutical and medical technology industries. “The whole premise of NJII is to find solutions to real-world problems,” he says.

NJII is already seeing results. For example, Hackensack Meridian Health’s $25 million innovation center, in partnership with NJII, has supported several start-ups..

[[any and all emphases of any kind or color, added]]

**NJII is a 501©3. HINJ is also a 501© (membership). Co-occurring board memberships build networks, and these are private entities intent on accessing public funds while building their own representative groups commercially. The public served are “non-voting” but (because of public funds involvement) paying investors — and will be paying customers too. Some may also be employees.

HACKENSACK: Hackensack (until 1921 called “New Barbadoes”) is an “inner suburb of New York City” and is the county seat of Bergen County. At founding (says its city billboard) 1693, it pre-dates the United States of America, has a population somewhere over 40,000, is (currently) ethnically diverse, and seems to have two major health care centers (see “Footnote Hackensack, NJ” taken from both its Wikipedia, and “Hackensack.org” for more visuals, below). Bergen County is NorthEast NJ, which puts Hackensack, its county seat, just a bit northwest of NYC. It claims to be currently undergoing a Renaissance.

HINJ (HealthCare Institute of NJ) Overview, referenced in Bloomberg.com’s article on NJII 3/5/2019. HINJ is an industry trade organization established, it says, 1997. Notice also statement about who NJ is home to in this field (see also, diff’t link, its partners).

HealthCare Institute of New Jersey, a.k.a. “HINJ,” describes itself, and, in a sense, New Jersey, in addition to having been formed in 1997. “HINJ Overview”

New Jersey is home to more biopharmaceutical companies than any other state in the country, or any other country in the world. The biopharmaceutical and medical technology industry is a major factor in creating a thriving economy in New Jersey, as well as making our state a leader in research and development.

Founded in 1997, the HealthCare Institute of New Jersey (HINJ) is a trade association for the research-based biopharmaceutical and medical technology industry in New Jersey.

HINJ list of member companies includes: Abbott, Allergan, Amgen, Bayer, Bristol-Myers-Squib, Eli Lilly, Johson & Johnson, Merck, Novartis, Novo, Pfizer, Roche, Sanofi, and several others (<~~I used the abbreviated, not full, company names) That doesn’t include HINJ’s “Partners & Affiliates.”

NJ’s HISTORY OF ESTABLISHING FAVORABLE BUSINESS CORPORATION LAW, in an era when ANTI-TRUST (MONOPOLY) SENTIMENT WAS HIGH — 1890s to early 1900s (leading up to 1913, establishment of a central bank and the income tax)

On seeing this Bloomberg article, “When Innovation is a State’s Main Industry,” I also remembered how New Jersey became a favorite state for the original pharmaceutical and many other industries, surpassing even opaque Delaware for its industry-favorable ways to skirt the anti-trust laws, ℅ James Brooks Dill (1854-1910), who I previously posted on, in the context of complaining about the low quality of charitable databases and the impact of such a situation on accountability to the public for use of its (our) tax receipts, and hard-to-locate charitable entities composed of and networked with others composed of, state agency or department directors,

and, in general but showing specifically, the impact of this on accountability for all levels of public (i.e., public institutions, i.e., government entities’) funds.

Whether or not this can be changed, we should be aware of how innate this is to the system. Such knowledge would at least, I believe, mitigate being taken in repeatedly by the same types of nonprofit organizations which they, by design, cannot deliver — and typically are not reporting honestly, either.

The history of united business interests already by then controlling major public infrastructure in many cities skillfully avoiding attempts to skirt anti-trust | monopoly laws, for profit, goes back at least 110 years and reflects on who was commandeering basic infrastructure then and, to a degree, still is. That is, there still is intergenerational transmission of wealth and control (and political influence) by way of, essentially, monopolies and tax-exempt entities organized to conceal cash flow (and avoid taxation) from the people most in need of understanding it. This infrastructure doesn’t stop at county, state, or even national borders, although often people are stopped at such borders.

Obstructing Relocations Free Travel of Supposedly Free Individuals (if parents of minor children) at US Domestic State Borders:

In fact, through family law, divorce, domestic violence, and custody cases we also know how often one family member, if there are minor children, is prevented from even leaving a metropolitan region or a state, for reasons of “co-parenting” and of course theories of child development and poverty-theory as rooted in family structures (not public/private tax-exempt or tax-evasion structures).

There are “Parent Locator Services” for child support and ongoing encouragement for paternity registration at the hospital, even “putative paternity registration.” Other times, a parent can and does move away with minor children and completely cut off contact. Enforcement seems arbitrary, meaning entire families are held hostage to that decision-making. Some mothers have their children taken away at birth…in the hospital, involuntarily, without necessarily being on drugs or having a history of drug involvement. Even WITHIN the United States of America… Meanwhile, businesses and public institutions (and their investments) certainly can incorporate almost anywhere, including overseas.

In looking for my previous posts (turns out there was also a page) on The Corporation Trust Company, James Brooks Dill, and the history of professional registration companies (i.e., in general the NJ favorable climate towards industries who don’t want too much about them showing up on the state registries databases) on the New Jersey Innovation Institute (Tweet and related article, then tax filings)..

..I was also reminded how some of the same organizations and their owners collaborated around issues such as tobacco (anti-smoking campaigns) and how the Laskers (advertising wealth), pushed forward the creation and subsequent major expansion of the NIH under the United States Department of Health and Human Services (as it’s now called). My prior posts which reference The Corporation Trust Company (a professional registered agent) and the long-deceased but influence still felt, J.B. Dill, contain sections writing that up also. Fees for incorporating in NJ helped pay off state debt at that time.

James Brooks Dill (1854-1910)’s interests may be seen by a list of his books at “Online Books Page.” Having said that, here’s a link to the Copyrights and Licenses page of this book (including some of its sources) by creator (at UPenn?) John Mark Ockerbloom. For more, see Footnote “OBP/James Brooks Dill”.

This is background to the current situation, and symptoms of it. Over a century ago, he was wanting a national corporation law to avoid “sectionalism” and the states warring for corporate revenue — as NJ is doing, it seems, successfully (and aided by some of his creations and expertise), regarding pharmaceuticals and public research universities to incubate nonprofits and provide talented, skilled workforce to operate and work at, all of which is collectively beneficial (is the theory) for the state overall.

(Public Domain now: UMichigan has Yale Law Review reprint of (NJ lawyer James Brooks Dill) address at Harvard, 1902, “National Incorporation Laws for Trust” (<=same shortlink=>http://bit.ly/2HIsNXo, I found today ℅ that OBP list, but I’d read and posted on this about a year and a half earlier).

SEE POST TITLE: “Interlocking, Dysfunctional Definitions, Cont’d: “NJII, a NJIT Company,…”

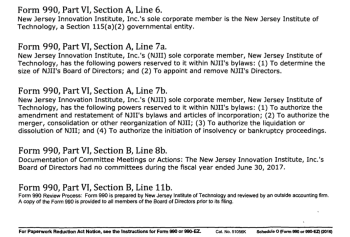

Just to list the THREE entities mentioned (after I decided to find out who or what was the fine print reference to “an NJIT company” on the NJII web pages), the tax return Schedule R, Part II, though in fine print, clearly references two tax-exempt entities, and their EIN#s.

One, you won’t find under “Foundation Center” because its basis for tax-exemption is being a public research university; however like many public universities, it also has a foundation which is there. That foundation is a second one created in 1959 and which, I’m just finding, holds over $100M assets, making me wonder why a third one called NJII was needed in 2014 — and how many more might have been formed, spun off over the years.

What’s more the one labeled (by FoundationCenter.org) as “NJIT Foundation” (written out) then “NJIT” (written out) without the word “Foundation” is in fact legally called “Foundation At the New Jersey Institute of Technology.” The nonprofit providing this information (tax returns show recent gross receipts $26M and it’s been around for years) continues to spit out wrong names on name searches, while provision of searchable databases seems to be a main source of its revenue.

Nothing new from that source (getting organization names wrong makes name-searches come up empty. A person would have to first, locate an EIN# from a separate source — which I did, that Schedule R — then look up the EIN#.

Perhaps some of the major database and computer talent at NJIT — or, the private CIT (California Institute of Technology in Pasadena, or at “CalPoly” in San Luis Obispo, California’s “Sunny central coast” (“National ranked public university with connections to industry in the Bay Area and Southern California” “small classrooms” “Learn by doing..”) might help solve this problem over at Foundation Center, if proper motivation could be provided at any such university laser-focused on moving innovation into commercialization, faster.

CalTech history/Milestones (basically, by Presidents): Founded 1891, finally admitted

“female undergraduates” in 1970, under Harold Brown, after it had more than doubled in size (acreage and faculty) and experienced post-WWII Growth (1949-1969):

…Most significant, perhaps, were his efforts to open Caltech to female undergraduates. In 1970, the Caltech Board of Trustees voted to admit women. However, the board made the admission of women conditional upon the building of new student houses, which they knew would take at least two years. Not wanting to wait, Brown pressed for an arrangement that would set aside corridors for women in existing houses. Because of his persistence, Caltech began admitting women in the fall of that year.

“Cal Poly, San Luis Obispo” began admitting women (1903-1930), then banned them for 26 years until 1956. Interesting history at Wiki (no quick link to history provided at actual website) and apparently average GPA is high (3.92). It’s focused on undergraduate education. See also wiki section on “Relations with local community” regarding housing — as the school expands, lower-income families and individuals are getting pushed out by students, and the city poverty rate is 27%. Despite that it seems like major on-campus housing projects exist.

Female admissions[edit]

In 1903, Cal Poly San Luis Obispo opened as a coeducational school with 20 students enrolled, 16 new male students and 4 new female students.[19] In 1930, Cal Poly San Luis Obispo banned women from the entire school until 1956 when it once again began admitting female students. The university remains coeducational today, with women constituting 46.7% of the Fall 2015 total student population.[20]

I referenced California colleges knowing that Foundation Center has an office in San Francisco. However, it’s home state is New York. Looking it up at CharitiesNYS.com, I see that it is not claiming any public funding (government grants), just private. I should set up a separate page for this entity on the blog, with that information.

Here is the state-level Registration (cover sheet only shows; to see more, you have to pay!) for the “Assets over $100M foundation” I referred to:

FOUNDATION AT [NJIT] (mislabeled), EIN# 221714037, established 1959..

| ORGANIZATION NAME | ST | YR-end | FORM | PP | TOTAL ASSETS | EIN |

|---|---|---|---|---|---|---|

| New Jersey Institute of Technology Foundation | NJ | 2016 | 990 | 49 | $102,903,578.00 | 22-1714037 |

| New Jersey Institute of Technology | NJ | 2015 | 990 | 50 | $104,167,207.00 | 22-1714037 |

| New Jersey Institute of Technology | NJ | 2014 | 990 | 48 | $101,559,676.00 | 22-1714037 |

| ORGANIZATION NAME | ST | YR-End | FORM | PP | TOTAL ASSETS | EIN |

|---|---|---|---|---|---|---|

| New Jersey Innovation Institute

[THIS link obtained from IRS.gov, not FoundationCenter, which doesn’t have it up yet. TAX RETURN WAS SIGNED ALMOST A YEAR LATE< ONLY in MAY, 2018 (YE is JUNE)] IMAGE GALLERY (2X2) below this table has excerpts. |

NJ | 2017 | 990 | (see link) | $3,583,635.00 | 47-1042118 |

| New Jersey Innovation Institute, Inc. | NJ | 2016 | 990 | 38 | $2,815,662.00 | 47-1042118 |

| NEW JERSEY INNOVATION INSTITUTE INC | NJ | 2015 | 990 | 35 | $709,738.00 | 47-1042118 |

-

- NJII Tax Return FY2016(YEJun2017) only signed May15 2018 (obtained from IRS’gov) Sched O shows NJIT control

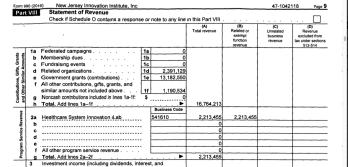

…Just to point out, in 2017, this version has “changed its tone” to actually describing what they do. Prior two tax returns (electronic filings ) just brushed by that section with little detail. You can see (Image 4) $13M of government grants. Not shown (page2, click link provided) about $13M of expenses for clearly its largest current project, “iHealthcare” Labs. $13M in, $13M out.

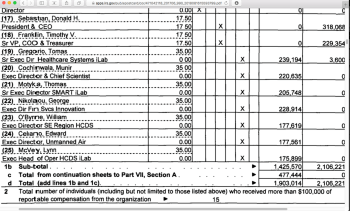

I posted part of Schedule O (Image 1) to establish who clearly controls NJII, and a section of Part VIIA of the tax return, showing totals of paid officers (3rd column of x’s from left) or highest paid employees (5th). The first column of $$ represents paid by NJII, the second, paid by “related organization” probably NJIT (as the Foundation doesn’t, I think have major employees). I also wanted to show George Nikolaou, $228K for “Exec Director Financial Services Innovation” as his name came up on among the top links on this post associated with HealRWorld and the UN SDGs (as I recall). From that NJII.com link:

According to NJII’s Executive Director, Financial Services Innovation, George Nikolaou, “NJII operates the largest tech/life sciences incubator/business development center in NJ, the Enterprise Development Center, and has established a cluster development business acceleration program – HealthIT Connections with funding from JP Morgan Chase’s Small Business Forward initiative to help scale up Health IT companies accelerate their development. NJII is in the process of expanding its Technology Adoption and Acceleration programs for both large corporations and small businesses within the framework of its Innovation as a Service (IaaS) offerings.”

…

SEE POST TITLE: “..(how, exactly, NJ became) “the State of Innovation.”

(See my October-November, 2017 posts on this. Showing how I discovered this. Who controls which databases, and from which country. Corporations are bought and sold, as was those involved in seeking to establish a single interstate registration portal for charities, to make life easier for those interested in setting up in multiple US states. WalterKlowers.com got this one)

November, 2017 seems to be the year that the founder of “CT Corporation’s predecessor in NJ started getting under my skin, while I was looking at the topic of Charitable Registration Databases. I had both a post and a page on this.

Here’s from the post, and I recognized that my habit of simply doing drill-downs on, for example, logos which didn’t seem to fit the context (there, it was “Bizfilings”) which led to this information. Because I have so much occasion to look up charities myself in various states, I then also put up a page. Both this post and the related page explain (for the patient!) how New Jersey, specifically, became a “go-to” state for industries seeking to maintain corporate offices in ANY or ALL states (with or without having actual business there), but skirt being actually caught in anti-trust or monopoly law. Given the times, this made James Brook Dill popular, and the State of New Jersey, well, “flush,” it seem. It was surpassing even Delaware for a great place to set up shop but not have to reveal too much about just how.

As a personal investigative blogger, I have noted over time (it comes up periodically) that one doesn’t get very far at all researching organizations in NJ from its Secretary of State database. It’s just somewhat opaque — never a good situation for the inhabitants.

Post Title: About MRFP, Inc. (NAAG/NASCO’s “Single Portal Initiative” for MultiState Registration and Filing by Charities — except, apparently, for MRFP, Inc, NAAG, and NASCO). Also See my New Page (publ. 11/11/17) on SimpleCharityRegistration.com [This post Publ. 11/18/2017](case-sensitive shortlink here ends “-7X8”).

Subtitle: Who’s Regulating the Regulators? Why are they exempt from the rules they exist to enforce? Wake Up, People!!

Those Acronyms in the Title: “MRFP” = (see post title).* “NAAG” = National Association of Attorneys General. And “NASCO,” it’s said, is “National Association of State Charity Officials.”**

- *Technically speaking, “MRFP, Inc.” is a business name, not an acronym, but it does seem to represent the phrase”MultiState Registration and Filing Portal.”

- **“Proof of Life” or business entity personhood is just not found so far, despite other similar or interested entities, even the IRS.gov itself, publicizing, positively, the name in full and as an acronym as if a creditable point of reference and a legitimate entity with a legal domicile somewhere in the USA or one of its territories.

- **If so, if NASCO exists, where is its incorporation or charitable registration; does it even have an EIN#? If yes, then where are its tax returns or even a single Form 990-N? Or where is it on someone else’s tax return as its fiscal agent?

- **…Speaking of which, I’d ask NAAG (i.e., a NAAG Tax return/Form 990) which seems to be acting as a fiscal agent for some NASCO functions — but where are NAAG’s returns (even though NAAG’s EIN#, no thanks to NAAG’s own website, was eventually found)??

For an example of references to NASCO (as well as apparent confusion, as ever, between the puppet and the puppeteers, that is, the creation and the creators — specifically a business with a product, and the product itself), these next two links to a single document written as if responding to the “RFI” (Request for Information) on the Single Portal Initiative, showing the logos for “GUIDESTAR” on the left and “SimpleCharityRegistration.com” on the right, and the found document was actually posted at MRFP, Inc. …

[SCR.com] See Partners list near bottom of image: Guidestar, BizFilings? Nat’l Council of Nonprofits Council and Perlman & Perlman Guidestar provides a nonprofit database I used before discovering Foundation Center’s results provided in easier to print tables..

By the time you get through my page on this, you’ll see that SimpleCharityRegistration.com also adds fully FOUR logos labeled “in partnership with” of which one is Guidestar, and another one (BizFilings.com) provides us clues to the whole mess that predates the federal income tax, and how corporate law was adjusted (and by whom) to get around anti-trust laws of the same era. It’s fascinating information and definitely turned on some of my own lights as to the phenomenon I’d already observed of effective monopolies (or “oligarchies”) within the nonprofit sector and intersecting with government itself.I also discuss several aspects of that situation here, adding some new links.

…

And, the page to go with this: I felt it that important.

I also thought such a resource would be a convenience. i wonder if one was ever developed.

…

Page Title: State-by-State Charity Lookup Links (from SimpleCharityRegistration.com’s March 2017 WordPress post) Started Nov. 8, 2017, Published Nov. 11; intended for my “Vital Links” sidebar menu. Case-sensitive, generated short-link ends “-7Vm”

Delaware Corporations Division showing 12/12/2013 filing date for (“MFRP”) and its registered agent business.

I intend this page as a service to individual researchers of charities. And a general alert on new developments by at least two “where’s your Tax Return and Corporate Registration?” entities coordinating the state charities regulators through associations whose primary members are high-level state employees, and the internationally-connected Corporation Trust (“CT”) Company syndicate, now apparently run from or at least headquartered in the Netherlands. What they want is digitized Forms 990 — something there are definitely pro’s and con’s to — for better support of (in this case) their “MultiState Filing and Registration Portal, Inc.” projects (“MFRP”) incorporated in Delaware in 2013; I haven’t found its tax returns yet either, although it’s classified as “Exempt” and described as “nonprofit.”

Both my Page & Post sometimes get the nouns (and corresponding letters in the acronyms) switched, as above, MFRP when it’s actually “MRFP.” First they must register, then continue filing as required state by state. … Checking up on this entity again, under its correct word order legal name, for this post (in March 2019), I found it has another registered agent. Note: “entity type: “Exempt”)

This situation should be interesting. Having a brand new (almost) Institute (501©3) NJII to start with where already the “NJIT”** connection is being fine-printed and down-played, I felt we should front-page and again, look a lot closer at how these things develop, and — when it comes to 990s — account for and label their cash flow, interrelationships and (as requested by the IRS to do in SPECIFIC format) “Program Service Accomplishments.”

**(NJIT, per itself and Wikipedia, is a long-standing public university with land grant, sea grant & research status. As a public university it should be filing CAFRs, or showing up under the State University System’s CAFRs. In addition, I already see a “Foundation for NJIT” 501©3, a common situation)

Add to this how NJII’s most recent tax returns are just now showing yet at FoundationCenter.org, which makes me wonder how many different places must one look to find what the IRS already has, and is supposed to cough up for public viewing, when the filing entity is classified as tax-exempt?

I am writing Q1 2019.

The latest tax return readily available (at the above database at least; FYI I’m not a subscriber; do subscribers get more current info?) for NJII reads “2016” which isn’t too bad until one realizes it represents Fiscal Year 2015, which ended June 2016, almost three years ago. Between Year 1 and Year 2, its gross receipts increased about ten-fold (roughly*: it was $1M then over $10M; look at FYE2016’s Schedule A). What’s happened for FY 2016 (ended June 2017), FY2017 (ended June 2018) which would normally mean a tax return should be reported by the end of 2018 at least….

*The point is to reference a major increase. If it was important to that statement to show exact amount of major increase as an indicator of previously-organized funding, I’d make the rough estimate closer).

Add to this, even a beginning look at various parts of the first two (available — the “Initial” and the next one) IRS tax return contents, including their schedules, shows money moving back and forth on various pages between its sponsor (NJIT) and sole corporate member (NJIT) who advanced NJII $500K, but received a grant of over $450K from NJII; on the other hand some unknown entity (like NJIT) provided — acknowledged in Form 990 Part XI (Reconciliation of Tax Return to Audited Financial Statements) as having “Donated facilities and Services” of over $450K (IRS form doesn’t require this Line 2a in Part XI to be detailed, and it isn’t. Donor is not named). Some amounts were $463K, some $453K. I do not have exact recall of which amount was in which part which year, but will be providing links if not images also, so am summarizing “generic” details.

In other words, looking at just a single page in any tax return, it’s just: money granted (an expense), money received (revenues|contributions), money earned (revenues|here, program service revenues, i.e. performance contracts, leaving “for whom” open ended unless tax returns specifies), money borrowed (a liability), or more contributions not shown on the tax return but shown on the audited financial statements (donated services and facilities).

When these amounts, at first glance seem both similar in amount and involving the same (or apparently the same) “other” — like NJIT (and the street address is “℅ NJIT, which is also a related tax-exempt entity, and on which one director’s spouse consults (specifics: See “Schedule L”), the question comes up, IS NJIT really different (and, if so, how different?) from the offspring it controls, NJII? And if barely so, why spin it off in the first place?

Another thing already evident in NJII’s first two IRS returns– they (“it”) must not be expecting much oversight, as no attempt to even break down description of tax return’s main question on Page 2 (Part III, Lines 4,a,b,c and “d” if more than three substantial categories of “Program service activities”) is made on first or second year of activities– it’s a boilerplate (block-copied) response showing purpose — not accomplishments, although the tax return’s category is “Accomplishments” specific to THAT YEAR and “BY EXPENSE.”

In this sense, there’s little “innovative” about NJII’s filings. They’re not the first, and will probably not be the last, nonprofit hidden under university umbrella, nominally separate from the university, sort of, but controlled by it, making operations that much harder to account for when “accountability” is the goal, not promotions. Why would these means be necessary, and what “end “justifies them?

Attracting yet more business to a state already known for its favoritism to business through corporate law going back a century, and which I at least experientially know (like Delaware) runs a secretary of state business entity search site which is borderline useless to a serious, but unsponsored, investigator, which members of the public ought to become as part of basic civic responsibility for what they’ve (we’ve) been forced to invest in every time we go to work and are paid, or consume goods necessary for life, pay bills, etc.

Delayed production of tax returns is also a tactic. There’s no real need to delay so far past any deadline.

I’d like to show that in this post. In doing so, I also go back a year and (as of starting this post) a quarter in my own writings to talk about the setup of business and corporation law to have effective monopolies and trusts without actually, technically, getting caught at it (before, if caught, they have sufficient resources to pay off any fines and go back to business as usual).

I also already see that by “Year 2” the main activity is Healthcare related. This bears further investigation, including likely further than I could do individually. But I believe I can at least put out one or two alerts — THIS time, near the startup of another NJ University-based “shell” (?) entity covering for its sponsor university, though functioning in the private realm with too little oversight.

FOOTNOTES:

Footnote OPB/James Brooks Dill (b. 1854)

OBP James Brooks Dill (Image from UPenn’s Online Books Page, viewed 3/17/2019)

OBP James Brooks Dill (Image from UPenn’s Online Books Page, viewed 3/17/2019)

OBP Copyrights and Licenses (Image from UPenn’s Online Books Page, viewed 3/17/2019)

This Online Books Portal was helpful in illustrating what topics the author was writing on and for interested readers to follow up if they choose. Thanks to individual who cataloged it and took the time to clarify the purpose, i.e., Mr. Ockerbloom. It’s been two years since I was reading on this author (not through this source, to my awareness) and having a list of books to illustrate the general topics was helpful in producing this (public-interest) post without re-creating the original look-ups. I have studied copyediting, and worked on this blog for many years, so I do understand that the skill of indexing and abstracting is important and valuable. I DNK how much may be done via “Artificial Intelligence” or data analytics/semantic software now, but doubt it’s as good as live human involvement, which represents a lot of work.

Moreover, the human beings which do that work have exposure to the information they’ve researched, which makes them also a resource to others.

FOOTNOTE HACKENSACK, NJ:

Link to their latest “Audit” which is actually and odd-looking (if you’re used to reading CAFRs in more standard format) (listed under “audits” not under “Financial Statements”, a drop-down menu). But awareness it IS a “CAFR” is shown in its url, which reads “CAFR2017”

Which is most notable for NOT using a GAAP (Generally Accepted Accounting Practices in the US). It is still early 2019, so, I can now understand why perhaps a FY2018 CAFR is not uploaded yet. I was also curious about segregating its financial statements into “NOT under “CAPS”” (the phrase used in quotes 16 times, but only shows up on the number tables, and is not referenced in notes. I could find no phrase translating its meaning in the Notes. The closest anything comes to it is “Compensated Absences and Payroll Benefits” which doesn’t match because of the final “B” (and doesn’t match as to size). Interesting reading.

Leave a comment