Published May 24, 2017, with a “partner” post “Schools for the Children of the World: Great Theme — Now Here are the Forms 990” (case-sensitive short-link ends “-6Qq”). Both are under 10,000 words. I do not know for sure, but I’ll bet that automated word count may include captions to images, and I have a lot of images with captions on both. This one was posted and most of it written first.

For example, UCB CC+S [Jeffrey M. Vincent*], 21stCSF [Mary Filardo],** NCSF, BEST [Ford-sponsored], SCW [DeJong] (**incl. Scientex, African Science Institute [Eddie Neal])

*Deputy Director. There is also an executive director Deborah McKoy, Ph.D., at CC&S, but in this “New National Initiative, the deputy director’s name is mentioned.

These three images relate: 21st Century School Fund, a DC “Superintendant’s Task Force” showing a co-chair to be Eddie Neal of “Scientex,” repeated with larger context, below.

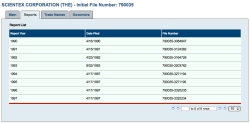

Of interest — a search for any current version of “Scientex Corporation” drew a blank — but three entities with that name showed up in D.C. (none current), while a bio for Scientexedu advertising for tutoring, referenced the African Science Institute in Oakland, CA — which is no longer valid either, and there were two entities, not just one. The filing track record is well below substandard.

See list of Task Force on Education Infrastructure images below.

I just now took a quick look for the right column’s “New Columbia Community Land Trust” Pamela Jones, Esq.), who was Co-Chair. The Land Trust (“NCCLT”) is co-located with a historic Black Catholic Church (St. Augustine’s) in D.C. which goes back to 1858.

What this representative from NCCLT, involved in the buying and selling of land and land sites, and developing them, is doing on a Superintendent’s (of Washington, D.C. Public Schools) Task Force belongs in the body of this post — or some other post — before it derails the introduction… But looking at it, like looking at any of the other participants, is part of basic drill-down homework, and rarely fails to inform, amaze, or bewilder how such things can take place over time.

(The trust street address matches a historically Black Catholic Church, St. Augustine’s parish, in D.C., and they are buying, developing, and selling land to lease to the poor, with only two employees and no listed website, since 1991. Just in time for that Task Force… and has some subcontractor (?) involvement with the address 5929 Georgia Avenue NW, i.e. where a large Wal-Mart store opened in 2013.) (“Lawsuit filed over status of historic status of future D.C. Wal-Mart store” Dec. 2, 2011 in BizJournals.com under “economic development.” )

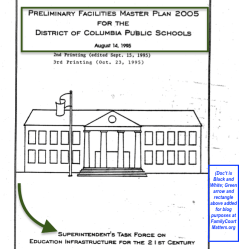

Click image to see larger (DC-based, 1995) Superintendent’s Task Force on Educ Infrastructure for the 21st Century

Click image to see pp9-10 showing 1994 reference to 21st Century School Fund before it incorporated, and other possible impetus for this Task Force..(1989 rept, 1992 lawsuit re: fire codes in DC public Schools),

(DC-based, 1995) Superintendent’s Task Force on Educ Infrastructure for the 21st Century

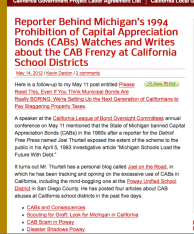

You can read this post before or after hearing from my other post (same-day publication, two-in-a-row) about the “Capital Appreciation Bond” fiasco which was outlawed in Michigan after exposure for royally screwing residents for school renovations (interest rates 572% in the long haul) by the Detroit Free Press writer Joel Thurstell, as occurred? 1988-1993, however the practice has already migrated to California and is in place at about 1,000% interest (or payments 10 times the principal)….. One link and two images on that:

Reporter Behind Michigan_s 1994 Prohibition of Capital Appreciation Bonds (CABs) Watches and Writes (KevinDayton May 14, 2012 post @Laborsolutions’com) (this pdf has active links to other articles by Thurstell as referenced by Dayton, who suggested he might want to do a California tour. (That link and two images below in the other post also).

Image 2 of 2 (for same pingback page), image here not clickable — use Image 1.

Image 1 of 2; if related link no longer active, click image to view this “Printed to pdf” version of same page for active links to the other Joel on the Road articles on CAB!

…. After reading my other post (published same-day), you will probably also need to admit— which I proved simply by quoting the sources — that the CAB situation alone (even without all the other dredged-up information from tax returns and corporate filings/mis-filings) reflects upon UCBerkeley’s Center for Cities + Schools (“CC+S”) judgment OR its overall purposes, as part of a self-selecting “Leadership Team” choosing who gets to be on their “Educational Facilities Planning Work Group” for a “New National Initiative,” and from their framing the questions, and facilitiating the work groups too. (More on all that in this post).

CC+S Staff and Affiliated Faculty,( viewed today from “Who We Are” link)

Deborah McKoy, PhD, MPA, Executive Director Jeffrey M. Vincent, PhD, MCRP, Deputy Director Amanda Eppley, MCP, Y-PLAN Program Director Shirl Buss, Y-PLAN Creative Director || Myrna Ortiz, Y-PLAN Oakland Coordinator and Coach [B.A. Urban Studies UCBerkeley) Ciera Dudley, [same degree, with CC+S here since Jan. 2016] Y-PLAN NYC Coordinator and Coach [and 1 operations manager, several research assistants or associates, looks like all women; no links provided].

Interesting only one male staff member out of all listed. The “||” separates what appear to be more highly degreed and possibly experienced members of staff — the latter two have only B.A. in Urban Studies from UCB, and are probably older too. Y-PLAN is obviously for greater youth involvement in this social change movement regarding Cities and Schools.

Affiliated Faculty:

- Judith Warren Little, Former Dean, Graduate School of Education, UC Berkeley

- Rebecca Cheong, UC Berkeley, Principal Leadership Institute, UC Berkeley

- Walter Hood, Professor & Former Chair, Landscape Architecture and Environmental Planning, UC Berkeley

- Malo Hutson, Assistant Professor, Department of City and Regional Planning, UC Berkeley

- David Stern, Professor Emeritus, Policy, Organization, Measurement, and Evaluation, Graduate School of Education, UC Berkeley

- Nora Silver, Director and Adjunct Professor, Nonprofit and Public Leadership, Haas School of Business, UC Berkeley

- Bruce Fuller, Professor, Graduate School of Education, UC Berkeley [no link shown]

Why does this reflect on their group-dynamic judgment and/or motives (notice, I didn’t say, professional or academic qualifications)?

Among the Educational Facilities Planning Work Group as facilitated by one person from UCBCC+S and another from the D.C.-located “21stCSF,” was a single “SCW” –meaning “Schools for the Children of the World, Inc.” (a nonprofit associated with the DeJong family (William, Brent (TX?), Matt (?) and at least Todd (CO) and Charles Newman, architecture firm in Naperville, IL, among others).

DeJong-Richter had recently (October 2016) merged into “Cooperative Strategies, LLC” in Irvine California, formerly an individually-owned (said the press release) Dolinka Group, LLC, run by Benjamin Dolinka, long-time advisor to many California School groups.

And simple web searches of Benjamin Dolinka resulted in several articles on those CABs.

But that post had a lot of tax returns, which bear reading, not just news articles, as I also connected the DeJong family to contracting with the Beverly Hills Unified School District — while running semi-annual trips to the Honduras, Haiti, and Africa to help (especially as to the Honduras) with a master plan (nationwide — just like is planned in the US, only coordinated by a network and of course, the National Council on School Facilities, incorporated only in 2013 in D.C.) — to build or repair schools in Central America and Africa. Meanwhile, in its earlier years, just from my mental storehouse of “Huh?” moments reading tax returns — early in the 21st Century School Fund tax filings — seeing grants going to Chile; so make that “…and South America.”

So, I can’t say for certain whether this mentality of “equitable distribution of funds for school facilities renovation” is actually a “Robin Hood” (rob the rich to help the poor of the United States of America low-income urban neighborhoods). It does seem like a major robbing, long-term, of the US homeowners when it comes to those Capital Appreciation Bonds, while enriching the facilitators — such as advisors.

. . . .So, I was exploring one of the UCB CC+S’s initiatives’ uploaded 2016 publications called: K-12 School Facilities: Planning, Siting, and Joint Use (<= announcement page, and from there,) a New National Initiative: Planning for PK-12 Infrastructure: Adequate School Facilities for All Children (<=working group summary and initiative overview. Images are shown below, so don’t feel it has to be memorized to read the post).

Today’s other post, Schools for Children of the World, Inc. — Great Theme, Now Here are the Forms 990 (case-sensitive short-link ends “-6Qq”), follows up to what caught my attention as an apparent nonprofit mentioned in affiliation with one of the members, “Bill DeJong” of “DeJong & Associates” and “Schools for Children of the World,” (“SCW”)** on a working group (one of six “cross-sector working groups” for this initiative, the group it called “Educational Facilities Planning Working Group“) as convened by a “Leadership Team” for the “New National Initiative: Planning for PK-12 Infrastructure…” — a Leadership Team based in California, Washington, D.C., and Colorado, with the apparent purpose of establishing mutually controlling and nationalizing the planning for PK-12 School infrastructure and a new association (NCSF) based on membership in the planning facilities, at state or territorial level, which would have major input into pushing for repair, maintenance, and more funds for the same.

**Yes, “SCW” (it has an acronym, too!) is a nonprofit, (EIN# 56-2358076).

Above, I underlined both organization and initiative names and terms which UCB CC+S and its Partners (and Advisors, and their collaborating initiatives such as “BEST” (for “Building Educational Success Together,” sponsored with $1M in 2002 by the Ford Foundation and led by 21stCSF — see next images, but not the main topic here) and nonprofits, at least one (Neighborhood Capital Budget Group) which is “no longer with us” (IL revoked its corporate status for non-filing)…) are using as call-to-action labels symbolizing the desired functional purpose(s) in the mutual-promotion (sales, public relations) language of the public/private network.

2002 Press Release on 21stCSF website, earlier version, acknowledges Ford Foundation backing. See also 21stC School Fund Forms 990 of this time, some on my 5/21/2017 post below) Click image as needed to read.

The purpose of this networking is admitted within the networks and, said to be a good thing, changing the paradigm, by those in the network.

This language is common to most “cause-based” rhetoric, as “cause-based” literacy in practice is the opposite of “accounting-based” literacy, and tends to ignore the latter, while gesturing towards it at times to support “the cause,” whatever that cause might be, THIS decade, or year, or this time around. As I said in recent posts, “the tension continues between…” this language and the one we should be speaking IF balance of power between those taxed (i.e., your basic employees) as a national sector and those people working with or for (or simply ARE) those who historically have had access to the most tax-receipt AND investment- financed assets and figuring out ways to expand the privately-controlled, tax-exempt nonprofit sector redistribute the cash flow, and justifying the process, to continue forever as a politically influential sector.

When looking at clearly inequitable existing cash-flow distributions, it’s not enough to show a serious problem. In consenting to any wide-scale solution for it, we still have to pay attention to “the problem-solving traffic directors,” and look at how they handle their own affairs, and choosing partners to work with.

MOSTLY (I speak in general and from my experienced both networked, dealing with a specific other course — the family courts and what goes with them (domestic violence, child custody, child support, federal HHS grants to promote marriage, fatherhood, co-parenting, and frame criminal violence as a relationship and/or health issue, triage it, and forward to “treatment providers” (or, behavioral change experts…). It is equally true of Schools Reform (“Closing the Achievement Gap”) or School Facilities Planning Reform, (“Closing the School Facilities Infrastructure Investment Disparity gap” essentially).

paradigm (n.)  late 15c., from Late Latin paradigma “pattern, example,” especially in grammar, from Greek paradeigma “pattern, model; precedent, example,” from paradeiknynai “exhibit, represent,” literally “show side by side,” from para- “beside” (see para- (1)) + deiknynai “to show” (cognate with Latin dicere “to show;” from PIE root *deik- “to show,” also “pronounce solemnly”).

late 15c., from Late Latin paradigma “pattern, example,” especially in grammar, from Greek paradeigma “pattern, model; precedent, example,” from paradeiknynai “exhibit, represent,” literally “show side by side,” from para- “beside” (see para- (1)) + deiknynai “to show” (cognate with Latin dicere “to show;” from PIE root *deik- “to show,” also “pronounce solemnly”).  Related: Paradigmatic; paradigmatical.*deik- Proto-Indo-European root meaning “to show,” also “pronounce solemnly,” “also in derivatives referring to the directing of words or objects” [Watkins].

Related: Paradigmatic; paradigmatical.*deik- Proto-Indo-European root meaning “to show,” also “pronounce solemnly,” “also in derivatives referring to the directing of words or objects” [Watkins].

(Many thanks for “OED” here, I quote them often, to):

We shouldn’t need constant translation from people operating, or claiming to operate, in the public interest as a reason for existing, and a reason for existing especially as a 501©3 or contractor with a 501©3!! But, overall, unless or until this language is not just understood, but also spoken, by those not IN on the networks already (or who may be working for them without comprehension of the larger scope — a job’s a job, right?), we do!

A systemic alteration in labeling for paradigm shift is an intent to change “basic operating principles.” When that shift is AWAY FROM fiscal accountability and calling things what they are

using a common language of identifiable “comes from and goes to for what authorized purposes” and “what are the evolving, revolving balance sheets showing about stewardship?”

(such as the language used to account for public funds with regard to these coming from individuals regularly as a consequence of living and working in the USA, and for the functions, operations, and cash-flow of IRS-exempt, or heavily reduced-tax entities)

relating to government entities and their operations, that is a “paradigm shift” AWAY from the basis for public-supported government itself, which is to say, the basis for giving governments the power to tax.

Again, one of three key indicators of “governmental character” when judging whether some entity is or is not a governmental one, is the power to tax — I showed this recently from a U.S. Census of Governments Document, which came up specifically after the 21st Century School Fund’s spinoff nonprofit, “National Council on School Facilities” citing statistics, used a piechart without a specific link or cite, from the U.S. Census of Government spanning 17 years (1995-2017) and admitting its data skipped 1997, 2001 and 2003, and the U.S. Census of Governments context also does not take into account regional Joint Powers Authorities (or Agencies) that crossed state lines (!).

Click Annotated Image To See *~~~

Another characteristic of government listed right there is “a high degree of responsibility to the public, demonstrated by requirements for public or for accessibility of records to public inspection, is taken as critical evidence of governmental character.”

Gov’t Character (from Definitions part of 2012 US Census of Gov’ts) CLICK IMAGE if needed to read full-sized.

Attempting to shift the organizing paradigm, here, that is for School Facilities Planning and Purpose (joint-use) Power away from accountability to ALL the people taxed for those projects, or by those funding those projects, and to out-of-reach, inaccessible specific financial records, and doing this under a paradigm shift purpose labeled, in essence “more power to the people (to “communities”), is an oxymoron — it’s a wise stupidity, or joke. The “joke” is on the community — not the leadership of those entities pushing for the shift.

The larger tax-exempt foundations (often filing Forms 990PF, not Forms 990 — which do not have to report EINs# for each grantee, from what I can tell — have no problem admitting their paradigm-changing purposes (for a example: MacArthur Foundation’s “Models for Change” targeting, among other things, juvenile justice systems).

Our job as individual citizens (if the shoe fits, wear it!), to “Keep Our Eyes on the Prize” — and understand that for those already in power, who are ALREADY networked public/private networked and have been for generations, that prize is either personal control or collective control within self-selecting collaborative networks usually connected with some with major personal control (i.e., owners of billion-dollar tax-exempt foundations representing even larger corporate wealth, often also privately controlled) of the income-producing assets, paying the least possible taxes on them, which perpetuates the stockpiling of wealth strategically for future use.

When (like, NOW) the nonprofits are still proliferating, but lack “sticking power” and accountability (adhering to ethical, legal standards at the state and federal levels, individually and throughout the self-selecting networks usually organized for multiple causes rolled into one), it becomes clear that from the start we had, and now we still have, a systemic, inherent, built-in conflict of purpose, not just a passing conflict of interest in specific cases.

So this language for the population as a whole needs practical translation into the “Who-What-When-Where-(“WTF?”)-and Show Me ALL The Tax Returns, Financial Statements (public and private both) and Entities Involved” language. We can’t all read all of them. But we ought to, it seems, all at least to become aware they exist, and familiar with their format, and understand the most misleading features of their omission from mainstream discussions whenever and wherever BUDGET or DEFICIT is brought up as a topic, or when faced with fund-raising for any public institution, including local school districts for capital investment purposes.

Sooner or later (i.e., with adulthood in this sphere) constant translation should not be needed. With practice, there comes some fluency; translating isn’t so laborious. Fact-checking is still needed, but you get a sense from looking at either the tax returns, the reporting, and/or the organization website, who is what kind of organization and who is not.

To repeat my post preview paragraph:

Today’s post, Schools for Children of the World, Inc. — Great Theme, Now Here are the Forms 990 (case-sensitive short-link ends “-6Qq”), follows up to what caught my attention as an apparent nonprofit mentioned in affiliation with one of the members, “Bill DeJong” of “DeJong & Associates” and “Schools for Children of the World,” (“SCW”)** on a working group (one of six “cross-sector working groups” for this initiative, the group it called “Educational Facilities Planning Working Group“) as convened by a “Leadership Team” for the “New National Initiative: Planning for PK-12 Infrastructure…” — a Leadership Team based in California, Washington, D.C., and Colorado, with the apparent purpose of establishing mutually controlling and nationalizing the planning for PK-12 School infrastructure and a new association (NCSF) based on membership in the planning facilities, at state or territorial level, which would have major input into pushing for repair, maintenance, and more funds for the same.

I realize, untranslated or in translation it’s a mouthful, so here’s a brief review of the past two posts, remembering that I started above saying I’d looked at the UCB Center’s “() Partners, () Advisory Board, and () Initiatives.”

First, the two posts (also shown on blog’s right sidebar), published the same day:

1st, UCB’s Center for Cities + Schools (Kellogg Foundation-sponsored) 2016 PK-12 Infrastructure Planning (Education Work Group Details) (case-sensitive short-link ends “-6Lh”).

2nd, UCB’s CC+S (Kellogg Foundation-sponsored) 2016 PK-12 Infrastructure Planning (Education Work Group Details) ~~> Cont’d. , (short-link ends “-6P8“).

These two May 15 posts focused more on the Partners and Advisory Board members” than the specific initiatives, as well as the larger context. A third post published May 17 (“Fascinating Genealogy”) had referred to a different UCB CC+S initiative labeled “Strong Cities, Successful Young People,” and so is not included here as to the topic “Schools for Children of the World.”

As I’ve shown, the UCB “CC+S” Partners list and Advisory Board list have a certain emphasis on the Washington, D.C.-based “21st Century School Fund” (“21stCSF”) and its sponsored, “spin-off,” 2013-incorporated nonprofit the “National Council on School Facilities” (“NCSF”). I also showed that the NCSF is unique in prohibiting non-civil-servant membership — they want decision-makers on school facilities. NCSF also apparently suffers from a “failure-to-launch” (physically find its own digs/street address) and, like its parent organization, the “reluctant to file our returns” syndrome. It shares a street address and more, housed, probably inexpensively, at the Thurgood Marshall Center for Service and Heritage, run on what seems like a lean budget by the Thurgood Marshall Center Trust. (Some more on this, below).

Of the six “cross-sector working groups,” I picked one, and looked at the membership and picked one name out of several as likely representing a nonprofit, and then, naturally, went looking at the tax returns. At the bottom of the 2nd post, after looking, but being somewhat exhausted on this process for, at least that post, I commented:

After taking a dash through “Schools for Children of the World” ([its] self-reporting AND 10+ years of tax returns — after first noticing it was switching reported legal domicile between Kansas and Ohio, while a principal officer was in Illinois, and that the address was sometimes in Colorado but their operations mostly (turns out) in the Honduras, Haiti, and eventually (allegedly) Liberia + Nigeria, apparently to practice there which is in process in the USA also and [after noticing] how many DeJongs seem involved overall (so far, father and two sons Brent and Matt. I DNK how “Tracy” fits in), I put the screenprints into a named folder for follow-up.

But will say, based on that “mad dash” (when I dash madly, I still look for consistency (or lack thereof) in categorizing or reporting revenues (and expenses), [I often observed] incompleteness of returns and avoidance behaviors, like failing to name the grantee where the amount is significant.

In Honduras, particularly, looks like they are testing out a country-wide “Educational Master Plan” for all schools in the country, sponsoring semi-annual trips, some of the business of course to be shared with DeJong relatives.

I also found a google groups message from others (“Carol & Phil”) tracking some DeJong entities and their “shtick” which seemed to involve targeting underpopulated or poor school systems, evaluating, recommending school closures, and rebuilding a larger school in its place. A portion of that quote, then:

Google Groups message, Topic (based on the url) Coalition to Strengthen Austin Urban Schools:

…From scanning an array of news articles, the company lit & checking with other communities affected by Dejong-Richter consultations, (Boise & Grand Rapids) the following pattern appears to emerge.

– While DeJong Richter bills itself as an educational consulting firm, what they really do has less with education and much to do with facilities & with construction.

– When hired by a school district to create a “Master Facilities Plan” they choose urban areas where the schools are generally small and old (these area generally inner city areas that have been depopulating in recent years)

– After going through their consulting process (i.e. evaluating the old buildings & assessing the student demographics) they recommend closing several schools and building a very large new school.

– They just happen to also handle setting up bond elections and their affiliate company (same Ohio address) DeJong & Associates which specializes in building large schools.

Both news articles & their web page indicate they have done this with scores of school districts. [[the groupmail message then goes on to list some of the related entities]]

I also remembered the name “DeJong” from somewhere else and in writing this post, found it on an early 21st Century School Fund tax return, showing a pre-existing relationship to the 2016 Infrastructure Planning Initiative referenced above. I’m getting to that…

I will recite the relationships again below with more visuals because without the visuals, or some background to what each phrase is, and where it sits in a heap of relationships, people are more likely to be confused, by the many names, relationships, and — it comes with the territory — tax return excerpts — that are going to show up below!

Yes, it’s tedious to keep documenting and reviewing, but, left unsorted, unevaluated, and without appropriate labels, it will serve just to impress, confuse, or otherwise suspend any concerted efforts to look further into the jumbled verbiage mess of “we’re with THEM doing THIS, for Health, Equity (Reducing Disparities), and Planning Good Things for All Children in All Communities; we’re also associated with Very Important People, Institutions (UCBerkeley), and Organizations (Ford Foundation comes up, W.K. Kellogg Foundation, Brookings, and more, show up in the documentations) — so, “Not to Worry….“

They are indeed associated with VIP Institutions, Organizations, and Public Officials — but the real question is how, and in whose best interest. To answer that, we need more of the facts — and these many of these sponsored organizations’ websites, as well as the university center(s) are more interested in advertising and self-promotion than specific self-revelation attached to dollars, consistently maintained legitimate business entities (or government entities) and valid timelines.

I’m worried with good cause, and particularly the closer I look at ANY of the many organizations involved. Is it such really a hard thing to demand: when the organization is doing business and collaborating with others tax-exempt and/or for-profit, and especially targeting the use of public funds and public institutions AND real estate (which public school facilities are!) — “file your damn tax returns and stay incorporated!”? And is it really so much to ask that those collaborating WITH them demand compliance with staying incorporated and filing Form 990s (and, as appropriate, audited financial statements if the organizations are large enough where it’s required), and if those cease complying, they drop the relationship, or publicize the violations?

Then again, if a whole great-cause-specific network is designed AROUND exactly this type of unaccountable behavior, it’s up to us to demand a different way of utilizing tax receipts, that is public funds.

Many other foundations were involved — early on — with the 21st Century School Fund and in today’s post, Schools for Children of the World, Inc. — Great Theme, Now Here are the Forms 990. (case-sensitive short-link ends “-6Qq”) by looking harder for the earliest on-line tax returns (I found for FY2000), I found an early board of directors associated two or three more “failed to stay filed” entities in D.C. and also a nonprofit in California.

Among the many cooks in the kitchen, spoons stirring this pot — an extended family clan, or perhaps we could call them godfathers + godmothers, are multiple sponsors and donors from the start of the 21st Century School Fund. Naturally, 21stCSF was also sponsoring other individuals and nonprofits too from ITS start, whether as grantee, or as subcontractor. So the money is flowing in this move to build the capacity and will to support more, better, and more equitable, healthy and green public school infrastructures, and call down billions more spending, and better distributed too.

This overall theme intersects at least in some UCB CC+S uploaded, 21st Century School Fund (and friends) publications, with the US Green Building Council (one of its centers) in Colorado.

Despite all these finances moving around the network, when it comes to producing yet another report, someone has to sponsor it and take credit, which for the one featured at the UCBerkeley Center (top-center billing along with others in the “sliding-banner” formation), which was the W.K. Kellogg Foundation.

1st, UCB’s Center for Cities + Schools (Kellogg Foundation-sponsored) 2016 PK-12 Infrastructure Planning (Education Work Group Details) (case-sensitive short-link ends “-6Lh”).

2nd, UCB’s CC+S (Kellogg Foundation-sponsored) 2016 PK-12 Infrastructure Planning (Education Work Group Details) ~~> Cont’d. , (short-link ends “-6P8“).

I was looking at one of its initiatives in the second of those posts. Image, if the main banner is clicked, leads to a summary and an uploaded pdf:

(Click image for url; but that UCB “CC+S” website may change over time).

From: “http://citiesandschools.berkeley.edu/news/ new-natl-initiative-planning-for-pk-12-infrastructure” (quotes the image below the second heading).

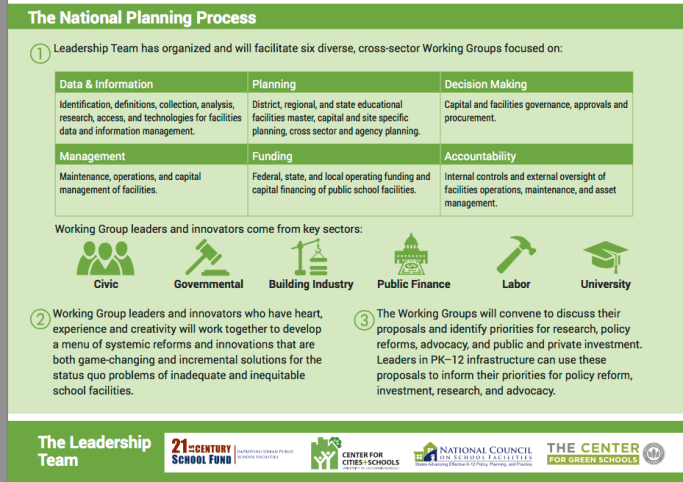

…CC+S is partnering with the 21st Century School Fund, The Center for Green Schools, and the National Council on School Facilities to address the structural problems of inequitable and inadequate school facilities found in too many communities across the U.S.

Through this initiative, six national cross-sector working groups have developed a menu of solutions to guide government, industry, labor, and the civic sector in the delivery of high performance public PK-12 infrastructure for all children. The six working groups are organized around basic elements of a well-managed facilities program: Data and Information, Educational Facilities Planning, Management, Funding, Governance and Decision Making, and Accountability. This map identifies policies, practices, and tools needed to structure, manage and fund the public and private capacity for equitable and efficient public school facilities for all communities.

Initiative Summary and Working Group Descriptions (PDF)

This initiative is funded by the Leadership Team organizations and the W.K. Kellogg Foundation.

Photo Credit: wavebreakmedia/shutterstock.com (and the footer of this page shows the UCBerkeley Center of Cities and Schools, logo, at the School of Environmental Design, IURD (Institute for Urban and Regional Design).

In other words, the website “http://citiesandschools.berkeley.edu” is being used in part to upload the various studies and display logos and blurbs about who’s who in which networks, as well as (I showed in two posts at least) to solicit more funds for UCBerkeley under a fund named after this CC+S project.

As to the “Working Group Descriptions, in the last May 15, 2017 post (UCB CC+S… cont’d.) I chose the “Educational Working Group” to look up, in which you will see the reference to “Schools for the Children of the World.”

Internal details of this will show (I hope) how they came up with an “Educational Working Group” in the contents, but — being about School Facilities Planning — don’t mention any working group or even sector labeled “Education” (“University” is a subset of “Education”)

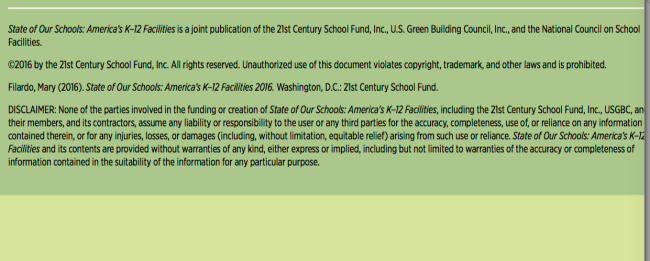

Regarding this “Initiative Summary and Working Group Descriptions (PDF),” I also pointed out that despite the obvious intent to be used for certain facilities planning and funding purposes, based on its report, it still comes with fine print — a firm disclaimer of responsibility by any of the parties or funders if anyone chooses to rely on this data for any purpose as to its accuracy or completeness (next image). I wonder if the same thing could be said to the IRS regarding the tax returns of the entities herein? For comparison, consider an audited financial statement transmittal letter (example below for the District of Columbia government in YE 9/30/2002 and in YE 9/30/2015), it has to specify an opinion (qualified, unqualified…) and the basis of its opinion clearly as well as clear descriptions of what it did, and did not audit, and who bears responsibility for the statements it audited. This 2016 upload is only an initiative summary, but it comes with a major disclaimer.

Notice, it’s a “joint publication” but the “© 2016” is held just by the 21st Century School Fund, Inc.:

I’ve posted on this before, and have been considering it for several days. My key concerns include who’s funding it, who it’s funding, and why the spotty availability of tax returns dating as far back as it says it existed (1994). These concerns are reflected in an over-annotated “About” page. In general, “about pages” for any organization can (and should) be taken with a grain of salt — I don’t know if any group can be held legally responsible for mistakes or mis-statements on them — but if the first sentence is false? And if what’s not stated are simply the larger entities behind it, making this more of a “front” entity than a highly talented and influential nonprofit which says it started in 1994, and proof exists of at least 2002 (8 years later!) tax return!

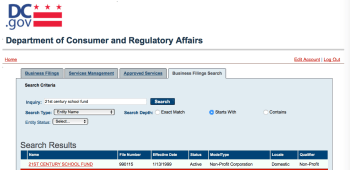

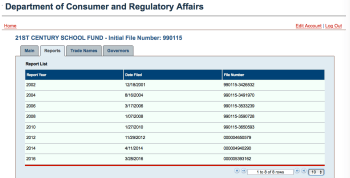

Business Search a Corporation, LLC (etc.) in D.C. — I just posted this link under “Vital Links” on blog right sidebar, top entry). You must register a free username and password to use; I have because so many influential organizations choose D.C. for their place of business, or legal domicile. In checking here today, I found this entity registered in 1999 (not 1994), is active as a domestic nonprofit, and has filed biennially as required since then:

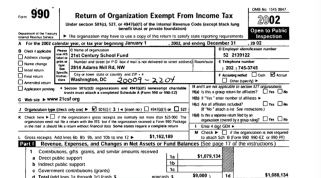

From 21st Century School Fund, Inc. <== link to the “testimony” pages; scroll down to see that testimony under this entity name went as far back as 2002 to DCPS (D.C. Public Schools) regarding budgets — although the entity’s first visible tax return that I can find was not until FY2002 (<==EIN#522139122, entire return; next three images are excerpts from it). That Form 990 has a Schedule A of Support showing 21st Century School Fund received contribution (and produced revenues for services as described on Schedule) as far back as 1999. Other self-descriptions of the entity say it started 5 years earlier, in 1994, see annotated “About Us” page image.

After that image, I searched “citizenaudit.org” and clicked EVERY result showing that EIN#, discovering one earlier Tax return for FY2000, (BUT none for 2001) which answers other questions I had about their activity, and shows a Schedule B showing $192K of contributions for that year (in 3 chunks only, one of $152K) and more on Ford and other foundations, and the prominence of DeJong & Associates (comes up here) and a certain software in their activities. References to payments from previous years also shown.

FY2000 Return (CitizenAudit.org link), or view as uploaded to this blog; I annotated — not heavily but some.

We see that DeJong & Associates (connected to “Schools for Children of the World,” as I showed at bottom of recent UCB CC+S May 15, 2017, post) shows up in the revenues section of this one,

21stCSF FY2000 found+printed (2017May19) @pdfs’citizenaudit’org:2002_03_EO:52-2139122_990_200012 and what were some of the other related organizations or corporations (and/or government officials) involved even this early. I may come back to this situation as better explaining what’s going on here, but have laid out some of the parts in next few paragraphs and screenprints.

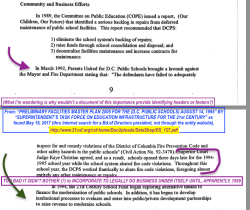

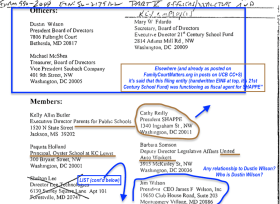

A second document (found only by searching the “President” named on this early tax return, Dustin Wilson of Bethesda, MD, which brought up a document dated 1995 from the 21stCSF.org website. It shows a Task Force started by the DC government officials, but “co-chaired” by 21stC SF (which wasn’t registered in DC at the time, per DCRA.gov, as a corporation) and some other names who show up on the Yr2000 tax return. Filename: “

Found by searching for FY2000 21stCSF President Dustin Wilson (of BethesdaMD) –citing 21st SF in a 1995 doct (CSF-Home|DocUploads|DataShop|DS_127″ See cartoon-like cover with school-house (?) image:

Click image to see larger (DC-based, 1995) Superintendent’s Task Force on Educ Infrastructure for the 21st Century

Click image to see pp9-10 showing 1994 reference to 21st Century School Fund before it incorporated, and other possible impetus for this Task Force..(1989 rept, 1992 lawsuit re: fire codes in DC publis Schools),

(DC-based, 1995) Superintendent’s Task Force on Educ Infrastructure for the 21st Century

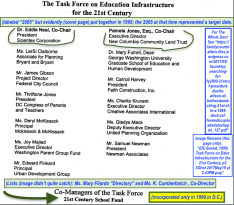

(See Task Force on Educ. Infrastructure for the 21st Century Co-Chairs. One specializes in technology (long-time federal contractor), the other is a Land Trust..

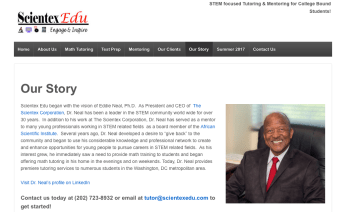

The Task force is “Co-managed” by two people with only affiliation “21st Century School Fund. You will notice Nat’l Co-Chair & President Dr. Eddie Neal of “Scientex”. His LinkedIn Scientex Corporation Described on the LinkedIn:

President and CEOThe Scientex Corporation June 1979 – Present (38 years)

Founder and CEO of engineering research and services company providing technology and management services to federal and local governments worldwide. Founded as a U.S. Navy systems engineering contractor, the company evolved into a prime contractor for U.S. civilian agencies including; Department of Transportation (DOT), Environmental Protection Agency (EPA) , United States Agency for International Development (USAID) and National Institutes of Health (NIH). The company performed over 300 contracts with a total value exceeding $100 million. The Scientex Corporation has received local and national recognition, including; selection by U.S. Small Business Association (SBA) as Top Prime Contractor to the federal government (1986), citation by Black Enterprise Magazine as a top 100 Black Owned Business (1990) and recognition by US DOT for commercial application of innovative technology for transportation safety (2005).

He is also associated for many years with an Oakland, California-based (and well-connected) ASI (African Science Institute) looking to encourage STEM involvement in the African diaspora (incl. in the USA and internationally), started under a different name in 1967. There is also a Scientexedu.com — notice, that’s not a *.edu website — with his image and photo on it, which is where I found “ASI.” Pictures are effective, so here are some:

SCIENTEXEDU.com (a tutoring site, not much to it but posting prices and contact info):

1

2

3

Three Images from the website ASI-org.net show a neat presentation with what sounds like a great idea, but the website is underdeveloped (too few links for the activities described):

History of African Scientific Institute implies continuous legitimate existence throughout (which a simple check shows, is misleading)

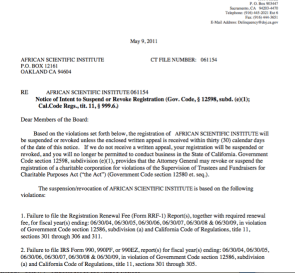

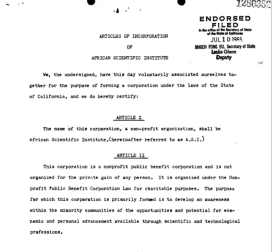

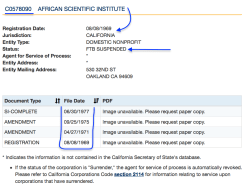

Well, in California, the “African Scientific Institute” has had two incorporations with two different entity#s (one in 1969, another in 1985), BOTH are FTB-Suspended. It also shows up as two separate charities (sic) on the Office of Attorney General Registry of Charitable Trust — one is delinquent and the other (which turns out to be the earlier one) is simply “not registered.” The earlier one “Not Registered” with California OAG Registry of Charitable Trust was eventually FTB-suspended in 1977 (looks like) another, with same name and street address (and just 3 men involved — Dr. Eddie Neal wasn’t listed as one in founding documents) was pulled together in 1985 (although Founding document signature pages are undated, then followed by a Notary Public. What kind of people as late as 1985 didn’t know to put a date (or, just didn’t) when signing Articles of Incorporation?), and this one DID register as a charity– but apparently never filed a single tax return or (this century) showed any revenues over $25,000. It also didn’t file ANY required annual tax returns (RRFs) until, after 1st notice of delinquency, 2nd notice of delinquency, and finally re: Fees and Intent to Suspend (an attempt to collect $375 fees due, based on $25/year for each thing not filed…). Apparently they then quickly filed all missing RRFs improving their status — as a charity at least — to simply “Delinquent” while the corporation remains suspended. That EIN# was 237157285. Rather than drag the readers through all of this (submit a comment — and maybe a few $$ for my time! — if you want to see the images annotated with captions and further explanation). I’ll just slap some of them up here for viewing:

California OAG asks African Scientific Institute for all its past RRFs (annually required, many years missing) and its many Form 990s (ditto) in May, 2011 in a “Notice of Intention to Suspend” (after two notices of delinquency were apparently ignored).

From 1985 articles of incorporation for 2nd version of African Scientific Institute.

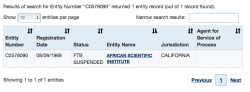

African Scientific Institute | Calif. SOS details for the 1969 version (Click Image to see this one)

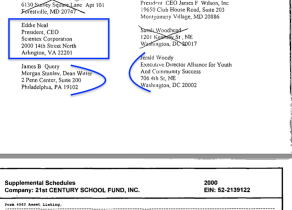

Then, on the later 21st Century School Fund FY2000 Tax return (my annotated version of the one found on CitizenAudit.org (same link as shown earlier), evidence of contracting with Scientex, and the importance of developing certain software (FORMAT-Pro), as well as showing Dr. Eddie Neal on the Board of Directors. The Program Services Accomplishments page gets complicated, and can be somewhat matched with the Schedule B of Donors. When in question on next 4 images, go to that annotated full Form 990 Yr 2000 and scroll through it, keeping in mind this was about 5 years AFTER the Superintendent’s Task Force.

21stC School Fund Form 990 Yr2000 Bd of Directors (Detail w affiliations) #1 of 2 images.

21stC School Fund Form 990 Yr2000 Bd of Directors (Detail w affiliations) #2 of 2 images, shows Eddie Neal, President/CEO of Scientix Corporate + others possibly from 1995 Supt’s Task Force.

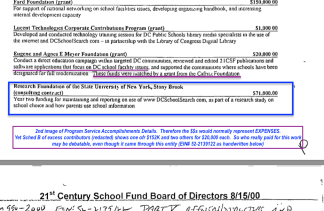

21st C School Fund Form 990 Yr2000 Click Image for ProgService Accomplishmts Detailed (FY2000 21stCSF) Image 13B (bottom of page)

21st C School Fund Form 990 Yr2000 Click Image for ProgService Accomplishmts Detailed (FY2000 21stCSF) Image 13A (Top of page)

I looked up “Scientex Corporation” in D.C. and found two revoked, and one merged-out (link to search these yourself now :Business Search a Corporation, LLC (etc.) in D.C. (also in my right Sidebar, top link under “Vital Links” Menu; it’s also in this post, if the images are not easily readable). I just quickly verified that ALL THREE versions of “Scientex” are associated with Eddie Neal (his name is on all three) and that the one labeled simply “Scientex Corporation (The) “Merged” (middle row below), registered 6/1979, has no reports shown with it. Maybe it merged into the other one which then got revoked; without documents, who knows?

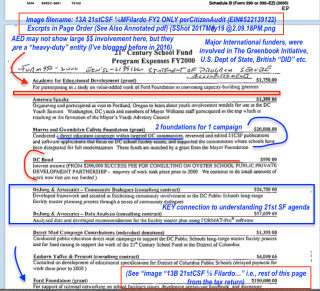

21st C School Fund FY2002 return Pt Page 1 ($1M contribs, notice address)

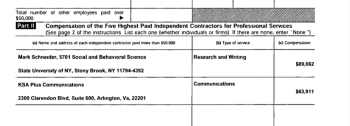

21st C School Fund FY2002 return (Highest Indep Contractor includes Mark Schneider of SUNY(paid $89K) + Communications group in VA

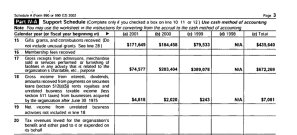

21st C School Fund FY2002 return Sched A of Support shows funds in 2000 and 2009 (and that revenues were higher than contribs for a few yrs) but where are those first two tax returns? Nevertheless, read its Form 990 FY2002 for more info.

Mary Filardo and two others testifying 4/19/2002:… It’s only 3 pages, and that it cites what testimony is ON, but not where (place, address, etc. of any government agency) or in what form it was given (written or spoken, which entity was meeting, who was present at the meeting, etc.) — which is unprofessional, and troublesome to verify, including any list of who else testified at the same meeting.

Above: 21st century School Fund, bottom of their “Testimony” uploads show testimony occurring before its first Form 990IRS shows up (at FoundationCenter.org, which gets them from the IRS).

“I have the opportunity to travel and meet with Chief Operating Officers, Directors of Facilities, facility planners, architects, builders, school board members and community leaders across the country about school facility concerns. There is hardly a city or school district that does not establish a public oversight body to monitor the implementation of the capital program at the inception of the program. I know of such bodies in Chicago, Cleveland, Oklahoma City, San Antonio, and Miami-Dade County.

I request the Council or Mayor initiate an audit of the process, cost and quality of the capital projects that have been undertaken since FY1998 and that the Council put a line item of approximately $350,000 in the District’s capital budget to pay for this audit. I also call on the Council and Mayor, as an urgent matter, to work with the 21st Century School Fund and others to establish a citizen’s capital program oversight committee immediately…

I’m wondering why there is no reference throughout to any CAFR’s produced by the District of Columbia already, which report such things, before demanding another one. I just went looking, and it only took a few moments to find them on-line. Why is no reference being made to this documents (these financial reports, and existing audits) which report, by funds, and functions of government, what’s going on in the District of Columbia overall, its primary government (including varieties of funds blended component, separate component units, etc.) and assets, liabilities, changes in fund balances, etc. of each of them?) Is that just not consistent (informing the public) with being the resident network (in combination with identified — then and later — sponsoring friends? One look at the FY2002 tax return for 21st Century fund, or various information on-line at their “BEST Collaborative” quickly shows other sponsoring organizations — such as the Ford Foundation….

DC CAFR (FY ended Sep 30, 2002) Initial pp (Ltr Transmittal etc) incl discussion of changes in CAFR Reporting started this YR (I annotated several of the pages; this is not complete CAFR). Or, DC FY 2015 CAFR (pp 17-19 only)- Org Chart,Principal Officials, + GFOA Cert Achievemt

Total results: 3. Search Again.

MOVING ON towards the 2016 PK School Facilities Planning Initiative

The Leadership Team components:

I already pointed out that “The Leadership Team” descriptions (all=green image with logos at the bottom) involved only two nonprofits (which shared the same street address) and two centers — one center at a university, and the other one, at the United States Green Building Council, Inc., which center had only started around 2007.

The various start dates involved, therefore, in this “Leadership Team” of two centers and two nonprofits (both housed at the same street address, also a historic building being run by one trust (Thurgood Marshall Center Trust) and with tenants involving several other nonprofits*** look to be, according to their self-reports, 1994 (21st Century School Fund), 2004 (UC Berkeley Center for Cities and Schools), 2007 (The Center for Green Schools), and lastly ca. 2012 and as sponsored by the Advancement Council (a California nonprofit) and co-located with the 21st Century School Fund at “1816 12th Street NW, Thurgood Marshall Center, Washington, DC 20009” [NS but tax return says, currently 3rd floor] (National Council on School Facilities). The three “states” involved as to those entities are District of Columbia (two co-located), Colorado, and California.

Short comments and a few images on Thurgood Marshall Center for Heritage and Service (building) and the Trust that runs it (some also found on my other posts, in the same context), involving other tenants:

***– a situation I’m noticing around the country: Someone gets or rehabilitates a historic building, and then invites the nonprofits in as tenants for free, or below-market cost. For example, Thurgood Marshall Center Trust (tax returns added post-publication to my 2nd May 15th post) is barely clearing its expenses, has almost no public contributions, and the primary source of program service revenues is (per Part VIII) “rents.” So, one could say (I think it’s a reasonable assumption) that whoever is financing those nonprofits is helping pay the rent, AND they seem to be overall getting a pretty good deal on the rent. I’m referring to where the 21st Century School Fund AND the National Council on School Facilities exist (same street address). Notice that the latter is NOT listed in this (viewed today) Thurgood Marshall Center for Services and Heritage statement of tenants. Just a few images and notes on this (I showed more in a previous post):

Click image for better view; website url also on image

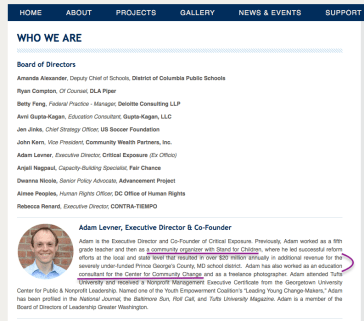

One of the Thurgood Marshall Center tenants (“Critical Exposure“) has leadership (Adam Levner) associated with the (Well-known) Center for Community Change.(in its 45th year at least, well-known Executive Staff, Deepak Bhargava, of Open Society Foundations (OSI-Baltimore) connections. Levner’s association with Center for Community Change, it says, was as educational consultant (not employee). Searchable (both org. and individual Bhargava) on this blog.

Deepak Bhargava of Center for Community Change (Exec. Team) (contains an mp3 file to listen) Deepak Bhargava Speaks at OSI-Baltimore Donor Appreciation Event Apr. 28, 2011: Deepak Bhargava, executive director of the Center for Community Change and Open Society Foundations board member, spoke at a reception for OSI-Baltimore donors about the role of community organizing in shaping the future of our country. The Center for Community Change is a national nonprofit organization whose mission is to develop the power and capacity of low-income people, especially low-income people of color, to change the policies and institutions that affect their lives. During his tenure as executive director, Bhargava has sharpened the center’s focus on grassroots community organizing as the central strategy for social justice and on public policy change as the key lever to improve poor people’s lives.”

The Critical Exposure (at Thurgood Marshall building in D.C.), Center for Community Change / ACORN / Open Societies Foundations connections, or at least possible connections:

Nonprofit executive overseeing the White House’s Obamacare youth video contest is the disgraced ACORN group’s former top lobbyist (in the DailyMail.UK) By David Martosko in WashingtonPUBLISHED: 19:56 EDT, 19 August 2013 | UPDATED: 20:16 EDT, 19 August 2013

ACORN, the once-mighty Association of Community Organizations for Reform Now, crumbled in 2010 just months after a video sting operation showed its employees advising activists posing as a pimp and prostitute on how to evade federal taxes and hide crimes including human trafficking and prostitution. Congress voted officially to defund it shortly thereafter.

The far-left ACORN was also dogged for years by allegations – some proven, others not – that its street-level organizers engaged in widespread voter registration fraud.

In its heyday, ACORN’s legislative agenda was managed by Deepak Bhargava, an Indian-born community organizer. Bhargava left ACORN in 2002 after holding the top government affairs position there for 10 years. He is now executive director of the Washington, D.C.-based Center for Community Change.

In 2013 that organization sponsored a new youth outreach arm called Young Invincibles, which announced a partnership on Monday with the U.S. Department of Health and Human Services. Their joint effort will award cash prizes to the creators of online videos that convince millennials to sign up for Obamacare health insurance exchanges, which open for enrollment on October 1

[[…Notice the “fiscal sponsorship” comment for a public/private partnership, so typical1]] Continuing quotation from the DailyMail.UK, 2013 —

(The DailyMail.UK sounds from the overall tone and references like it may have some conservative leanings… I notice it was also quoting someone from the likewise conservative Capital Research Center (ditto), however I just wanted to point out that the D.C. Thurgood Marshall Center for Service and Heritage looks like it might be housing some progressive/Left-leaning organizations, which may reflect on another one of its tenants, the 21st Century Fund, but certainly doesn’t establish this general agenda just by occupancy.

The rents MUST be low for all the entities shown in the tenants list to only be producing about $1M of rents/year in D.C. in a restored historic building. (I just added the Thurgood Marshall Center Trust Forms 990PF (last 3) to my May 15th post for easy viewing. Or use the “Search Again” link at any set of Forms 990 (3-row tables) I post here. Compare Pt. I line 9, “program service revenues,” with Part VIII, Line 2, which specifies the same or nearly the same (I DNR offhand) amount as “Rents.”

NOTE: I was going to go from here to the SCW tax returns. However, in doing some follow-up on that merger, and on their Secretary of State filings (in Colorado, KS where legal domicile was claimed one year, and Ohio), I found it too much detail for one post. This post was written first, both will be published as a “dynamic duo.” //Let’s Get Honest May 24, 2017.

Reblogged this on World4Justice : NOW! Lobby Forum..

daveyone1

May 25, 2017 at 2:58 AM